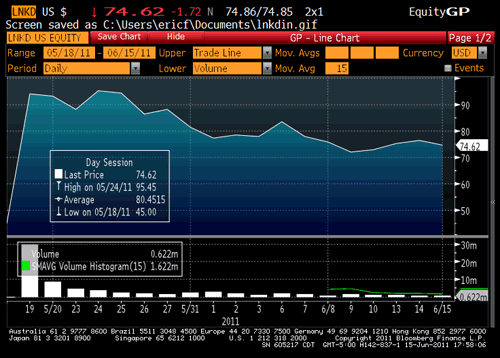

Linkedin (LNKD) has a PE of about 1000, which is making a lot of people very excited (Facebook, , but such valuations seem high to most people, so there are more people eager to short than shares available, causing the ‘borrow rate’ to rise to about 10% annually (ie, you pay 10% on the revenue generated from a short sale).

This perverse borrow rate shows up in the options market. The Feb 2012 $75 strike put trades around $19.80, and the $75 strike call at $14.00. You can put on a Feb forward position in LNKD via options, by buying a call option, and selling the put.

Looking at Put-Call parity, we can generate the following implication. A synthetic forward position can be created by buying the call and selling the put:

Call-Put=(Forward-Strike)/(1+i)

As interest rates are near zero, let’s assume i=0:

Call-Put=Forward – Strike

$14-$19.8=Forward – $75

Forward=$69.19

It currently trades at $74.77. Now, if you are a long term investor, why pay $74.77 for the current GM, when you can by the Feb forward for $69.19? It’s an easy $5. Regular investors don’t reap the borrow rate on their long stocks, that’s all kept by the broker. So it appears that anyone owning this stock in such accounts appears to be leaving money on the table.

Is this a market inefficiency? It depends on semantics to a large degree. Arbitrage does not exist, which for many is all that matters. But market prices are clearly biased, as whenever there are options available on stocks that are hard to borrow you have a large number of investors behaving suboptimally (there are about a dozen of these situations currently in the US).

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

typo alert! GM should by LNKD.