The Automatic Data Processing (ADP) employment survey was weaker than expected in April. It shows that private sector employment rose by 179,000, below consensus expectations for a 200,000 increase. That marks a slowdown from the 207,000 jobs added (as estimated by ADP) in March.

Partially offsetting the disappointment was the fact that the March numbers were revised up from a gain of 201,000 jobs. The gains, however, were widespread, and if confirmed by the BLS on Friday, would still be a solid report.

In March, ADP was a bit on the conservative side, as the BLS reported a total of 230,000 private sector jobs. In January it was far too optimistic, showing a gain of 187,000 and then the BLS only reported a gain in private sector jobs of 50,000 (later revised up to 68,000).

In February ADP was almost spot-on with a forecast of 217,000 private sector jobs added and reported a gain of 222,000 private sector jobs. However that was subsequently revised up by the BLS to a gain of 240,000. In other words, the ADP numbers are generally in the ballpark, but there is still considerable room for the numbers on Friday to be significantly different.

Small, Medium and Large Businesses

Small businesses, defined as those with fewer than 50 employees rose a total of 84,000 jobs in the month. Medium-sized firms, those with between 50 and 499 employees, gained 84,000 jobs while large firms with 500 or more employees added 14,000 jobs. Large businesses are a relatively small share of total employment in the country, accounting for just 17.467 million out of a total of 108.474 million private sector jobs in the country (16.1%).

Small business is the largest source of employment at 49.104 (45.3%) million, followed by medium businesses at 41.903 million (38.6%).

Goods Producing

The goods producing sector added a total of 41,000 jobs. Overall, goods producing industries are not that big a source of jobs in this country, just 17.817 million (16.4%) in total. Employment in goods producing industries tends to be more volatile than in the service sector, and thus the goods producing industries have an outsized influence on the overall strength of the job market.

Goods producing jobs, particularly manufacturing jobs, have been in a secular decline — especially as a share of total employment — for more than 30 years now. Relative to the overall increase, it looks like that trend is continuing. The goods producing sector is made up of Manufacturing, Construction and Mining. While construction jobs did increase during the housing bubble, those jobs were particularly hard hit in the Great Recession.

Construction Employment Improves

Construction industry employment was up by 9,000 in April, only the second gain for the sector since June 2007. Construction jobs peaked well before overall employment in the country, in January 2007. Over that period has shrunk employment by a total of 2.115 million. That is more than one fourth of the total jobs lost in the entire economy since the recession started.

Historically, construction employment (especially residential construction) is one of the first areas to recover when the economy starts to rebound, but that is not happening this time around. With the extraordinary weakness in new home sales in recent months, there is very little reason to believe in that construction employment is going to pick up anytime soon. High vacancy rates in most forms of commercial real estate also means that there is not going to be much of a pick-up in commercial construction any time soon.

Still, just by not being a drag on the rest of the economy, things will start to look better overall. Eventually higher employment is going to lead to higher rates of household formation. That combined with population growth will increase the demand for housing and the massive inventory overhang we have now will be absorbed. That, however, is not a first half of 2011 story, but it could well start to occur late in 2011 or in 2012.

Manufacturing Back on Track

Manufacturing had been a bright spot in this recovery, but it faltered in the fall. It looks like it is getting back on track with a gain of 25,000 jobs in April on top of a gain of 37,000 jobs in March. There were 11.655 million manufacturing jobs, or just 10.8% of the overall private sector workforce.

ADP does not break out mining jobs separately, but given the overall rise in goods producing jobs, we can surmise that the number of mining jobs was up 7,000 on the month. Within the goods producing sector, most of the gains came from the medium-sized firms, which added 26,000 jobs. Large firms added 1,000 while the small goods producing firms gained 14,000 jobs for the month.

Services

The Service sector is far larger, accounting for 90.657 million jobs or 83.6% of the private sector total. It added 138,000, down from adding 164,000 jobs in March. Of the jobs gained in April, 70,000 were added by small service firms, while medium-sized firms added 58,000 and large service firms gained 10,000. Far more people are employed by small service firms, (42.470 million) than by either medium sized firms (34.153 million) or by large sized firms (14.034 million).

Government Jobs Not Included

The ADP report only covers private sector employment, not government jobs at any level. The two series do tend to move in the same direction, and tend to be closer once all of the revisions are in. Government employment has been falling in recent months, particularly at the state and local level, and that trend is widely expected to continue. Thus, if the ADP numbers prove accurate for April, it means that the headline number on Friday is probably going to be around 160,000.

Mixed Signals in Economy

In a normal environment, that might be an OK performance; it is not very inspiring coming out of a deep recession. That level of job growth will not put much of a dent into the vast army of unemployed and underemployed in this country. We have been getting a lot of mixed signals on the economy over the last few weeks, particularly on the employment front.

On the upside, the ISM surveys have been very strong, including the employment sub-index. On the downside, initial claims for unemployment insurance have rebounded back over the 400,000 level. The BLS’s own household survey has (the part from which the unemployment rate is derived) has also been showing far larger job gains than the employment survey in recent months.

Looking Ahead to Friday

The consensus is looking for a gain of 185,000 jobs on Friday, with more than all of the gains coming from the private sector. The ADP numbers should not make a significant change in those expectations.

The consensus is looking for a loss of 15,000 government jobs, mostly at the state and local levels. The apples-to-apples private sector expectations are for a gain of 200,000 jobs on Friday.

State and local governments have been under severe fiscal strain and are likely to be laying off people. The state and local layoffs were 14,000 in March. In February, they were origionally reported at 30,000 but then revised up to 46,000. It would not shock me if the State and Local losses are greater than expected again this month, and/or if the March lay-off numbers were revised substantially higher.

Some governors seem almost gleeful at the prospect of laying off state and local employees these days, particularly if they are represented by a union, and are likely to use job cuts as a weapon to force public sector unions to accept pay cuts and pension reductions to help balance strained state and local budgets.

With a stalemate going on between the GOP house and the Democratic Senate and White House, don’t look for any help to the states from the Federal level. After all, such aid made up about one quarter of the ARRA or Stimulus Plan. Since states are legally not allowed to run operating deficits they either have to raise taxes or cut spending. Raising taxes is less politically popular right now than cutting spending, and the states continue to cut taxes, particularly on businesses.

For the most part cutting spending at the state and local level will mean laying people off, or cutting take-home pay of public servants. The state and local cutbacks are a major source of “de-stimulus” that offsets the stimulus from the ARRA on the Federal side.

From the point of view of the overall economy and aggregate demand, it really doesn’t matter if the spending is coming from the Federal or the State government. (It does matter on a couple of other levels, but not in terms of total demand in the economy). Thus, the total amount of stimulus in the economy is much less than is commonly believed.

Even so, there is going to be a lot less of it going forward than we have had over the last two years. On the other hand, if private sector employment is starting to pick up, and this report clearly points in that direction, then overall incomes will rise, and those States with income taxes will see revenues start to rebound.

Assuming people start to spend more when they have jobs, then sales taxes will also rise. The third major source of state and local revenues, property taxes, are still likely to be strained as housing prices are likely to continue to fall for most of 2011, and that will result in lower assessed values, and hence lower property tax revenues.

Somewhat Discouraging

This was a somewhat discouraging report. It came in below expectations and points to slower job growth than we saw in either February or March. On the other hand, the job gains appear to be widespread, with participation by both the goods producing and service sides of the economy, and all sizes of business participating.

This sort of job growth will not put much of a dent in the vast army of the unemployed, but at least the situation is not getting worse. The unemployment rate has fallen sharply in recent, actually the steepest two-month fall in the unemployment rate since 1958 in December and January, but a big part of it (not all but a big part) was due to a falling civilian participation rate.

And if the economy is really starting to turn around, the participation rate is unlikely to continue to fall, and is more likely to rebound. That would put upward pressure on the unemployment rate even as the economy starts to do better in job creation.

Given the other data we have seen of late, it seems as if job creation should be getting back on track, although the rough weather probably was a factor in holding down job gains during the winter. When the big report comes out on Friday, look at the revisions to the February and March numbers.

In recent months the revisions have been running large and positive. If this report is confirmed by the BLS numbers, a gain of 179,000 private sector jobs is sort of respectable, and would be a good number if we were not in such a deep hole.

In the last jobs recovery, starting in September of 2003 and running through December 2007, on average the economy added just 156,000 jobs per month, and 141,000 private sector jobs (only counting the “good” parts of that period). Since this jobs recovery started in February 2010, we have only been averaging 138,500 new private sector, and 114,800 total new jobs per month, so a private sector total of 179,000 would represent a substantial acceleration.

On the other hand, total employment in March was still 7.26 million below the January 2008 peak (and private sector jobs were 7.04 million lower). At a rate of 179,000 new jobs a month, it would take 39 more months from here before we passed the prior private sector employment peak, in other words July of 2014. Add in a growing population and workforce, and bringing down unemployment to what we thought of as normal before the Great Recession appears to be a glacial process at best.

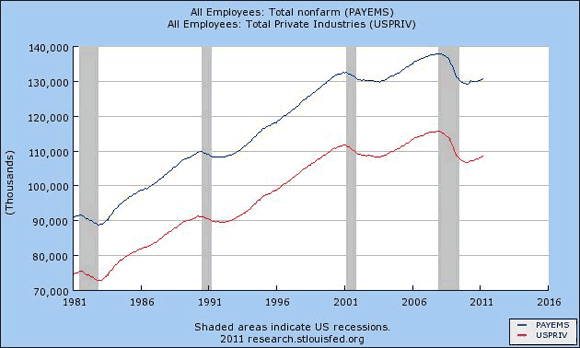

The graph below shows the path of employment, both total and private sector, over the last thirty years. Note that relative to the last two downturns, the increase in private sector job growth has been relatively strong, though not as strong as following the 1982-83 recession — but the decline was also much larger.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply