Bernstein’s Pierre Ferragu, the Axe in Research in Motion (NASDAQ:RIMM) is backing off from his uber bearish thesis this morning.

– Ferragu is upgrading RIMM to Market Perform from Underperform (tgt unch. $40) telling his clients to cover their shorts today.

RIM’s stock has lost 39% since its high of February and is now clearly implying a medium term evolution of the company far worse than management guidance or even sell-side consensus implies. With EPS 10% below consensus for this year and 21% for next year, they believe they currently model the bleakest possible outlook for the company and show in this piece of research that a significantly worse scenario is very unlikely to materialise in the next 2 years. As a consequence, Bernstein recommends covering short positions in RIM today.

They also recognise the stock is particularly cheap on any metric, were the company to stabilise its current position and make the right strategic moves to stay in the smartphone race. But they believe management remains in denial of challenges facing the company and therefore do not recommend buying the stock yet, or at least not beyond a short term play on a likely rebound.

They recommend covering short positions in RIM.

RIM’s stock has lost 39% since its high of February, while sell-side earnings expectations only marginally adjusted and management maintained full year guidance. The stock is now trading at 4.7x management guidance and 5.5x sell side consensus for FY12 EPS (ex-net cash). In other words, investors give no credit to these numbers.

Even on their numbers, RIM appears cheap on all metrics. The firm forecasts EPS 10% below consensus (22% below guidance) for this year, 21% for next year. On these numbers RIM recently traded at 5.6x 2012 ex-cash Earnings and 0.9x 2012 sales, at the bottom end of the tech universe.

Bernstein believes the scenario they model is already very pessimistic.

They model RIM’s user base growing only 32% this year and 17% next year, compared to 46% over the last 12 months, which implies a combination of continued share loss in North America, peak shipments in Europe this quarter and a steep deceleration of growth in other markets.

They expect service revenue per user down 25% in FY13 and FY14 resulting in service revenues falling by 10% in FY13 and 14% in FY 14, and device shipment growing 10% in FY12, 3% in FY13, which implies replacement rates will fall from 79% in the last 12 months to 61% in FY12 and 55% in FY13.

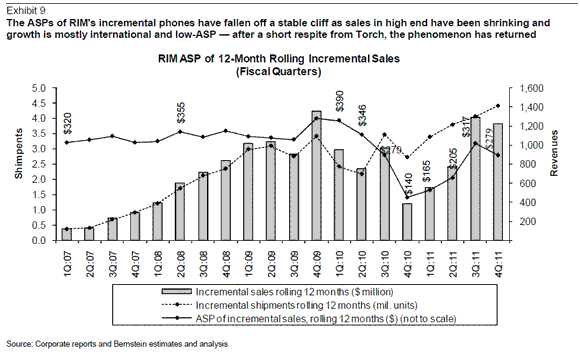

They model ASPs falling 7% this year, 12% in FY2013, which correspond to an ASP of $284 this year and $250 next year.

A scenario still justifying a short position (i.e. driving less than $4 of earnings for this year or next) remain highly unlikely. They do not see EPS falling below $4 per share without a steep collapse in shipment volumes. Such a scenario would reflect a decline of RIM’s user base both the US and international markets, which remains very unlikely in the medium term, given the continued traction the brand gets in low ASP segments and outside of the US.

The firm therefore recommends covering short positions on RIM today.

Notablecalls: Ladies and gentlemen, will you give it up for Pierre Ferragu at Bernstein. He has done a great job as the most bearish Street analyst in RIMM.

Rumour has it RBC’s former RIMM uber bull Mike Abramsky bursts into tears every time Ferragu is mentioned.

The stock is down 39% since February, pretty much in a straight line.

Today, Ferragu is telling his clients to cover their shorts. I suspect the stock will see n-t bounce that could last for several days and takes the stock toward $46-47 level.

I’ve been looking for a reason to buy RIMM for quite a while now (and have the tire marks on my back to prove I have tried). Today we got good one.

Oh and give kudos where it’s due. I do!

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

What all these analyst fail to factor in is that RIM will likely continue annual common share repurchases, currently running at 10% per year. So even if there was no growth at all, RIM EPS would go up by 10%.

So Bernstein’s 32% growth becomes 35.2% on a per share basis.