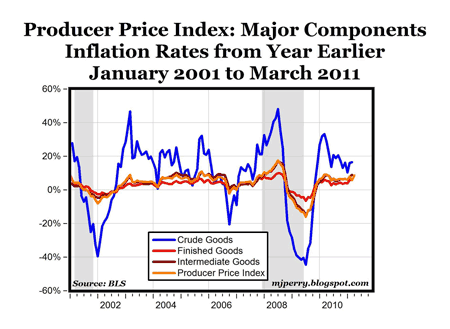

Based on today’s PPI report from the BLS, the charts above are updated from last month’s CD post on producer price inflation where I suggested that it’s hard to make a strong case for producer price inflation when looking at a 10-year history of the PPI and its three main components.

The 12-month inflation rate of the crude material component of the PPI has been trending downward, and is less than half of the rate compared to a year ago, and about one-third the peak for crude material inflation in 2008. The other main PPI components (intermediate goods and finished goods) have turned up a little bit recently at annual rates, but finished goods inflation is below its year-ago level, and both finished good and intermediate inflation rates are still below their levels in 2007, and about the same as their levels from mid-2002 to 2006.

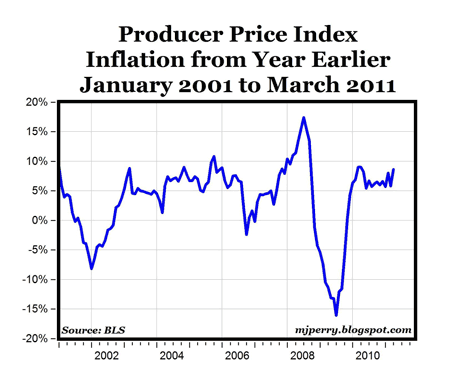

The bottom chart above for just the overall PPI annual inflation rates over the last ten years shows a similar pattern: A slight increase in recent months for PPI inflation, but still below the levels in March and April of last year, below the 2008-levels, and about the same as the 2004-2005 period. And the PPI level of 199.1 in March is still 3.1% below the peak of 205.5 in July 2008.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply