I didn’t think I would be writing this post so soon after the last one I wrote about Ford (F) and the one I wrote last night about GMAC but here we are. The WSJ has a pretty satirical article about the likelihood of the government taking over GMAC.

GMAC differs from other companies under the government thumb because it isn’t too big to fail. So the government doesn’t need to save GMAC to safeguard the financial system.

Instead, GMAC must be saved, the argument goes, to revive the auto industry and consumer economy. The details of that approach are strikingly scarce. In fact, nearly everything about GMAC — its mission, board, and future ties to government — is unknown. As Winston Churchill might put it, GMAC is a financial black hole stuffed into a governance black box.

These details matter. The Treasury is in the middle of a plan to turn privately held GMAC into a new über auto-lender, financed with taxpayer dollars and likely falling under taxpayer control. This has the potential to spark unintended consequences across the auto and banking markets, similar to the quasigovernmental meddlings of Fannie and Freddie.

Would this government-sanctioned company have an unfair funding advantage against Ford Motor’s Ford Motor Credit, for instance? Would it be willing to do the politically unpalatable work of cutting credit to certain car dealers? What happens if Congress starts mandating low-cost auto loans?

Oddly, Congress and the rest of the country seem to have grown numb to the bailouts. Not once has GMAC been discussed substantively in a congressional hearing.

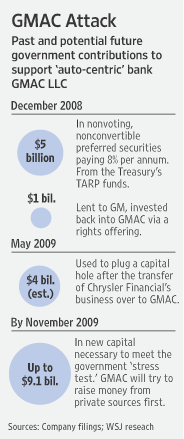

So here are the basics: GMAC is set to receive two new injections of government capital. The first is expected to come by Friday, when the government will back up GMAC after it takes on the business once written by Chrysler’s Chrysler Financial. This could cost the government about $4 billion, says a person familiar with the matter, though the final number isn’t set.

The second step is to fill an $11.5 billion capital hole identified in the government “stress test” last week. GMAC’s existing capital is around $22 billion, a figure battered by years of bad real-estate loans.

GMAC differs from other companies under the government thumb because it isn’t too big to fail. So the government doesn’t need to save GMAC to safeguard the financial system.

GMAC differs from other companies under the government thumb because it isn’t too big to fail. So the government doesn’t need to save GMAC to safeguard the financial system.I said earlier, that the Obama administration had over-committed to the rescue of the auto industry. Hamstrung by their debt to the UAW, they seem never to have considered the consequences of the road they chose to follow. Apparently, alternatives were to complete salvation of Chrysler and GM (GM) were never considered and consequently all they can do is dig the hole deeper.

The Journal sums this up well:

Put it together and what have you got? A bank potentially owned and regulated by the government. One that is embarking on an ambitious merger in a troubled industry, directed by a board in flux. Looming above are a Congress and White House that have expressed little public care for strategy or accountability.

Congratulations, indeed, taxpayers.

Congratulations indeed. No good is going to come of this path. In all likelihood, Ford a viable competitor will be sucked into the vortex that’s developing as will numerous suppliers. This strategy has the earmarks of a disaster. I would like to say that it’s not too late to reconsider strategies but you and I know better. Politics has trumped any chance of reason prevailing.

Update: This is gnawing at me. By nature I don’t tend to buy into conspiracy theories, so I’m reluctant to pursue this theme but I will for the sake of convincing myself there is nothing there.

The entire GMAC episode has been bizarre. Somehow, someway the company keeps on breathing while similar companies expire. It’s mortgage operation was arguably one of the worst in the business and probably has enough embedded future litigation liability to render it insolvent, yet it not only continues to exist but is bailed out at every turn.

The Fed insisted on a debt for equity swap as a condition to approval as a bank holding company and access to TARP. After repeated attempts met with failure, the Fed approved the BHC application despite the fact that it was not recapitalized according to the stipulated plan. One member of the Fed’s Board of Governors voted against granting the company BHC status arguing that it shouldn’t be used as a tool for bailouts.

The FDIC has so far refused to use its authority to guarantee any new debt issues by GMAC despite having been quite accommodating to the rest of the banking sector. As the Journal points out, the FDIC has reportedly said that it isn’t in the business of bailing out auto finance companies. Maybe some political hardball there, and certainly a backhanded way of saying that the whole Fed approval was a sham, nevertheless a rather odd response from an agency that’s been playing ball so far.

Given that all of this occurred during the transition from one administration to another, it is harder to see some grand scheme. Perhaps it’s just nothing more than government groping for any solution that lets it avoid the hard choice.

Like I said, I’m not into conspiracy theories. But this one sure smells.

Graph: Wall Street Journal

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply