In a Wall Street Journal article this past Friday, Stanford economist John Taylor articulated a two-track plan to restore growth. The first track pertains to fiscal policy, but what always attracts our attention here at macroblog are Professor Taylor’s comments on monetary policy, the essential second track in his formulation for economic restoration. Here are the highlights (emphasis mine):

“… the Fed should lay out a plan for reducing its extraordinarily large balance sheet. To achieve a more predictable rules-based policy going forward, the Fed’s objectives should be clarified…

“Recently the multiple objectives [for both price stability and maximum employment] have been used as a rationale for interventionist policies, such as QE2, an approach that Fed officials avoided in the 1980s and ’90s. Such interventions can have the unintended consequence of increasing unemployment—as illustrated by the decisions to hold interest rates very low in 2003–2005, which may have caused a bubble and led to the high unemployment today.

“It would be better for economic growth and job creation if the Fed’s objective was simply ‘long-run price stability within a clear framework of economic stability…’

“The Fed should also be required to report in writing and in hearings its strategy for monetary policy… the renewed requirement should focus on the strategy for setting interest rates. The Fed should establish its own strategy and report it to Congress.”

I bolded portions of those passages because I have some thoughts on them. These are not new thoughts, but I believe they are worth noting again:

- Though all plans are subject to revision and refinement, the Federal Open Market Committee (FOMC) has laid out “a plan for reducing its extraordinarily large balance sheet” and did so some time ago. From the minutes of the January 26–27, 2010, meeting of the FOMC:

- “Staff also briefed policymakers about tools and strategies for an eventual withdrawal of policy accommodation and summarized linkages between these tools and strategies and alternative frameworks for implementing monetary policy in the longer run. The tools for moving to a less accommodative policy stance encompassed (1) raising the interest rate paid on excess reserve balances (the IOER rate); (2) executing term reverse repurchase agreements with the primary dealers; (3) executing term RRPs with a broader range of counterparties; (4) using a term deposit facility (TDF) to absorb excess reserves; (5) redeeming maturing and prepaid securities held by the Federal Reserve without reinvesting the proceeds; and (6) selling securities held by the Federal Reserve before they mature. All but the first of these tools would shrink the supply of reserve balances; the last two would also shrink the Federal Reserve’s balance sheet.”

The minutes go on to explain the options for deploying those tools, actions, and plans (that have since been completed) for ensuring that the tools are operational and agreement by FOMC participants that “raising the IOER rate and the target for the federal funds rate would be a key element of a move to less accommodative monetary policy.”

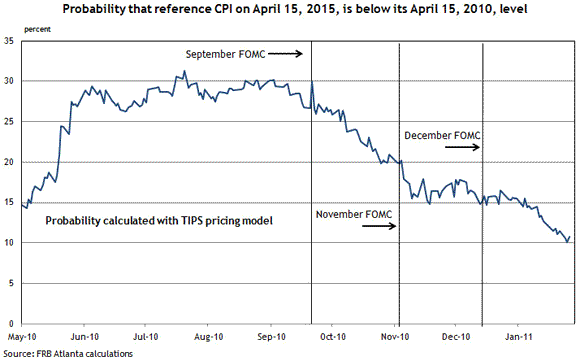

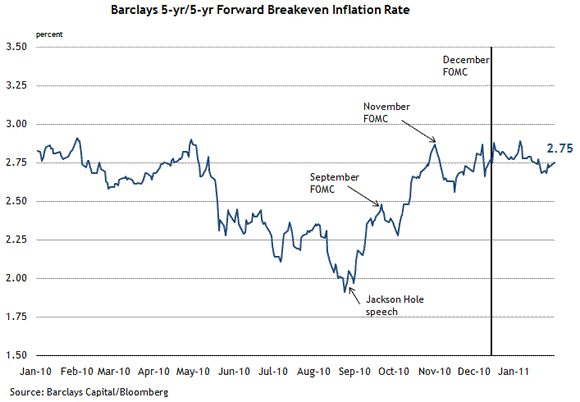

3. Large-scale asset purchases (termed QE2 by some) are in my opinion clearly in line with the Fed’s price stability objective. I have made this point before, but through the summer of last year up to the point when the possibility of more accommodation was signaled by Fed Chairman Ben Bernanke in late August, there was a clear downward tilt to market inflation expectations and a discernable shift upward in the perceived probability of deflation:

Stabilizing inflation expectations is at the core of any central bank’s price stability objective. As these charts clearly illustrate, the concern that expectations were becoming unanachored was real, and the policy, I believe, has been successful in addressing that problem.

Whether the Fed’s so-called dual objectives complicate policy going forward remains, of course, to be seen. But from where I sit, the dual objective/mandate question is a red herring in the discussion of whether QE2 was warranted or not.

4. The notion that the Fed has not established its own consistent strategy in terms of interest rate policy is not supported by the facts. Here’s the Taylor critique, succinctly:

“Economists cite the Taylor rule—which says that the Fed’s target interest rate should be one-and-a-half times the inflation rate, plus one-half times the shortfall of GDP from potential plus one—as evidence that this approach worked…

“Unfortunately, leading up to and during the recent crisis, the Fed deviated from this framework. It held interest rates too low for too long from 2002 to 2005, and after the crisis began to flare up in 2007 it engaged in massive discretionary credit operations.

“So the answer to the question [‘What should the Fed do next?’] is simple: Get back to the rule-based policy that was working before the crisis.”

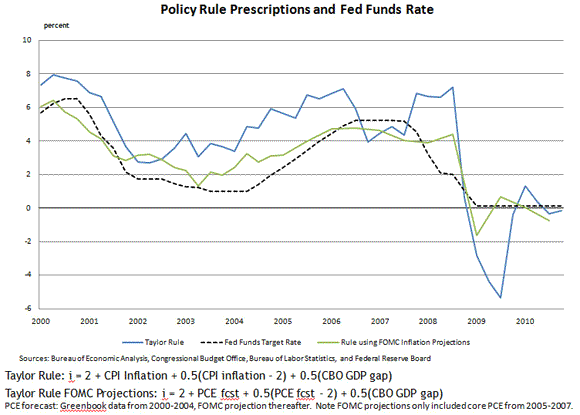

An important issue with this critique, noted by Chairman Bernanke in a speech delivered about this time last year, is that, at least up to the point where the federal funds rate hit its effective lower bound, the FOMC did behave in a consistent rule-based fashion—just not precisely the one preferred by Professor Taylor:

In the chart above, the blue line is a simple version of the Taylor rule, which prescribes that the central bank react to contemporaneous inflation and GDP. But, as Chairman Bernanke explained:

“… because monetary policy works with a lag, effective monetary policy must take into account the forecast values of the goal variables, rather than the current values.”

The green line in the chart above depicts a “forecast-based Taylor rule,” and as can be clearly seen, it is quite a good indicator of the funds rate policy actually chosen—and chosen in a consistent rule-like manner—by the FOMC.

That consistency is certainly no virtue if the implicit rule is flawed. But that brings me to my final point.

5. The theme that runs through many a critique of current and past Fed decisions arises from the assertion repeated in this most recent Taylor piece that “decisions to hold interest rates very low in 2003–2005… may have caused a bubble and led to the high unemployment today.” The evidence presented to date on this count is, in my opinion, tenuous at best. For some perspective, I refer you to Tim Duy, who provides others’ rebuttals, as well as his own. Also, here’s some more perspective, from the Financial Crisis Inquiry Commission Report, which is relevant as well:

“Low interest rates, widely available capital, and international investors seeking to put their money in real estate assets in the United States were prerequisites for the creation of a credit bubble. Those conditions created increased risks, which should have been recognized by market participants, policy makers, and regulators. However, it is the Commission’s conclusion that excess liquidity did not need to cause a crisis. It was the failures outlined above—including the failure to effectively rein in excesses in the mortgage and financial markets—that were the principal causes of this crisis. Indeed, the availability of well-priced capital—both foreign and domestic—is an opportunity for economic expansion and growth if encouraged to flow in productive directions.”

There is no absolution for policymakers in that conclusion. But, I believe there is a warning about carefully separating the baby from the bath water when evaluating past, present, and future monetary policy actions.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply