From Wikipedia:

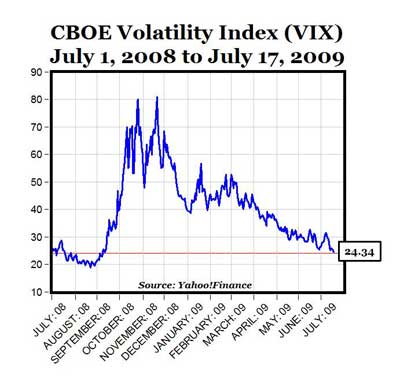

VIX is the ticker symbol for the Chicago Board Options Exchange Volatility Index, a popular measure of the implied volatility of S&P 500 index options. A high value corresponds to a more volatile market and therefore more costly options, which can be used to defray risk from volatility. If investors see high risks of a change in prices, they will require a greater premium to insure against such a change by selling options. Often referred to as the fear index, it represents one measure of the market’s expectation of volatility over the next 30 day period.

MP: The chart above displays the daily history of the VIX back to July 1, 2008 [data here], showing that the index of market volatility fell below 25% on Friday for the first time since early September 2008, and reached a fresh 10-month low.

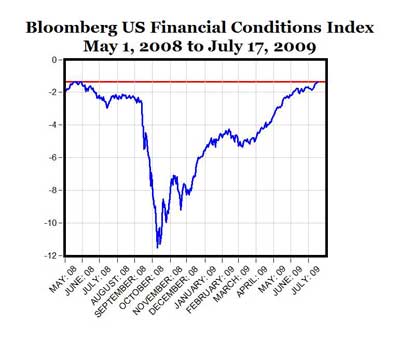

The chart below shows the Bloomberg U.S. Financial Conditions Index, which “combines yield spreads and indices from the Money Markets, Equity Markets, and Bond Markets into a normalized index. The values of this index are z-scores, which represent the number of standard deviations that current financial conditions lie above or below the average of the 1992-June 2008 period.”

The chart displays the Financial Conditions Index daily from May 1, 2008 through Friday (July 17, 2009), and shows that the index is approaching the same levels as May 2008. Based on this measure, financial conditions in the U.S. were at their worst and bottomed in October 2008, and have been improving steadily for the last 9 months. We’re now getting back the same financial conditions that prevailed more than a year ago.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply