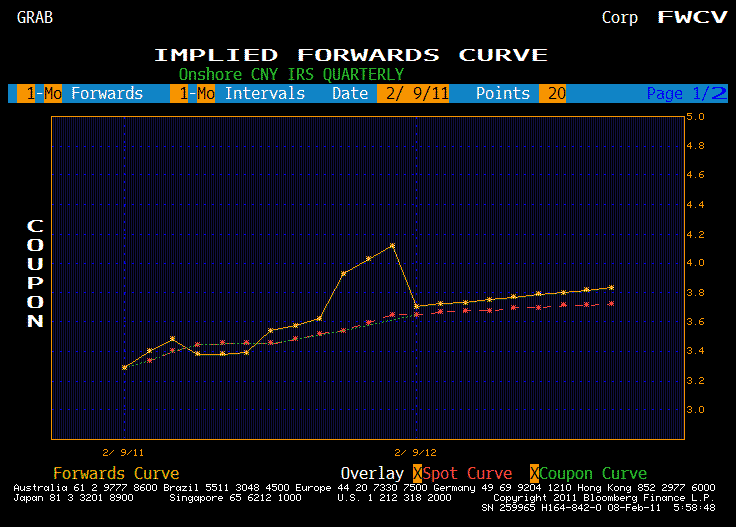

Nice to see Europe keeping things tight in the MRO/STRO allotments and nicer still to see EUR/USD rally (thank the Dark Lord’s followers for their helping hands). But its really the Chinese news that has taken up today. You only need to look at Chinese forward curves (see chart below) to see how massively discounted the news was and the markets reaction, after knee-jerk reactions in the usual suspects, has been pretty muted. So far. As there is a school of thought one of us is entertaining that the news, however discounted, may be enough just to tip the western equity market over from its lofty linear climb we have been following for so long. But it’s a moot point. However it does lead us to consider our general Developed Markets vs. Emerging Markets trade we have had as one of our 2011 Non-Predictions.

(click to enlarge)

A running theme of the past couple of weeks has been the stopping out of consensus trades. As mentioned, One of TMMs trades du l’annee has been the DM vs. EM out-performance trade and whilst perhaps not totally owned in the real money space, we know we are in the company of a fair chunk of fast money. As we have seen the sell-off in rates markets and general improvement to the US macro data, as well as a strong earnings season that showed a move from margin compression to sales beats has supported the foundations of the DM leg and we expect this to continue in the longer run. The EM under-performance bit has been supported by a reluctance to hike rates int he face of inflationary pressures, instead going for macro-prudential credit measures. But as food inflation and related issues have moved to the popular press, and rumors about 5.5% CPI prints out of China, higher than expected inflation prints in Indonesia etc have failed to produce any further sell-off. So just ass Asian CBs have begun to tighten, TMM wonder if we might be passing the peak of the EM inflation worries.

We are reminded of Spring/Summer 2006 when a seemingly dovish Fed and spike in inflation in EM resulted in a generalized risk aversion and EM panic which only ended when the CBs started to hike and get back ahead of the curve. As such we can’t help wondering if we’ve reached this stage again, as the risk premia priced into these assets is ready to tighten.

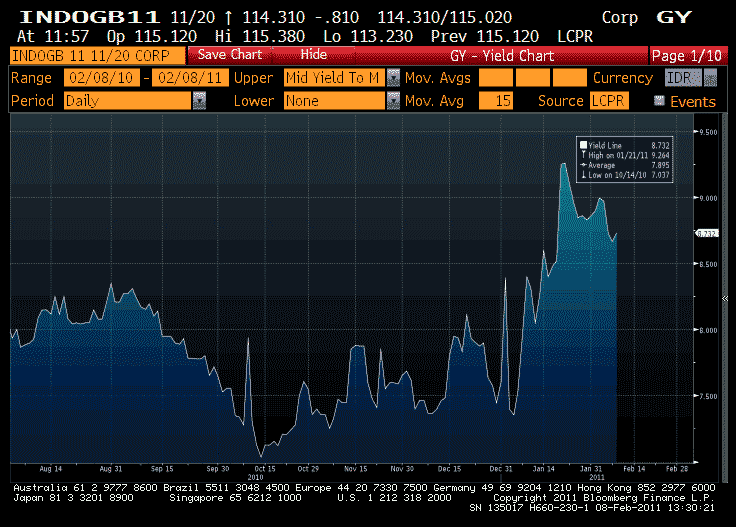

But we also see that not all EM markets are made equal: India and the RBI still seem behind the curve and on a “Fed model” India still looks rich. Similarly, China does not seem to have anyone convinced at this time and a deluge of upcoming IPOs is likely to keep performance weak. Indonesia, however, is showing a lot more resistance and does look like good value in equities and not just their bonds (see chart below). The Philippines also. Brazil, much like China is suffering from political transition and a lack of muscular action on rates and has instead focused on whining about FX. While TMM supports this noble endeavor it is doing very little for risk assets.

(click to enlarge)

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply