According to the New York Fed, “Research beginning in the late 1980s documents the empirical regularity that the slope of the yield curve is a reliable predictor of future real economic activity.”

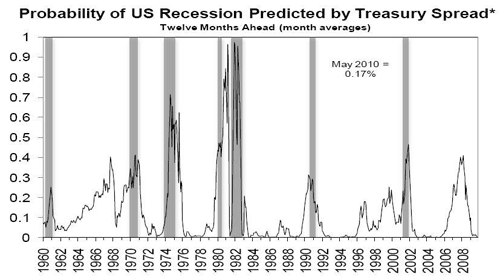

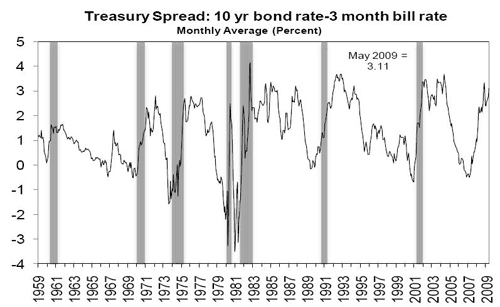

The New York Fed just released its latest “Probability of U.S. Recession Predicted by Treasury Spread,” with data through May 2009, and the Fed’s recession probability forecast through May 2010 (see chart above, click to enlarge). The NY Fed’s model uses the spread between 10-year and 3-month Treasury rates (currently at 3.11%) to calculate the probability of a recession in the United States twelve months ahead (see chart below of the Treasury spread, click to enlarge).

The Fed’s data show that the recession probability peaked during the October 2007 to April 2008 period at around 35-40%, and has been declining since then in almost every month (see top chart above). For May 2009, the recession probability is only 1.54% and by May 2010 the recession probability is only .17%, the lowest level since June 2005.

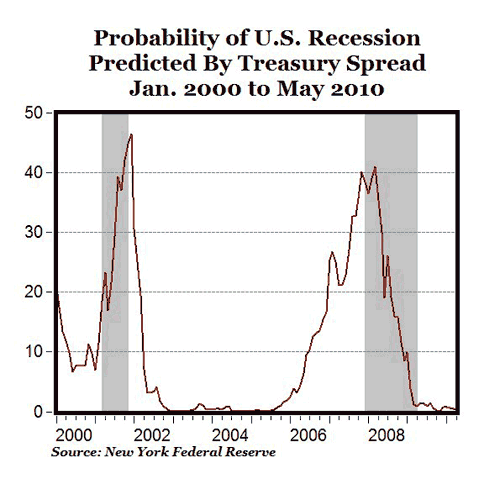

Further, the Treasury spread has been above 2% for the last 15 months, a pattern consistent with the economic recoveries following the last six recessions (see chart above). The pattern of the recession probability index so far this year (going below double-digits and declining monthly) is very similar to the pattern starting in March 2002 that signalled the end of the 2001 recession (see chart below).

Bottom Line: Looking forward to next year, there is almost no chance that the recession will continue into 2010. Further, my reading of the New York Fed’s Treasury spread model suggests that an economic recovery is probably already underway, and the Fed’s model predicts the end of the recession in 2009.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply