Osiris Therapeutics, Inc. (OSIR) has analysts buzzing over the prospects for the next couple of years. Estimates are surging after the third consecutive earnings surprise.

But is that enough of a reason to jump into this biotech company, which also carries a Zacks #1 Rank (Strong Buy)?

Company Description

Osiris Therapeutics is a stem cell company that develops products to treat inflammatory, autoimmune, orthopedic and cardiovascular conditions. The company has commercial rights to 2 drugs in the U.S. and Canada, with the rest of the globe belonging to its strategic partner Genzyme.

Better Than Expected

On Nov 5 Osiris Therapeutics said it earned $4.5 million in the third quarter, up from a $6.8 million loss. Revenues were up marginally to $10.8 from $10.6 million, primarily due to licensing fees.

Earnings per share came in at 14 cents, a dime higher than the Zacks Consensus Estimate. Osiris Therapeutics also has about $77 million in cash and receivables.

Potential Home Run

Investors looking at companies in this or similar fields are often at the mercy of regulatory agencies. Osiris Therapeutics is no exception. But in the most recent quarter the CEO commented on the progress towards getting the world’s first stem cell therapy.

However, it should be noted he did not give a timeline. Also, Osiris Therapeutics is particularly risky, given that the company’s primary drug, Prochymal, has failed to pass Phase III studies twice now.

But Analysts are Optimistic

The Zacks Consensus Estimate for this year and next year popped on the earnings release. Forecasts for this year are up 22 cents, to 36 cents.

Projections for 2011 are up 43 cents, to 44 cents. Osiris Therapeutics lost 72 cents per share last year, so this is quite a turn around.

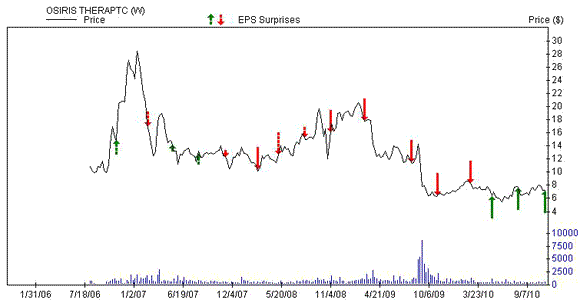

Earnings History

Osiris Therapeutics has topped forecasts in the past 3 quarters after falling short 9 consecutive times. Could this be the a sign that the company is turning the corner?

Leave a Reply