Canaccord Genuity is downgrading MOCVD leader Aixtron (NASDAQ:AIXG) to Sell from Hold with a $25 price target (prev. 37.50) given an increased risk profile based on changing customer patterns, a pending cyclical downturn and relatively rich valuation.

The details:

Investment highlights

• As we revisit our Third Cycle assumptions, we conclude that even with significant support from China, the MOCVD market is on the verge of a cyclical downturn and 2010/2011 will represent a historical peak in equipment sales.

• Aixtron has changed its bookings policy, leaving it up to management’s discretion from a conservative criteria, including deposits, documentation and delivery date. While the company believes this is a normal event in a maturing market, we simply note it has increased the risk profile.

• AIXTRON remains the leading MOCVD equipment vendor, but shares are expensive on a relative basis, especially in front of what we expect will be a peaking scenario and cyclical downturn in 2012/13.

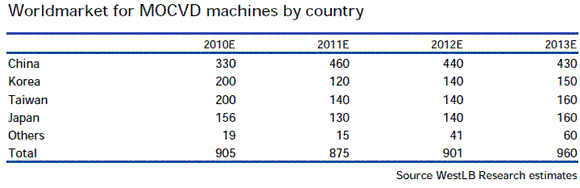

– Canaccord’s not the only firm out cautious on the name. German based WestLB is also cutting their rating to Neutral from Buy on Aixtron (NASDAQ:AIXG) this morning after April sales figures from the LED producers in Taiwan showed only slow growth, and confirm a pattern that the firm has already seen at Cree and SemiLEDS.

LED sales are being squeezed by price weakness and new competition. Accordingly, they have revised their projections for the sale of machines into both Taiwan and Korea, formerly the main markets for LED production equipment. In view of the large capacity additions in China, they still see a strong level of shipments in 2011 but expect the growth in China to be offset by declines elsewhere.

The details:

April LED growth rate drops to 9%. The LED production and packaging sector in Taiwan led by Epistar and Everlight saw sales growth in April fall from 25% year-on-year in March to 9% in April, according to figures published in the last few days. This is based on our sample of 10 companies and compares with a growth rate of 84% this time last year. It is the lowest growth rate since the credit crunch.

Price declines and low margins. We suspect that the year-on-year decline in prices may well have reached 20%. The underlying business in backlighting units (BLUs) for televisions is still seeing increased penetration, albeit with less units per screen, so we expect underlying volumes to increase by around 40-50%. Smartphone and netbook demand may also be some 20% higher in terms of LED units. However, the weak pricing and the effect on the sector of the weak value of sales is bad for margins. Gross margins were below 20% in Q1. Q1 is seasonally slack but it is all the more disappointing that the April recovery has been so slow.

Samsung also complained about the slow screen market. The world’s largest screen producer saw a 25% sequential decline in flat panel TV sales in Q1, which represented an increase of only 5% in the screen market year on year. This is a slow result for a successful product range with a high share of LED BLUs in it. We suspect that the Korean producers of LEDs for TV backlights have even greater difficulty achieving revenue growth than the Taiwanese. The inclination to add new machines against this industry background must be low. In Taiwan, capacity utilisation is said to be 80% but in Korea we believe it is lower than that.

12% downward revision to MOCVD machine market forecast for 2011. In light of the difficult state of the client industry, we have lowered our forecasts for deliveries by 12% for 2011 and 18% for next year. Within this we still believe that Aixtron will increase its market share. This is because of the catch-up effect, which should derive from the success of G5 models and Crius II.

Notablecalls: To put this in context, please go back and read the April 5 Cree (CREE) downgrade from Morgan Stanley. CREE uses MOCVD reactors from Aixtron. So do many of its competitors.

What has been happening is that LED volumes have been going up but ASP’s have been going down. When margins head south, companies will have less incentive to invest in equipment. The equipment side so far has been a duopoly (Veeco & Aixtron) so MOCVD ASP’s have been holding up well. It’s the volumes that are likely to suffer.

For some reason AIXG has always traded at a way (sometimes 2x) higher valuation than VECO. I suspect that this spread may decrease today.

The $25 PT is the Street low target for AIXG and I suspect will create selling pressure in the name in the n-t. I also suspect most people didn’t know about AIXG’s revised booking policy.

The stock took almost a 2 pt hit intraday back in Jan when Citigroup initiated it with a Sell & $30 PT, so it’s prone to make big moves.

I would not be surprised to see AIXG break $39 level in the very n-t

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply