Morgan Stanley Semiconductors team is out very positive on Sandisk (NASDAQ:SNDK) raising their EPS #’s way above consensus while reiterating their $100 Bull Case target for 2012.

According to the firm, investors are missing the longer-term growth story:

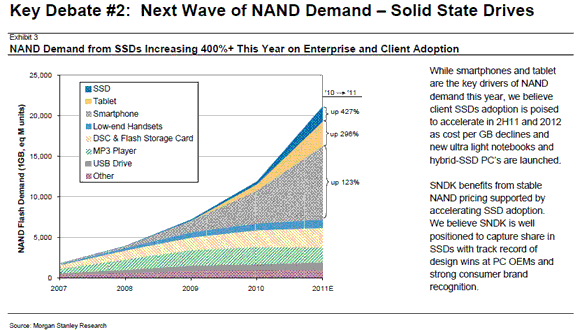

SNDK is trading at 9x/6x Morgan Stanley’s revised CY11/12 estimates respectively, suggesting investors underestimate the revenue and EPS upside potential from three catalysts: 1) NAND is becoming a non-commodity for OEM devices like smartphones as reflected by a 32% delta between spot and contract pricing; 2) client SSD adoption is poised to accelerate in 2H11 and 2012 as new ultra light notebooks with SSDs/and hybrid-SSD are launched; 3) NAND demand for high speed performance in enterprise storage for cloud computing surges.

Raising Estimates: Morgan Stanley raise their CY11/12 estimates on improving supply-demand fundamentals as reflected by Toshiba’s (#2 NAND maker globally – covered by Kazuo Yoshikawa) recent 20-30% annual ASP decline outlook versus MSe 32%. Their revised CY11/12 estimates are 24%/60% above consensus. Firm models full year gross margins at 46% versus 41-44% guide and ~300bps expansion next year.

What’s Changed:

Price Target $65.00 to $70.00

CY11 Earnings From $4.97 to $5.46

CY12 Earnings From $6.28 to $7.31

CY13 Earnings Initiate at $9.90

Notablecalls: OK, this is a new one – NAND is now a non-commodity play as per Morgan Stanley. You hang around long enough in this business, you hear it all.

OK, Morgan Stanley’s thesis seems to be that NAND will be non-commodity for the next 12-18 months as there is a lot of demand and they have the best quality product & manufacturing know-how. People are waking up to the fact NAND is quite difficult to manufacture. So that makes the call somewhat more understandable.

They are also playing the SSD card saying there will be lots of demand in 2012. That’s what STEC CEO kept saying on their earnings conference call last week. STEC is building manufacturing capacity to meet an explosion of demand starting 2012. (Btw, STEC is getting upgraded by Benchmark this morning)

It also appears that the iPad scare is over. It pretty much ended the day JMP cut their rating on SNDK.

Morgan Stanley’s estimates go WAY above consensus which will grab people’s attention.

The SNDK call has a fair chance of working in the n-t.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply