I often feel caught between two complementary yet seemingly contradictory narratives regarding the US economy, one that sounds very optimistic while the other, in my opinion, pessimistic. Nevertheless, I think both narratives can be embraced, at least to a certain extent. And which narrative the Federal Reserve embraces will determine the dominate monetary policy question: Will the Fed scale up quantitative easing, or scale down?

It is reasonable to conclude that the US economy possess the basis for sustained growth in the quarters ahead. Indeed, the signs of a cyclical upturn are all over the data – manufacturing, investment, retail sales, inventories, take your pick, they are generally moving in the right direction. And my take on the recent spate of data is that economic conditions firmed somewhat as we entered the fourth quarter. The ISM reports, both manufacturing and service sectors, were looking much more solid than the previous months. Initial unemployment claims have drifted downward, possibly even poised to make a sustained break below the 450k mark. And the all important employment report did surprise on the upside.

Overall, the four quarter average of GDP growth is 3.1% – perhaps a bit higher than potential (or perhaps not, given earlier productivity gains), consistent with the relatively steady path of the unemployment rate since the beginning of the year. And note private sector payrolls are rising at a monthly rate of about 112k this year, at the low end of estimates necessary to absorb the growing labor force (albeit acknowledging the potential for additional drag from the public sector). To be sure, during the past two quarters, average GDP growth slowed to an average of 1.9%, threatening to undo these patterns and prompting the Fed to step up large scale asset purchases. But the pick up in activity suggested by the ISM reports signals that growth will edge back up in the final quarter of this year.

Like others, I could find quibbles with the data. For instance, the household side of the October employment report was not exactly inspiring, suggesting that high unemployment continues to drive persons out of the labor force. And the gains on the employment side were concentrated in a handful of sectors – retail and wholesale trade, temporary employment, and health and education services accounted for 123.1k of the 159k total. I would prefer broader based increases, but will hold out hope that the temp employment gains foreshadow a more durable recovery in the months ahead.

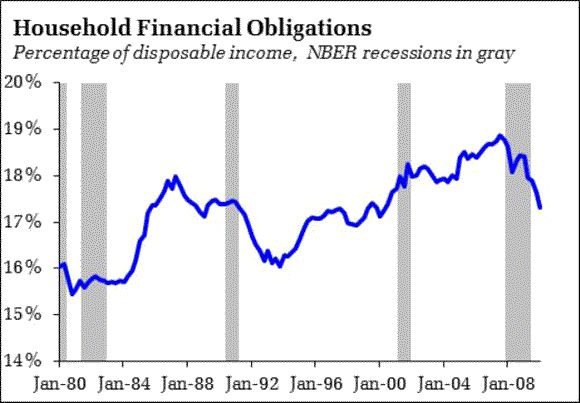

Moreover, I believe households are setting the groundwork for sustained spending growth in the quarters ahead. Not only are savings rates well off their lows, meaning that some or even much of that adjustment is already behind us. And financial obligations have collapsed back to levels last seen prior to the 2001 recession:

Goodness, consumer credit even rose a touch in September! Moreover, steady gains in the labor market would go a long way in supporting the handoff from spending sustained on transfer payments to spending sustained on wages. The net impact might not cause a surge in consumer spending, but it would at least keep it on its recent steady upward trend.

And yes, of course, households are still fundamentally challenged relative to five years ago. Housing markets remain a mess, net worth has been shredded, etc. And these events appear to have made something of a permanent mark on consumer psychology. Witness as retailers rush to get the jump on the holiday shopping season, ratcheting up discounts amid worries that consumers remain frugal and more discerning about their spending. From the Wall Street Journal:

Retailers and manufacturers are slashing flat-screen television prices more aggressively than usual this holiday season in hopes of avoiding a pileup of inventory.

Wal-Mart Stores Inc., Best Buy Co. and Amazon.com Inc. are touting deals ahead of Black Friday to clear out older and cheaper sets before an anticipated flood of deeper price cuts in coming weeks…

…The frenzy is being fueled by such top makers as Sony Corp. and Samsung Electronics Co., which are reducing suggested retail prices and sweetening their promotions with such extras as free Blu-ray movie players and 3-D glasses after initially overestimating the American consumer’s appetite for pricey features….

…Television makers had expected bullish sales for 2010 on the theory that Americans were slowly loosening their purse strings and becoming receptive to new, pricier technologies such as ultrathin LED screens, Internet-connected sets and 3-D TV.

But slow 3-D TV sales and a buildup of U.S. television inventories in August and September showed that Americans were still behaving frugally amid continuing high unemployment…

That said, I think it is importance to recognize that the relative challenges still facing households – namely a loss of asset values and the access to credit those values provided – is more a story of why spending did not quickly revert to trend, not a reason to believe that spending cannot be maintained along its current anemic trend:

Overall, I believe it is reasonable to embrace a story that the economy settles into a trend near potential growth – by some measures, an optimistic outlook. Indeed, I believe this was a story the Federal Reserve was willing to embrace, and would have had it not been for the slowing evident over the past two quarters.

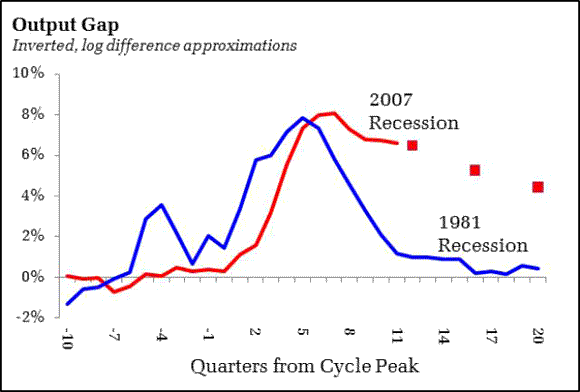

That said, the recent flow of data does little to convince me that the US economy is set to grow much faster than potential. For the sake of argument, supposed that QE2 does in fact support the economy, pushing growth back up to the 3% range in 2011 and 2012. Sales increases, profits increase, jobs increase, everyone’s happy, correct? Probably not. Consider the trajectory of the output gap under such circumstances:

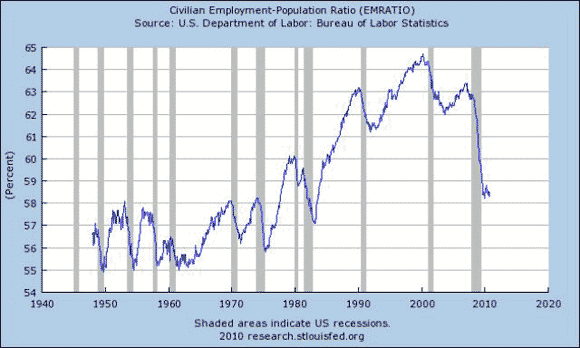

I included the path of the output gap through the 1981 recession cycle, centering both on the begining of the respective recessions. At 3% growth, the output gap will narrow to 4.5% by the end of 2012, 14 quarters after the “end” of the recession. In contrast, in the mid-1980s, it took just 7 quarters to collapse the output gap to just 1%. Perhaps more dramatic is a look back at the employment to population ratio:

The ratio went from 57.1% in January 1983 to 59.9% in June 1984 – just 17 months to return just a notch below the 60% of 1980. The record so far this year? Ten months to get from December 2009’s 58.2% to last month’s 58.3%.

In short, the US economy did not experience a V-shaped recovery, not even close. And I don’t see h ow you get a V-shaped anything at this point. Traditionally, employment would rocket up on the back of inventory correction – which would fuel factory rehires – and housing. But, like in the wake of the 2000 recession, the lost manufacturing jobs appear to be permanent, and housing is…well, that story has been told a thousand times at this juncture.

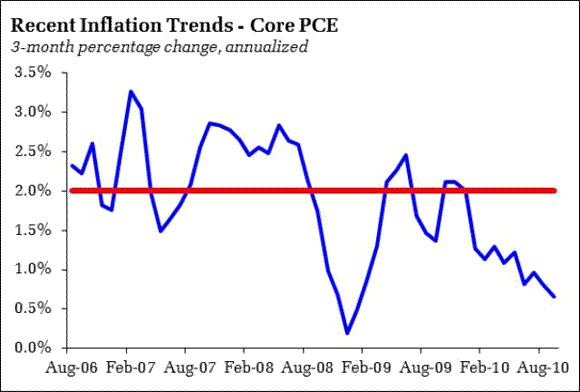

In this narrative, we simply need dramatically faster growth to relieve the stress on the labor market, not to mention to stave off deflationary pressures. Just a reminder, to ensure we are all on the same page on the latter topic:

If the Fed embraces this narrative – that potential growth is not good enough, that potential output should be the target, all else equal, policymakers will feel to compelled to scale up the program to scale up QE2. While opinions vary widely, I am hesitant to believe the Fed has truly engineered a sea change in expectations. I tend to agree with Paul Krugman that Federal Reserve Chairman Ben Bernanke’s objection to higher inflation expectations eliminates a potentially powerful transmission avenue.

But will the Fed embrace this narrative, or will policymakers embrace the notion that they have done all that they can if growth returns to potential growth (or maybe even something less)? Read this week’s speech by Federal Reserve Governor Kevin Warsh. I believe it is a Fed official’s most explicit plea for fiscal help:

Broad macroeconomic policies have not changed direction in the past several years. But change they must, if we are to prosper. In my remarks, I will first venture outside the realm of monetary policy. I do this not in the hope of expanding further the remit of the Federal Reserve. To the contrary–I do this because of the heavy burdens being heaped upon monetary policy. To give monetary policy a chance to be more effective, other key macroeconomic policies–fiscal, regulatory, and trade policy–cannot be working at cross-purposes. So, let me discuss how these policies–some long-in-the-making–might be reformed to restore the purpose and promise of our prosperity. Then, I will return to the conduct of monetary policy….

…We can no longer afford to tolerate economic policies that are preoccupied with the here-and-now. Chronic short-termism in the conduct of economic policy has done much to bring us to this parlous point. Think of your businesses in the public markets–and the harm that can be done to long-term prospects–if you were to do nothing but yield to the whims of analysts and the tyranny of quarterly measures. The best of your firms most surely deliver on your promises to your stakeholders, but your strategic judgments are made with a focus on the long term. You should accept no less from your country’s policymakers.

By now, policymakers should be skeptical of the long-term benefits of temporary fixes– one-off Band-Aids and short-cuts–to do the hard work of resurrecting the world’s great economic power..

Read the speech – it is worth your time. I won’t go through the many details here, and instead will fast forward to his thoughts about monetary policy:

The Federal Reserve is not a repair shop for broken fiscal, trade, or regulatory policies. Given what ails us, additional monetary policy measures are, at best, poor substitutes for more powerful pro-growth policies. The Fed can lose its hard-earned credibility–and monetary policy can lose its considerable sway–if its policies overpromise or underdeliver. We should be leery of drawing inapt lessons from the crisis to the current policy conjuncture. Lender-of-last-resort authority cannot readily be converted into fighter-of-first resort power.

Note that one narrative that emerged during the Great Moderation was that of the omnipotent Fed, the force that could moderate the business cycle via monetary policy alone, compensating for the ineptitude of fiscal authorities. Warsh is rejecting that story. He is throwing the ball back in the court of the fiscal authorities. After describing the Fed’s recent actions, he details the risks:

But, expanding the Fed’s balance sheet is not a free option. There are significant risks that bear careful monitoring by the FOMC. If the recent weakness in the dollar, run-up in commodity prices, and other forward-looking indicators are sustained and passed along into final prices, the Fed’s price stability objective might no longer be a compelling policy rationale. In such a case–even with the unemployment rate still high–the FOMC would have cause to consider the path of policy….

….The Fed’s increased presence in the market for long-term Treasury securities also poses nontrivial risks. The Treasury market is special. It plays a unique role in the global financial system. It is a corollary to the dollar’s role as the world’s reserve currency. The prices assigned to Treasury securities–the risk-free rate–are the foundation from which the price of virtually every asset in the world is calculated. As the Fed’s balance sheet expands, it becomes more of a price maker than a price taker in the Treasury market. And if market participants come to doubt these prices–or their reliance on these prices proves fleeting–risk premiums across asset classes and geographies could move unexpectedly…

…In the United States, the Fed’s expanded participation in the long-term Treasury market also runs the more subtle risk of obfuscating price signals about total U.S. indebtedness. Long-term economic growth necessitates putting the U.S. fiscal trajectory on a sounder footing….

…And overseas–as a consequence of more-expansive U.S. monetary policy and distortions in the international monetary system–we see an increasing tendency by policymakers to intervene in currency markets, administer unilateral measures, institute ad hoc capital controls, and resort to protectionist policies. Extraordinary measures tend to beget extraordinary countermeasures. Second-order effects can have first-order consequences. Heightened tensions in currency and capital markets could result in a more protracted and difficult global recovery. These, too, are developments that the FOMC must monitor carefully.

It is an impressive – and reasonable , in my opinion – list of concerns. One wonders how Warsh sleeps at night. At the risk of oversimplifying Warsh, I would sum these concerns as follows: It is hardly a secret that dependence on the Federal Reserve to be the dominate “stabilizing” economic force has coincided with the development of a nasty dynamic. During the past two cycles, the full employment came alongside an asset price bubble. And, arguably, all we are doing now is sitting around waiting for the money sloshing around in the financial sector to gain a little traction somewhere, and follow the resulting torrent where it leads.

But we shouldn’t kid ourselves. Flooding the market with money is dangerous business. It risks distorting prices and capital allocations. We simply don’t know where the money will wash up. I know that is in vogue to believe there is a nice, obvious story that links an increase in the money supply to an increase in nominal GDP, but that only works on paper. In the real world, the paths between money and output and prices are complicated. The ultimate composition of aggregate demand matters. It matters a lot – distortions have consequences. Warsh’s risks amount to a laundry list of the possible distortions that might occur as the result of ongoing quantitative easing. And he clearly takes those risks seriously.

It makes me think that I haven’t been taking those risks seriously enough. But when monetary policy is the only game in town, what choice do you have? You do what you can up to a point…but then you throw it back to Congress and say “you take responsibility for the mess you created by abdicating your role in crafting long run, stabilizing macroeconomic policies.” Warsh has set the stage for doing exactly that.

Of course, seriously, if we really have to throw this back to Congress, we are absolutely done for. Cooked. Toast. Somebody remember to tell the last guy to turn off the lights on his way out. Better to take our chances with the next bubble.

Bottom Line: One can tell a seemingly optimistic story – the threat of the double dip is behind us, setting the stage for a nice return to potential growth. But that story holds the dark side of persistent, pernicious low levels of labor utilitzation. Still, I think now the Federal Reserve would have chosen the optimistic narrative had it not been for the obvious slowdown midyear. Which suggests to me they are not eager to do more, especially if growth settles back in at trend. Reinforcing that belief is the Warsh speech, which makes a strong case that further monetary policy is increasingly ineffectual and very risky. But even more important, he makes clear a belief that only Congress and the Administration have the tools to restore growth. I imagine if that view is, or becomes, a widespread opinion among policymakers, we have seen the last gasp of quantitative easing. They have abated the financial crisis, serving as the lender of last resort, and flooded the economy with cash. They have done what they can. The rest is up to the fiscal authorities.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply