Via Calculated Risk, here is a post from the Healdsburg Housing Bubble which goes into some detail on the subject of Option ARMs and those in particular owned by Wells Fargo.

I’ve been trying to make the point for some time that the Wells’ Option ARMs that it inherited in the purchase of Wachovia (Wachovia came by them via its purchase of World Savings) are not an immediate threat to the bank. The terms of the mortgages were more lenient in the amount of negative equity that would cause an automatic recast of payments and the recast feature does not automatically trigger until the ten-year anniversary as opposed to the five-year featured in most other Option ARMs.

From the HHB:

If you’re paying close attention you’ll notice that something doesn’t add up. Wells Fargo, who holds more Option-ARMs on its books than any other institution, states in their last 10-Q filing:

Based on assumptions of a flat rate environment, if all eligible customers elect the minimum payment option 100% of the time and no balances prepay, we would expect the following balance of loans to recast based on reaching the principal cap: $4 million in the remaining three quarters of 2009, $9 million in 2010, $11 million in 2011 and $32 million in 2012… In addition, we would expect the following balance of ARM loans having a payment change based on the contractual terms of the loan to recast: $20 million in the remaining three quarters of 2009, $51 million in 2010, $70 million in 2011 and $128 million in 2012.

In short, Wells expects $56 million in Option ARMs to recast due to the loan balance reaching 125% of the value of the original loan and another $269 million to recast based on the terms of the loan. Given that we’re talking about a portfolio of over $100 BILLION of these loans, this means ESSENTIALLY NO LOANS WILL RECAST due to the negative amortization limits or contractual terms before 2012.

Both assumptions seemed suspect, yet, they are in fact true. Looking at page 55 of the Golden West 10-K from 2005 we read:

…most of our loans are scheduled to have a payment change without respect to any annual limit in order to reamortize the loan over its remaining life at the end of the tenth year or when the loan balance reaches 125% of the original amount. We term this reamortization a “recast.” Historically, most loans in our portfolio have paid off before the loan’s payment is recast.

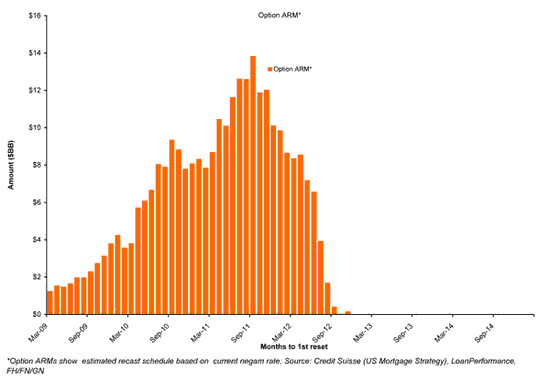

The HHB comes at this issue primarily from the standpoint of the infamous Credit Suisse chart that depicts the coming recasts for Option ARMs. The blogs contention is that the chart is most likely wrong due with recasts stretching out to 2014 and 2015. I think they’re probably right and you might want to read the entire article to get the full flavor.

I want to concentrate on what this implies for Wells. You can approach the situation with a glass half-full or half-empty mentality. If it’s half-empty you’re thinking that it’s just more time to let the negative amortization build up and while the day of reckoning is pushed out, the ultimate reckoning becomes that much more unpalatable.

I on the other hand see it as somewhat positive. In many respects getting through this period is a game of buying time. Right now and probably for the next couple of years, the less you have to write-off as a bank the better. There is going to be plenty to get rid of, so there’s no need to buy trouble. So long as the Option ARM owners are paying their monthly payments, no matter how small, that’s one less item to deal with.

With any luck five or six years from now we will have an entirely different world in which to attack the problem. There’s the possibility that the housing situation might look much different and even someone deep in the negative equity hole might decide to stick it out if it looks like home prices are making a comeback. If not, then let’s presume that we have a much better economic climate. Wells may then be faced with a more or less major problem with these loans but they won’t be facing that problem with ten other major issues that they have to deal with at the same time.

Even if housing doesn’t improve enough to bail out Wells in five or six years, the extra time gives them a lot of opportunity to reserve for any losses. Yes some of their borrowers might look at how far under water they happen to be and mail back the keys but given the low monthly payments and the time horizon before the music has to be faced, I’d wager that most will stay put.

So if you’re looking at Wells and their billion dollar Option ARM portfolio and having nightmares, you can probably sleep more comfortably. In fact, the market might be assessing this risk improperly in which case, the bank might not be a bad buy.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply