The collapse in trade has been unprecedentedly severe. This column examines potential explanations. While the global fragmentation of production has increased the responsiveness of trade flows to drops in demand, trade also responds more sharply to GDP during global slowdowns than during tranquil times.

The financial crisis is wreaking havoc on the global economy. In the first quarter of 2009, nominal trade fell by 30% on average relative to the same period last year. The world trade volume is estimated to have fallen by over 15% during this period. The declines have been widespread across countries and products, largely reflecting the sharp drop in global demand.

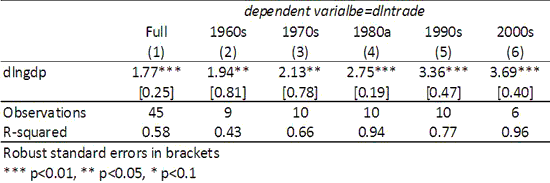

Why has the collapse in trade been so severe? Research on the relationship between trade and income offers some insights. Irwin (2002) estimates that that the elasticity of real world trade to real world income increased from around 2 in the 1960s and 1970s to 3.4 in the 1990s. This would imply that trade growth should decline more than three times as much as GDP growth, assuming crises are not special. In an upcoming paper, I reexamine this relationship and find (like Irwin) that it has increased over time, from under 2 to over 3.5 in recent years (see Table 1). The increase in the elasticity helps explain why trade has fallen so hard in the current global slump.

Table 1. Elasticity of world trade to world income

The significant increase in the elasticity of trade to income may be attributed to the fragmentation of production (Yi 2008; Tanaka 2009). Because many new goods use small inputs that are nearly costless to trade (e.g. mobile phones and digital cameras), the production process of these goods has become fragmented across countries. Many more traditional goods, such as shoes and cars, are also increasingly incorporating imported inputs. The elasticity of trade to GDP will rise if there is more incentive to outsource part of the production chain when demand is high. This is because GDP is a value-added measure while trade is a gross measure. So an increase in GDP may lead to more outsourcing and much more measured trade, as an increasing number of parts travel around the globe to be assembled and delivered to their final consumer. I find the greatest responsiveness of regional exports to global income in East Asia – where a 1% increase in real world income leads to 4.5% increase in real exports since 1995.

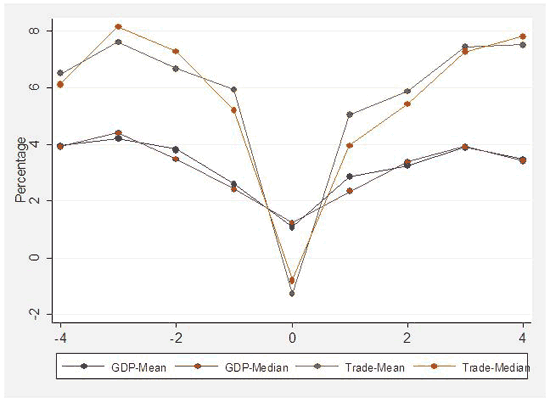

In addition, trade may respond differently to income during global downturns. I also examine real trade growth and real GDP growth in the years around previous global downturns (albeit less severe episodes). Global downturns occurred in 1975, 1982, 1991, and 2001 – in these years, world real income growth dipped below 2% and fell by more than 1.5 percentage points from the previous 5-year average. Figure 1 shows the mean and the median of growth in trade and income during these episodes. I report both to ensure that results are not driven by any particular outlier. Year zero is the downturn year. The decline in growth from the previous year to the downturn year is much larger for trade than for GDP. Income growth declines on average by 1.5 percentage points from previous year, while real trade declines on average by 7.2 percentage points, nearly 5 times as much. On a positive note, the rebound in trade is also very sharp when income expands.

Figure 1. Real trade and real GDP, growth relative to the previous year

Source: World Bank, World Development Indicators and author’s calculations.

Why would trade respond more sharply to GDP during global slowdowns than during tranquil times? There are a number of potential explanations:

1. Firms may draw down accumulated inventories sharply when the forecast worsens in an unexpected and dramatic way.

2. When global GDP drops sharply, protectionist policies kick in, which exacerbate the decline in trade.

3. During downturns, goods decline by more than services, and services make up the bulk of GDP, while goods make up the bulk of trade. Moreover, the share of services in GDP has increased over time exacerbating this distinction.

4. Trade is measured in gross value and GDP in value added. A large decline in trade could reflect a much smaller decline in the value added if production is done across countries at the margin, and as demand falls international production chains break down. For example, Porsche recently announced that it is reducing outsourcing to Finland during the crisis, while maintaining German production (New York Times, 4 April 2009).

5. People may tend to source relatively more from home country suppliers during downturns because of trust or financing problems.

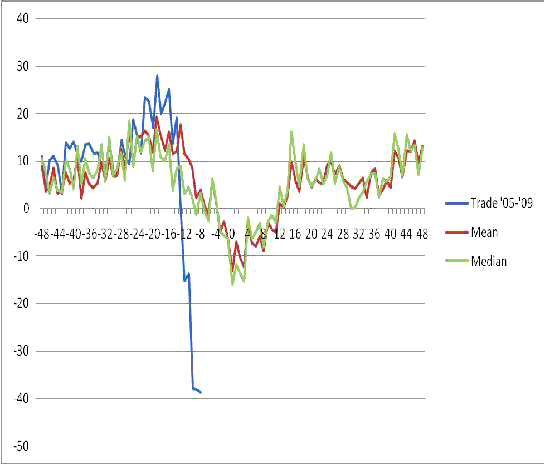

Indeed, trade has fallen fast and furiously since the onset of the financial crisis in the fall. Figure 2 compares trade growth (month over same month the previous year) in this crisis and in the previous downturns, using monthly data in constant US dollars for a balanced sample of 31 countries that report data from 1960 through March 2009. While growth leading up to the crisis was a bit higher in this episode, it still looked quite similar to the previous downturns. What is most evident from the picture is that the trade drop over the last few months has been much steeper and more severe than other recent episodes. This likely reflects the magnitude of this downturn and the increased responsiveness of trade to income in recent years.

Figure 2. The decline in trade, now and then

Source: Datastream. Data in $US for a balanced sample of 31 countries, deflated using the US CPI.

Using an elasticity of trade to income during the downturn of between 3.5 and 5, and a deceleration in real world income growth of 4.7 percentage points (the current World Bank estimate), the deceleration in real trade growth would be between 16-24 percentage points in 2009. World real trade growth in 2008 was about 4%, yielding a contraction in real trade this year of 12-20%. The one silver lining is that trade also tends to rebound sharply when income expands.

References

•Freund, C (2009) “The Trade Response to Global Crises: Historical Evidence” World Bank.

•Irwin, D. (2002) “Long-Run Trends in World Trade and Income” World Trade Review 1: 1, 89–100.

•Tanaka, K. (2009) “Trade collapse and international supply chains: Evidence from Japan” VoxEU.org 7 May.

•Yi, K-M (2008) “The collapse of global trade: The role of vertical specialisation” in The collapse of global trade, murky protectionism, and the crisis: Recommendations for the G20, edited by Richard Baldwin and Simon Evenett.

![]()

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply