“China’s overall surge in credit in the first half of 2009,” an article in yesterday’s People’s Daily assures us, “is normal and healthy; however problems still exist in the structure, quality and flow of credit. China should continue to optimize credit structure and guard against potential risks.”

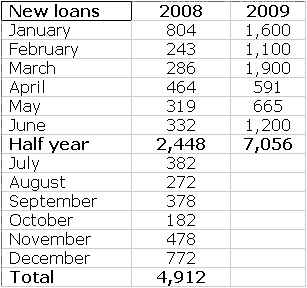

Credible rumors suggest that new loans in June will hit RMB 1.2 trillion or more, as banks rush to inflate their quarterly loan numbers, just as they did in March, on the assumption that any cap in quarterly loan growth will be based on the previous quarter’s numbers. I would argue that new lending in 2009, running at 2 to 3 times the new lending over the same period in 2008, is not at all normal and is very unlikely to be healthy. Here, by the way, is the breakdown for this year and last year (the June number is a rumored projection, so it may change):

Credible rumors suggest that new loans in June will hit RMB 1.2 trillion or more, as banks rush to inflate their quarterly loan numbers, just as they did in March, on the assumption that any cap in quarterly loan growth will be based on the previous quarter’s numbers. I would argue that new lending in 2009, running at 2 to 3 times the new lending over the same period in 2008, is not at all normal and is very unlikely to be healthy. Here, by the way, is the breakdown for this year and last year (the June number is a rumored projection, so it may change):

These are amazing numbers. The People’s Daily article indicates, I think, the schizophrenic attitudes prevalent in China today, with growing nervousness in some circles about the consequences of this explosion in lending riding side by side with a determination to keep it up.

We are going to get 8% growth this year come what may. Since late last year I have been writing about how this everything-but-the-kitchen-sink strategy of throwing everything possible into countering the effect of the global contraction on the Chinese economy might result in higher growth this year and next but will make China’s necessary transition even more difficult and will almost certainly result in much slower growth over the longer term.

I am more certain than ever that this is the correct analysis. The biggest damage is likely to be in the banking sector, which will then create problems in the fiscal accounts. Here is how I see the two greatest risks associated with a sharp rise in NPLs:

1. NPLs are implicitly obligations of the government, whose debt is probably much higher than most of us think and whose commitment to maintaining high levels of growth will result in rising fiscal deficits. In my opinion there is almost no chance that we will not find ourselves worrying about the fiscal position of the government in the next few years. I know this may sound alarming, and it is certainly a little premature, but historical precedents are neither comforting nor forgiving.

2. If NPLs rise sharply, the banks must be protected and recapitalized. Unfortunately this will mean keeping lending rates low, to slow down NPL accumulation, and deposit rates much lower, to maintain banking profitability. As I have discussed many times before, most explicitly in my June 3 entry, low lending rates are one of the most powerful of China’s production subsidies, and low deposit rates, by acting effectively as a significant tax on household income, will significantly constrain consumption growth – basically households will be heavily taxed to protect borrowers and to recapitalize banks, and this cannot help but affect consumer spending. The consequence is that banking policies will be set directly in opposition to the necessary transition that China must make as the US trade deficit continues its long term decline.

Worries about rising NPLs in the banking sector are often brushed off with the claim that the explosion in new lending is implicitly guaranteed by the government so there is nothing to worry about as far as the banks are concerned. Would that were so. Fitch, the ratings agency which seems to be distinguishing itself as the most prudent in its analysis of the banks, has already pointed out that the self-reinforcing relationship between bank credit quality and government credibility, and if government debt is really in the range of 50-70% of GDP, which I suspect it is, I am not sure how much room there is for an explosion in bad debt.

The People’s Daily article also addresses this issue of government guarantee:

Loans secured for government projects mostly rely on “government credibility” – an invisible guarantee offered by local governments. According to data from the Jiangsu Banking Regulatory Bureau, of the loans issued by Jiangsu’s large banks to finance government platforms at all levels, 57.27 percent rely on public finances to repay debts and 49.13 percent are backed by financial commitment letters issued by local governments.

It is often difficult for banks to obtain prompt, comprehensive and correct information about the future disposable financial resources and implicit liability of local governments. If a local government faces financial difficulty, it will undoubtedly affect the quality of banks’ credit assets.

There is, on other words, a distinction between loans implicitly guaranteed by local government and the central government. Already there has been a lot of talk in various finance circles about the fiscal position of local governments, whose revenue sources have been badly hit – and the more desperate they are the more likely they are to guarantee loans. But I don’t know how real the distinction is. Provinces and municipalities are implicitly or explicitly guaranteed by the central government, and in the case of wide-spread payment difficulties I suspect the central government will have to step in anyway.

On this subject let me make a quick detour into history. Edward Chancellor, in his book Devil Take the Hindmost, makes an interesting comment about the famous English Bank Act of 1844:

Under the terms of the Bank Act (also known as Peel’s act after the Prime Minister) the Bank of England’s discretionary ability to issue notes was restricted to a statutory £14 million above its holdings of bullion. A currency tied firmly to gold, argued the bullionists, would prevent over-speculation by defining the limit of credit and offering no escape for the reckless during a crisis. The belief that the government had legislated away financial crises provided many with a false security in the year ahead.

Aside from (I hope) undermining the inexplicably widely-held belief that financial crises occur only in periods of fiat currency, and were unknown during the gold standard days, the real punch line for me is that within just a couple of years of the Bank Act, England experienced an out-of-control railway bubble whose collapse led to the great financial crisis of 1847. It seems that few things are more dangerous than the belief that governments can eliminate or sharply reduce the risk of financial crisis. The idea that a country’s financial system can act as crazily as it likes as long as the government is willing to protect it from its folly runs not only into the problem of undermining government credibility as bad debts surge, but the very belief almost guarantees that the financial system will act in a crazy way.

Can I prove that the Chinese banks are systematically behaving the way banks always seem to under such liquidity conditions? I can’t, and won’t be able to for a few years, but the anecdotal evidence bears terrible resemblance to the same kinds of anecdotal evidence in previous banking crises. For example, last week the People’s Daily had this article:

Three major Chinese lenders said Tuesday that auditors had discovered irregularities in their lending last year, but added that these findings would not affect their financial results. The Industrial and Commercial Bank of China (ICBC), China Construction Bank (CCB) and China CITIC Bank said in separate statements that the National Audit Office (NAO) found some violations of rules in last year’s routine audits. None of the lenders revealed the amount of loans involved in these violations.

…ICBC, China’s largest lender, said in Tuesday’s statement that some of its branches were found to have violated rules in business operations, and some weaknesses in management were also pinpointed.

The bank added it had corrected the violations and had moved to improve risk management and internal controls. The other two lenders said some of their branches had been found to have extended loans against rules or been negligent in supervision over borrowers after the loans were made.

And of course there’s a lot more evidence of credit gaps. Along with a study by a local economist suggesting that an awful lot of new lending was ending up on the gaming tables of Macau (which after all may perhaps be economically more justifiable than further commodity stockpiling), Wei Jianing, a deputy director at the macro-economics department of the Development and Research Center under China’s State Council, worries about money leaking into illegal stock speculation. According to an article in yesterday’s Bloomberg:

Chinese new bank loans worth about an estimated 1.16 trillion yuan ($170 billion) were invested in the stock market in the first five months of this year, China Business News reported, citing a government economist.

That’s 20 percent of the 5.8 trillion yuan loans banks extended in the period, the Shanghai-based newspaper said.

…A further 30 percent of the loans in the first five months may have been used for discounted bill financing, or short-term credits used to fund working capital needs, China Business News said today. These funds may help form a financial bubble, the newspaper cited Wei as saying, adding this is the economist’s personal view.

Stock market speculation is likely to be the least of the worries. At least there is a chance that some of those loans will get repaid. I am not sure this is true of all the other loans being made. In fact I guess I just take it as an iron-clad rule of finance that when bankers are under huge pressure to lend, and especially when there is a perception that someone is willing and able to backstop the risk, every banking system in history has or will behave in exactly the same way.

In that light today’s New York Times had an interesting article on an Argentine private banker who ended up committing fraud at UBS, even after he left to join Chase, with almost laughable ease.

The curious case of Mr. Arbizu, whose career exploded when a Chase customer discovered and reported his crime in May 2007, offers a rare window into this well-shielded world, and raises questions about how carefully some of its largest institutions monitor their bankers.

In telephone and e-mail interviews held in the last eight months, Mr. Arbizu put himself in what he said was the “3 percent of bankers who at some point get confused because of the pressure. We feel like we can take risks that other people don’t even dream to do, and that we can manage that risk — I don’t know why.”

What does this sorry story of fraud have to do with my topic? Perhaps not much, but at the very least it indicates how easy it is even for well-managed banks (ok, stop snickering, UBS is indeed relatively well-managed, but even the best managed banks have never been able to avoid stupid behavior during credit bubbles) to permit, under conditions of rising liquidity and surging financial markets, some very shaky behavior, and I would be utterly shocked if a lot of the same things weren’t occurring in Chinese banks. A lot of analysts like to claim that the credit risk management systems among Chinese banks have improved dramatically. This may very well be true, but it is easily possible for a risk management system to improve from “terrible” to “a little less terrible,” and in the past three weeks I have had conversations with an auditor for one of the Big Four banks and with a foreign advisor who has advised the Chinese government on the setting up of credit risk management systems, and both have totally and without reservation dismissed out of hand the quality of the risk-management systems of Chinese banks.

Under these conditions, and with the amount of what perhaps we can politely call non-credit-related aspects of the lending decision, it is really such an heroic assumption to assume that we are going to see problems in the quality of loan assets? I know it is now very fashionable to dismiss risk management at UBS, Chase and other Western banks, but risk management is still really a lot more experienced and independent at UBS and Chase than at their counterparts here in China.

What makes me worry even more was, paradoxically, the OpEd piece suggesting the opposite by CBRC chairman Liu Minkang, appearing the weekend edition of the Financial Times.

Sometimes the most effective way to address a complex issue is by using basic, simple but useful measures. Practice shows us that traditional tools work, especially considering that financial engineering can malfunction. In recent months we have noticed that many regulators in the rest of the world have also started to embrace this “back to basics” approach.

Much has been written about what triggered the global financial crisis, but in my view it can be attributed to five factors. First of all, the firewall between capital and banking markets was eroded by unsound financial innovations. Second, macro-prudential regulation was neglected. Third, financial institutions had too much leverage and were too opaque. Fourth, incentives for staff at financial institutions were driven by short-term gains, rather than long-term benefits. Fifth, the bail-out put the cart before the horse by pumping in capital and liquidity before cleaning up balance sheets.

There is a long tradition of bankers and regulators waggling their fingers at their fallen brethren in other countries and suggesting that their own practices are much better and should have been more widely copied – just before they find themselves stuck in an even worse quagmire. Although Chinese bankers are probably right to feel annoyed, and just a little pleased, after all the self-important drivel they have had pressed on them by foreign bankers and regulators, still, I would really resist the temptation to hold up China’s system as a model. Like with Japanese bankers in the late 1980s sloughing off Americans and Europeans for their terrible banking practices that were so unlike banking practices in Japan, this is just tempting fate, and Dr. Liu’s five risk factors, and especially the second and the last two, are not exactly foreign to the Chinese banking system.

Before closing, I know I have made a number of references to the 33 A.D. banking crisis in Rome as one of the first recorded cases of a banking panic. I often get questions on it, so let me post here a portion of Chapter 15 from Will Durant’s History of Roman Civilization and of Christianity from their beginnings to AD 325

The famous “panic” of A.D. 33 illustrates the development and complex interdependence of banks and commerce in the Empire. Augustus had coined and spent money lavishly, on the theory that its increased circulation, low interest rates, and rising prices would stimulate business. They did; but as the process could not go on forever, a reaction set in as early as 10 B.C., when this flush minting ceased. Tiberius rebounded to the opposite theory that the most economical economy is the best. He severely limited the governmental expenditures, sharply restricted new issues of currency, and hoarded 2,700,000,000 sesterces in the Treasury.

The resulting dearth of circulating medium was made worse by the drain of money eastward in exchange for luxuries. Prices fell, interest rates rose, creditors foreclosed on debtors, debtors sued usurers, and money-lending almost ceased. The Senate tried to check the export of capital by requiring a high percentage of every senator’s fortune to be invested in Italian land; senators thereupon called in loans and foreclosed mortgages to raise cash, and the crisis rose. When the senator Publius Spinther notified the bank of Balbus and Ollius that he must withdraw 30,000,000 sesterces to comply with the new law, the firm announced its bankruptcy.

At the same time the failure of an Alexandrian firm, Seuthes and Son due to their loss of three ships laden with costly spices and the collapse of the great dyeing concern of Malchus at Tyre, led to rumors that the Roman banking house of Maximus and Vibo would be broken by their extensive loans to these firms. When its depositors began a “run” on this bank it shut its doors, and later on that day a larger bank, of the Brothers Pettius, also suspended payment. Almost simultaneously came news that great banking establishments had failed in Lyons, Carthage, Corinth, and Byzantium. One after another the banks of Rome closed. Money could be borrowed only at rates far above the legal limit. Tiberius finally met the crisis by suspending the land-investment act and distributing 100,000,000 sesterces to the banks, to be lent without interest for three years on the security of realty. Private lenders were thereby constrained to lower their interest rates, money came out of hiding, and confidence slowly re-turned.

This is not totally relevant to China today except to the extent that it indicates how difficult it is for banking systems flush with cash to avoid speculative lending, and how the very fact of their speculative lending then creates the conditions that can bring the whole thing crashing down. There has never been a political or economic system in history that has been able to avoid the consequences of excessive liquidity within the banking system. Even the Romans learned this, and they learned it the hard way, as we always do.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply