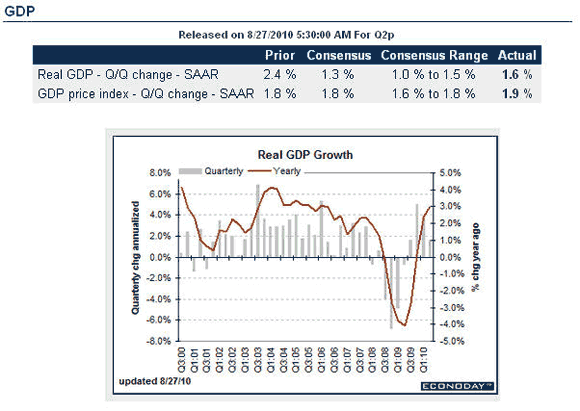

I may have scooped The Onion with this headline. Revised GDP ay 1.6% beat the expectations of 1.3%, although fell below ZH’s revised revision at 1.8%, but what caught my eye was this from MarketWatch:

Wall Street appears to have been caught off-guard by an upward revision to electricity and natural-gas usage figures, which led to an increase in real personal consumption to 2% from the 1.6% initially projected.

A simple explanation, offered by Bank of America Merrill Lynch’s Neil Dutta: households ran their air conditioners longer because of warmer-than-average temperature.

The best news was the increase in business spending to replenish capital equipment, but the recent weak durable goods numbers suggests that trend may not continue into the Q3 number.

The best bad news was that imports surged even more than in the prior report, to the best growth since 1984, which has a damper on GDP (the net of exports less imports is added to GDP), but that is likely stocking up for all those gadgets expected to be hot this Christmas, and is also unlikely to continue in Q3. Put into GDP numerology, real domestic purchases grew 4.9%, up from 2.9% in Q1, but real sales of domestic product grew only 1%, a drop from 1.1% in Q1. This means domestic demand is there, and if we get a drop in imports relative to exports in Q3, it might bolster the Q3 number – so look askance at predictions of a double-dip as early as Q3.

Nonethelesss Goldman Sachs sees a slightly lower Q3 number, largely driven by inventory rebalancing still being high; as it lessens the GDP is lowered.

The biggest risk to their revision is their assumption about fixed residential investment expanding at 27%, which seems nuts based on recent housing news. It has also been an area of over-estimation in past reports that led to downward revisions.

Bernanke’s speech was a bit of a dud, especially when he admitted that “central bankers alone cannot solve the world’s economic problems.” Why we would believe in Fed omnipotence is a topic for another day, but suffice to say the Fed claims it has more bullets to fire at the problem even as it confesses it is running out of ammunition. PragCap gives the Cliff Notes version:

- Bernanke sees no double dip (he also saw no housing bubble)

- Bernanke believes QE2 will “be effective in further easing financial conditions.” (Historical evidence and lending data shows that QE is a non-event)

- His two ideas that have everyone all excited this morning are: (1) changing his wording (which will do absolutely nothing for Main Street even though it might get Wall Street all excited for a few hours) and (2)he will cut the interest on reserves a whopping 25 bps (25 bps isn’t changing anything at this point Mr. Bernanke)

- Bernanke is oblivious to the fact that he has run out of ammo: “The issue at this stage is not whether we have the tools to help support economic activity and guard against disinflation. We do”

The market has ratcheted around a bit this morning, which has emboldened bulls. The expectations game applies to GDP as well as earnings(!), yet the market in the short run tends to be driven by technicals not fundamentals, so too much can be made of momentary jinks and jives due to a news event. Later I will post on the wave structure, which anticipated the sort of sideways move we have seen over the last three trading days.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply