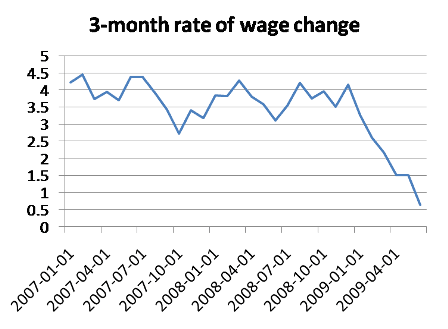

Professor Krugman says we’re heading into Japanese-style deflation territory. He supports his argument by showing a chart displaying the rate of wage change over the past three months — expressed as an annual rate, and by pointing out that “inflation usually runs below the rate of wage change, thanks to productivity growth“. So, deflation time.

If Paul Krugman’s premise proves right, then a U.S. Japanese-style deflation is a crucial debate for economists in determining whether we are headed for a depression-style deflation, or a persistent and problematic economic dynamic in which deflationary pressures keep the economy in a 1970’s style malaise. The debate is also crucial for traders and investors because under both scenarios, particularly the first one, the government bonds will be virtually the only game in town, or better, the only asset class worth owning (having said that however, under a deflationary depression even the safest bonds can go down, at least temporarily) while cash returns will go to zero. These trends (if a deflation scenario materializes) will continue and the process of reversing them will unavoidably be a lengthy one. Prof. Krugman said ” it smells like deflation”, and it certainly does. The reality is we still have a great deal of excess capacity in the world economy because of the overinvestment in capacity by EMs , growth continues to remain extremely weak , if non-existent, and the distress in the labor market is quite evident. So, the possibility of deflationary pressures building in that kind of environment are highly probable. We hope however, that will not turn out to be the case.

Graph: NYT

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply