Scotiabank is out with a good research report on the impact of surging crude prices on the global economy. In particular, the report states that the effects are being dramatically underestimated by market participants. This is despite the last time crude went parabolic back in 2008, which led to a worldwide recession. The reason the global economy is so susceptible to higher oil prices is because consumers are facing a combination of rapidly rising oil and food prices, creating a double whammy, which automatically decreases available discretionary income. It is estimated that increased food and oil prices have cost consumers an extra $225 billion (compared to late 2008 levels). Furthermore, US households are severely budget constrained. thanks to high unemployment (U-6 16%), no wage growth, and little to no home equity, which has been the traditional cash cushion of the American consumer. Without access to home equity, consumers are less able to whether the impact of increasing oil prices, even for a short period of time. This dynamic will have a severe impact on consumer spending, hence depressing economic growth in an economy, which is still reliant on government life support.

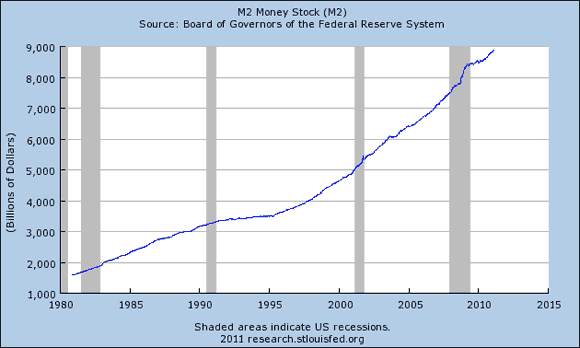

One last thing I need to address. Some analysts and financial pundits have declared that rising oil is actually deflationary. At first glance, I thought this was some kind of bad joke from the likes of Fed-payroll operatives like Steve Leisman on CNBC. But as it turns out, a few serious commentators like Ambrose Evans-Pritchard have argued that same thesis, arguing that rising oil causes central banks to react, which in turn slows the economy resulting in deflation. The idea that rising oil prices leads to deflation is a concept so stupid and misguided that it must have originated from the Federal Reserve Board! After all, in the mind of our dear leader Zimbabwe Ben, anytime asset prices fall it means deflation, which requires more money printing. SP 500 futures down 0.4% pre-market must give Bernanke and Co. a real scare as this is the deflationary spiral coming around the corner to kill us all! Don’t buy into this garbage from the same simpletons who told you in 2007-2008 that the US economy was “sound” and that sub-prime was “contained.” Inflation results from an increase in the money supply and has nothing to do with consumer prices. An increase in money supply (through money printing and excessive credit creation) pushes up prices as there is more money chasing the same amount of goods and services. Take a look at the chart below of M2 (best measure of the money supply since M3 was discontinued) and tell me if it is contracting (deflation). Not a chance with the Fed printing trillions of dollars.

Here is the report regarding oil:

The Potential Oil Impact On Growth Is Being Under-Estimated

5 reasons why the impact of higher oil prices on GDP growth is likely to be greater than the oft-cited lower bound of estimates.

The backdrop against which an oil price shock is occurring is not as severe as it was in 2008-09 when global deleveraging was commencing as jobs were being rapidly destroyed. But the effects of an oil shock on the economy are likely to be greater than the long-run average estimated effects for five key reasons that we explore.

Indeed, the conventional view that oil would have to rise much further for a long period of time before theeconomy incurs painful effects understates downside risks.

1. Uncertain Growth Effects

Half of that shock has arrived since September, thereby concentrating much of the effect on a shorter interval. Indeed, higher oil prices since last Fall chop a half point off US GDP growth, and thus largely offset the possible positive impact of President Obama’s stimulus extension — assuming that US consumers would spend such stimulus to begin with (versus hoarding it), which we doubted.

But studies have shown that the magnitude, lag and duration of the impact of an oil price shock on the real economy is dependent on a number of factors, including the duration (temporary vs. permanent), nature (demand- vs supply-side) and origin (domestic vs. exogenous) of the shock, the type of economy (developed vs. developing, oil-importing vs. oil-producing) and the state of the economy at the time of the shock. For instance, OECD and ECB research tends to argue that the three-year effect of a $10 rise in oil prices involves a cumulative hit to US GDP of about 1%, and less for other countries.

Thus, the $40 rise in oil prices since 2009 would involve a 4% cumulative hit to US GDP over three years. Increasingly more research — particularly in the post 2007-era — focuses on the nature of the shock [1] [2] [3].

While findings agree that higher oil prices due to supply shocks could have a large, adverse impact on global growth, conclusions vary on the effect of the demand shocks. Some believe that they have had limited influence on real GDP [4], while others suggest a more persistent hit [5].

Part of the explanation might be embedded in the dual causality that exists between oil demand and economic cycles [6], but the acuteness of the response also depends on whether the demand shock is domestic or exogenous [7] — particularly in the case of the United States and China — whether the study looks at the short- or long-term impact on the economy in question as well as the size of the shock (1% vs. 10%). Finally, it is worth paying attention to the time period examined by the study, since sensitivity of GDP to oil price shocks seems to have decreased over time [8] [9]. With economies adopting more transparent and credible monetary policies, becoming less reliant on oil in both manufacturing and consumption and reducing real wage rigidity the pass-through effect of oil price shocks to import, producer and consumer prices has diminished over time — particularly since the 1990s — reducing their second-round effect on the real economy.

Due to the factors discussed above, the magnitude — and sometimes even direction — of the impact depends on individual countries and scenarios studied. The negative impact seems to be the biggest on the United States and the smallest on Canada, although oil price shocks seem to contribute positively to Norway’s and Japan’s economies. Digging below the aggregate impact on real GDP, findings suggest that the negative effect of oil price shocks is relatively bigger on household spending and business investment [12] [13], and that their respective price elasticities are likely to get larger with time [14].

2. A Coincidental Oil And Food Shock

Second, historically, oil shocks often occurred in isolation of other consumer-oriented commodity price shocks, until recent years. As chart 2 demonstrates, global household budgets are being strained by the twin oil and food price shocks. In chart 2, we have indexed the trade-weighted UN Food and Agriculture Organization’s index of 55 food prices to the start of 1990, and done likewise for WTI oil. For instance, the early 1990s spike that more than tripled oil prices occurred while global food prices were flat. Indeed, for much of the period until the mid-2000s, food was dirt cheap to much of the world, and prices were going nowhere. Since 2003, however, this index of food prices has risen by a whopping 120%. Growth in emerging market demand for food as tastes broaden out with income growth, rich-world environmental policies oriented toward diverting crop production toward bio-fuel production, financial speculation that treats some commodities and alternative investments interchangeably in increasingly liquid markets, and global government actions toward blocking grain exports and stockpiling food have all combined to drive food prices to record high levels in recent years. If ever there were a time to resurrect the Doha round of global trade talks, developments in recent years offer a compelling case of the need to strike to the heart of trade distortions across developed and developing countries alike.

The combined largely non-discretionary spending categories that are focused on food and energy spending compete for share of wallet against discretionary spending. What American consumers are spending on food and energy as a share of their incomes is not far off 2008 levels. Americans are now spending an extra $225 billion on food and energy now versus after prices had collapsed by late 2008. Food and energy spending had peaked at US$1.497 trillion in 2008Q2, sat just $36 billion below that level as at the end of 2010 and is likely higher now. As a share of incomes, food and energy spending now sits at 12.6% versus the 13.5% peak in mid-2008. This share has risen by taking away over one-and-a-half percentage points of income since the 2009 trough in oil prices.

3. Household Budget Constraints

Third, historical growth sensitivities to oil prices assume historical levels of access to credit and income growth that are unlikely to apply today following a global banking crisis that still leaves credit much tighter than prerecession conditions. This is still a credit-constrained environment marked by trivial job and income growth.

Without stronger income growth or credit to back into, a commodity shock still crowds out discretionary spending and, in our opinion, is disinflationary for much of the rest of the consumer basket — a key argument we advanced in 2008. This crowding-out effect on discretionary spending is likely to raise the estimated impact of higher energy prices on growth — we just don’t know by how much. But the greater the commodity shock, the even greater likelihood that US consumers will save rather than spend stimulus. If they spend it, it’s likely to cover here-today and gone-tomorrow consumption of essentials, while other spending categories suffer.

This is why we doubt the line of reasoning that says an oil price shock must be long lasting in order to negatively impact consumer spending in a material manner. Historically, consumers backed into home equity or credit or income growth to smooth out fluctuations. Now, however, household budget constraints are so tight that the cumulative impact of repeated shocks to household finances — even if short lived — is likely to have a seriously destabilizing impact on consumers and businesses.

4. Limited Impact From Higher Production Levels

The fourth key reason why the actual impact on growth is likely to be materially greater than the lower bound of estimates on the historical effects concerns whether Saudi Arabia and other producers can react swiftly to bring more supply into the market, and thus contain further price upsides. Just because they have more spare capacity to draw upon now than they did when oil prices were high in 2008 doesn’t necessarily mean they will be able to contain upward pressure on prices. Supply-side price elasticities are stickier than this assumption of an automatic reaction implies, and a game theoretic approach to changing quotas within OPEC and across non-OPEC producers makes it unclear whether enough other producers would follow suit — or even contravene possible actions by Saudi Arabia. Further, commodities are notorious for overshooting short-run supply and demand dynamics, and concern over instability in the Middle East would not be swept away by simply raising oil production levels. We simply don’t know what kind of regimes will ultimately dominate the region, but the early signs from countries like Egypt’s military government are not encouraging by way of musing over opening the Gaza border, allowing Iranian naval ships to pass through the Suez canal for the first time in years on their way to Syria and off the coast of Israel, among other moves more radical than generally permitted under the Mubarak regime. One must be extraordinarily cognizant of the potential for developments across the Middle East to unfold in potentially much more destabilizing ways than is thus far apparent — the risk premium in oil will therefore reflect this uncertainty.

5. The Policy Response

How policy makers react to the surge in commodity prices is also key. This is a generalized commodity shock that is focused upon consumers that risks policy responses that could further aggravate the risks. An example is talk of raising rates at central banks like the ECB, just as they did in the midst of the last commodity shock in 2008 when its main refi rate rose to 4.25% in July of 2008 on frankly legitimate fears of a commodity shock sparking rising wage demands, but also on what turned out to be the eve of the severe deterioration in markets and the economy. The policy response to a relative price shock that risks demand destruction may well be materially different from the policy response to generalized inflation pressures.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply