UBS is initiating Sky-mobi (NASDAQ:MOBI) with Buy & $20 target this morning.

UBS thinks the value-added in the handset supply chain has changed from hardware (IC) to software (games or other applications), and thus they are more positive on the long-term outlook for the mobile Internet market than they are for hardware companies. UBS believes the key catalysts for the company’s share price are: 1) the increasing penetration rate of its Maopao platform; 2) improving handset baseband performance, which could better support mobile content functionality; and 3) the rapidly growing mobile Internet market in China. Their price target of US$20.00 is derived from 30x one-year forward PE, and is 44% above the current level.

The share price has fluctuated significantly since the December 2010 IPO: 1) December 2010–January 2011: 37% decline, mainly because of concern on the ‘triple confirmation’ policy; 2) February 2011: the share price rose 51% after the announcement of MOBI’s partnership with Tencent; 3) March-April 2011: 49% rise after MOBI signed an agreement with Sohu; and 4) the past week: the share has declined 33% as some investors sell as the end of the lockup period approaches.

Key catalysts

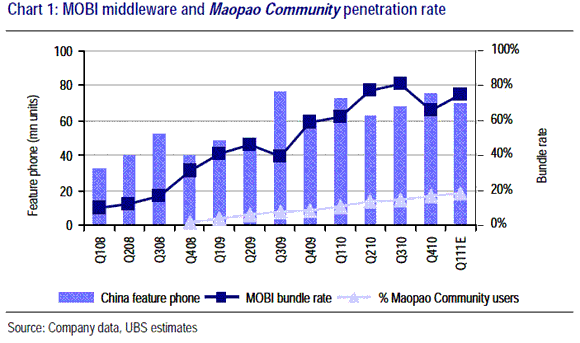

Increasing bundle rate of Maopao platform MOBI’s Maopao platform has been the dominant middleware in China since 2009. In Q310, the bundle rate increased to 80%+ of China handsets, according to the company. Although the ratio dropped in Q410 as operators began to request ‘triple confirmation’ of apps purchases by SMS (as they did in Q309 when operators requested ‘double confirmation’), UBS thinks MOBI should be able to maintain a 75% bundle rate in China going forward. The bundle rate for MOBI’s Maopao Community for mobile on-line games and social networking has ramped up quickly. In Q410, approximately 16% of new handset users in China joined Maopao Community, according to the company. They think the ratio could increase to 30%+ in the next few years.

Expect mobile Internet to be the next focus of handset market

With new handset hardware features limited, improving user experience through software applications is becoming more important to handset vendors. Apple’s ‘App Store’ is the most successful example of selling such apps in the market. In China, UBS thinks domestic companies are better positioned to benefit from growth in the mobile Internet market. They believe MOBI will be one of the major beneficiaries.

Leading position

MOBI has installed its Maopao apps on more than 5,600 handset models. In 2009, it had more than 50% of the market by revenue. Given the industry’s high entry barriers, UBS does not expect new entrants to threaten MOBI’s leading position in the near term.

Notablecalls: As many of you know, Citron Research has been all over MOBI in the past days, causing the stock to drop from $22 to around $14-15 currently. Volume has ballooned up as shorts have established positions in this Chinese name.

Yet now we have a tier-1 firm out initiating coverage calling Sky-mobi Chinese equivalent of Apple ‘App Store’. I’m pretty sure they wouldn’t have initiated coverage if they had ANY doubts regarding MOBI’s #’s. The environment is just too unforgiving when it comes to Chinese names.

I have no idea what the short interest looks like here but judging from the volume it probably stands around 30%.

A short squeeze may be in the cards today.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply