RBC Capital is making a big call on Corinthian Colleges (NASDAQ:COCO) upgrading the name to Outperform from Underperform with a $6.00 price target (up from $5.00).

– The moves comes after meeting with the company’s new CEO, Jack Massimino, earlier this week.

In RBC’s opinion, the return of Mr. Massimino, who was previously COCO’s chairman and its CEO before that, will be viewed a year from now as an important step in terms of getting the company back on track. They expect that Mr. Massimino will leverage his experience in running public companies in the health care and for-profit education sectors to develop a rehabilitation plan for COCO that stabilizes enrollment and addresses its perilous regulatory position. Firm also notes that they believe investor expectations for the company are excessively pessimistic. Although an investment in COCO is speculative, RBC believes that the risk/reward pendulum has swung in a favorable direction.

Potential Catalysts: 1) Investor confidence in COCO improves due to new messaging focused on quality student outcomes and the provision of a coherent business plan that has tangible operational and financial benchmarks. 2) CY11E enrollment stabilizes at 85,000 (-15% y/y) students. 3) CY11E operating margin exceeds 5% due to cost reduction initiatives. 4) Gainful Employment (GE) regulation is less onerous than expected. 5) COCO is acquired by another for-profit operator or a private equity investor.

Ratings Assessment: RBC notes their rating is consistent with their view that COCO shares will outperform the peer group due to excessively low investor expectations.

Valuation: RBC’s new price target of $6 is based on CY11E EPS of $0.60 and a P/E of ~10.0x compared with a current valuation of ~8.0x and a peer group average of ~10.0x.

Conclusion: They think it makes sense to get in early before COCO articulates and implements a new game plan. Mr. Massimino is an experienced operator with the wherewithal to successfully adapt the business model to the current environment.

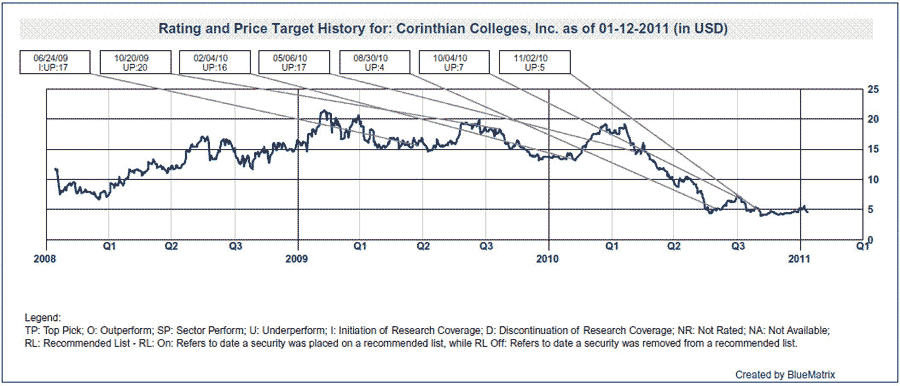

Notablecalls: Robert C. Wetenhall, the RBC Capital analyst might as well be the Axe in COCO. Why you ask? Take a look at this chart:

(click to enlarge)

Wetenhall has been Underperform rated in COCO since 2009. The stock was trading around $20 back then vs. $5 currently. He saved his clients a lot of dough and has Street cred. Lots of it, I suspect.

Now, the call itself is a short one (just 1 pg.) and definitly lacks the oh-so-usual valuation mumbo-jumbo. Wetenhall’s call is purely qualitative – Massimino is coming back & has lots of experience dealing the government. Health-care is highly regulated, as you know.

Couple of more points:

– The whole sector has rebounded sharply over the past week, since the STRA news. COCO has been VERY prone to move on intraday speculation/flow. The stock appears to want to go higher. All it needs is a good excuse.

– Ignore the $6 price target, just ignore it. If Wetenhall is right, this is one is an easy double. If not, then..not. But the price target means nothing here.

I see COCO trading up at least 10% today, putting $5.25-50 level possibly in play. Should go higher after that.

PS: (update 08:20 AM ET) I just checked, Wetenhall appears to be No1 ranked on Bloomberg absolute return ranking.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply