Want to know how the global economy is faring? Look at trade. CAI International, Inc. (CAP) is trading at just 12.2x forward estimates even as container utilization rates continue at a historically high level.

CAI International has a direct link into the world of international trade. It manages and leases intermodal freight containers in 10 countries worldwide. The company has a fleet of 799,500 TEUs.

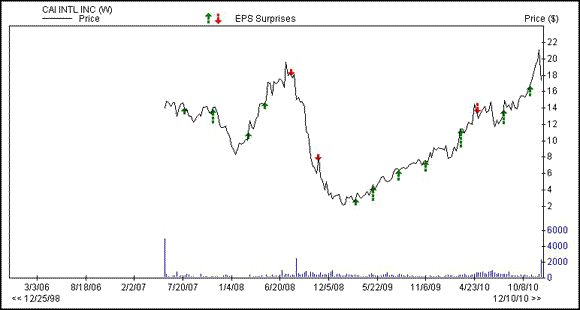

CAI International Surprised by 11.4% in the Third Quarter

On Nov 2, CAI International reported its third quarter results and surprised on the Zacks Consensus by 4 cents. Earnings per share were 39 cents compared to the consensus of 35 cents.

It was the third surprise in the last 4 quarters. There has only been one miss on estimates since the dark days of 2008.

Total revenue rose 27.4% to $20.1 million from $15.7 million in the year ago quarter.Total revenue for the third quarter of 2010 was $20.1 million as compared to $15.7 million for the third quarter of 2009. Rental revenue jumped 23% quarter over quarter.

Utilization was nearly 100% at 98.1%, up from 95.1% in the second quarter of 2010. Peer TAL International (TAL) also saw a 98.1% utilization rate in the third quarter.

CAI also saw the strength continuing into the fourth quarter as a month into the quarter, at the end of October, utilization rates continued to be 98.1%. Again, this is similar to what TAL also said regarding its fourth quarter.

Containers Are Hot

Like TAL International, CAI is adding new containers to meet demand.

It took delivery of 40,500 TEUs in the third quarter and in July 2010 purchased 23,000 TEUs of older units. The company also transferred about 25,500 TEUs of older containers to 2 investor funds in Asia.

On Dec 6, the company announced it was doing a public offering of 2.7 million shares of stock with an aggregate value of $30 million. The proceeds are to go towards working capital and other general purposes, including more investment in containers.

Outlook for 2011 Remains Strong

An industry research service predicted international trade would grow 10% in 2011. Given already high utilization rates, combined with growing trade, CAI expects container demand to continue to be strong in 2011.

CAI expects fourth quarter revenue to continue to grow over third quarter.

Zacks Consensus Estimates Rise for 2010 and 2011

Analysts are bullish about the final few months of 2010 and the outlook for CAI going into 2011.

The 2010 Zacks Consensus has jumped 4 cents to $1.43 per share in the last month.

Analysts expect earnings growth of 80.6% in 2010.

They expect more of the same for 2011, with the 2011 Zacks Consensus climbing to $1.93 from $1.88 in the past month. This would be earnings growth of 35.1%.

Plenty of Value in CAI Shares

Even with the stock up sharply off its recession lows, shares still have attractive valuations.

Along with its value P/E ratio, CAI has a price-to-book of just 1.9, which is well within the range of a value stock.

It also has a nice return on equity (ROE) of 13.9%, well above its peers at 6.1%.

Unlike its peer TAL, however, CAI does not pay any dividend.

Leave a Reply