There is a growing concern that we are approaching a wave of sovereign defaults in Europe. And if there is default on government debt, it will have an effect on the balance sheets of Euroepan financial institutions and this is the source of the recent concerns about the solvency of some of these institutions.

Stress tests are designed to look at “pessimistic” scenarios to see whether financial institutions have enough capital to deal with them. But stress tests will always have an element of subjectivity. How pessimistic should we be in these scenarios? The IMF has recently expressed their concerns about the need for capital of some European banks because of the possibility of sovereign defaults not priced into some of the stress tests that European regulators have produced. This is a source of debate between European officials, the ECB and the IMF. But what is a good assumption about sovereign default in Europe? How do we measure the probability of default? Should we look at CDS (credit default swaps or should we use interest rates as a measure of default probabilities?

Both of these measures capture the “market” view on default probabilities. A completely different approach is too look at the fundamentals of fiscal policy sustainability (yes, it requires more work but it is always a productive exercise to look at the numbers and not just at how others read those numbers!).

The IMF fiscal monitor (last issue is just out) provides a very detailed analysis of the fundamentals behind fiscal policy. They look at several indicators or fiscal policy risk:

– gross debt as % of GDP (Debt)

– gross financing needs as % of GDP (GFN)

– short-term debt (as % of total)

– the currency deficit (adjusted for the cycle) (CAPD)

– Expected increase in pension spending over the coming years

– Expected increase in healthcare spending over the coming years

– Difference between interest rates paid on debt and the growth rate of output (r-g)

All indicators are straightforward, they look at the past (debt), the present (deficit) and the future (pensions, healthcare) taking into account the cost of borrowing (interest rate) and the ability of the economy to generate growth to keep the debt to gap ratio under a reasonable number. You want all these indicators to be as low as possible.

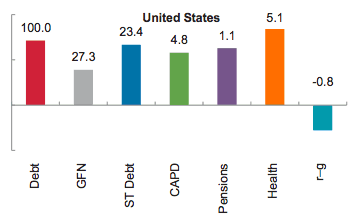

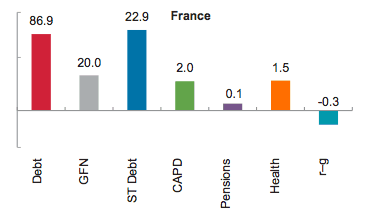

I am copying below the indicators for some of the countries they analyze (indicators are in the same order as in my list above)

Comparing France and the US we can see that both countries look risky along several dimensions. Overall, the US seem to score worse than France in several dimensions. Higher level of debt, deficits and more importantly, a larger future burden in terms of pensions and healthcare spending. The only indicator where the US does better is the low interest rates that the US government faces when borrowing in financial markets.

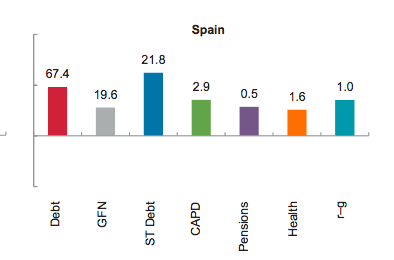

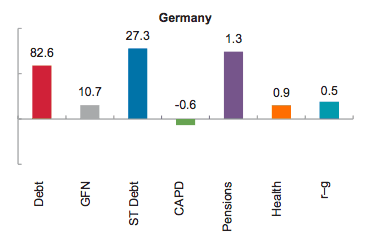

Here are the data from Germany and Spain

They do not look good either although the risks are similar or slightly lower than the ones in the US or France. Levels of debt are lower in Spain, current deficit is lower in Germany. Short-term pressures are similar to other countries and long-term pressures (pensions and healthcare) look better both in Spain and Germany than in the US. The only dimension where both of these countries do worse is when it comes to the difference between interest rates and growth.

In the case of Spain, the issue of credibility is key. If credibility is lost, the average interest rate paid on government debt will increase and will make more difficult to set a sustainable path for fiscal policy (in the chart above the indicator of the right will get higher). But the credibility of a government must be a function of the other indicators. The trust in a government’s ability to repay should be a function of the level of debt, future spending, etc. Looking at those first six indicators above for Spain explains why the Spanish government insists that their fiscal position is not as bad as what “the market’ believes. If you remove the last column, Spain could be seen as the strongest of the four countries.

But expectations and credibility matter and criticizing speculators might not be enough. What is needed is clarity in communications coming from the European authorities in order to rebuild the faith in the system. And this requires a combination of not denying bad news while at the same time restoring credibility where is needed. They need to try harder.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply