There is not much to be said about the August employment report released last Friday—or not much good, anyway. The ongoing updates at Calculated Risk provide a chronicle of the questions and challenges that have characterized the postrecession period. An exhaustive set of graphs are spread across several posts, here, here, and here. The last post in the series focused on construction employment specifically and includes this observation, which is based on the addition of 26,000 construction jobs in 2011 through August:

“After five consecutive years of job losses for residential construction (and four years for total construction), this is a baby step in the right direction. However there will not be a strong increase in residential construction until the excess supply of housing is absorbed.”

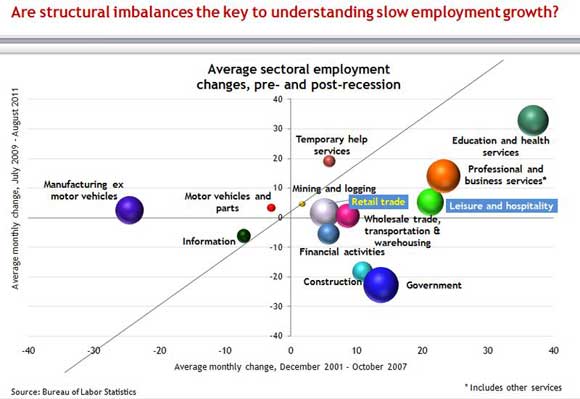

Given the likely pace of turnaround in the housing market, that sounds like a problem. It is not much surprise that employment in the construction sector is, and likely will continue to be, significantly weaker than it was before the recession. Can the same be said of most other sectors? The following chart shows pre- and postrecession, cross-sector average monthly changes in payroll employment, broadly defined according to U.S. Bureau of Labor Statistics’ classifications. For reference, the size of the circles in the chart reflect the relative prerecession size of the sector in terms of employment.

A few points:

- The 45-degree line represents points where average monthly employment changes before the recession (from December 2001 through November 2007, precisely) are exactly the same as the average changes after the recession (July 2009 through August 2011). Consistent with the slow pace of overall employment growth during this recovery, the majority of circles representing different sectors lie below the 45-degree line.

- In general, the pattern of circles is such that those sectors with relatively high employment changes prerecession are those that have exhibited relatively high changes during the recovery. In other words, we have not yet seen a widespread reshuffling of cross-sectoral employment trends outside of the recession. For example, employment changes in the education and health care sector led the pack before the recession, and that sector has led the pack thus far in the recovery. At the opposite end of the scale, job growth in the information sector has remained on a negative trend in the recovery period, just as it was prior to the recession.

- I want to note a few exceptions to the preceding observation, which discusses the sectors with relatively high employment changes before the recession being the same ones that exhibited relatively high changes during the recovery. As noted, employment in the construction sector is well off its prerecession pace. What may be less appreciated is the fact that manufacturing employment, outside of the motor vehicles and auto parts sector, has experienced monthly employment gains that are better than the prerecession rate. Employment in the government sector, on the other hand, has noticeably flipped from positive to negative. This shift is also true of job growth in the financial activities sector, though the change is less dramatic than in the government sector.

Manufacturing and government represent relatively big shares of employment. Including motor vehicles and parts, manufacturing payroll employment was over 11 percent of total U.S. jobs for the period from 2002 through 2007. Government employment was about 16.5 percent (and had the largest single share of sectoral employment in the breakdown used in the chart above). The bad news in the big picture is that the better performance in manufacturing job creation is really a shift from negative job creation in the prerecession period to zero job creation in the postrecession period. And as for government employment, it seems unlikely that the forces will soon align to move job growth in the public sector back into positive territory. (The same could probably be said of financial activities employment.)

I am not pushing any particular interpretation of these facts, but a couple of questions come to mind. Will non-auto manufacturing employment revert to the contracting trend in place prior to the recession? Will employment in the financial activities and government sectors continue to shrink? If so, will these jobs be absorbed by increased employment in other sectors, and how long will that take?

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply