Steven Madden (SHOO) is pressuring its all-time high as earnings estimates continue to climb on the heels of a record-setting quarter.

Company Description

Steven Madden makes footwear and accessories for the entire family through owned and licensed brands.

Net Income up 63%

On Jul 29 Steve Madden reported second quarter results that were driven by a 36% jump in sales, to almost $159 million. The company’s operating margin also continues to improve, this time up 360 bps to 20.2%.

Both of those factors lead to an impressive 63% jump in net income, to $19.8 million, or 70 cents per share. A year ago the company earned $12.1 million, or 44 cents per share.

The quarter set company records for both sales, net income and was the third consecutive earnings surprise, topping the consensus by 13 cents.

Bullish Outlook

Steve Madden raised their full-guidance and said they are on pace to meet their goal of doubling earnings per share by 2014.

Analysts, who were tapering estimate into the report, quickly changed their tune after the press release. All 5 analysts raised their forecasts for this year and next year.

The full-year Zacks Consensus Estimate for 2010 is up 15 cents to $2.56, a 41% growth rate. Next year’s projections are up 14 cents on average, to $2.84, for an 11% growth rate.

Valuations & Comparisons

Shares are currently trading at just 15 times forward earnings. Those growth rates are a decent value as the PEG ratios is 1.0. The shoe industry is the 16th rated, out of 264, on Zacks.com and Steve Madden is atop the group of 14.

The company is well ahead of its peers with a 11.7% net profit margin, compared to the industry average of 8.0%. Steve Madden’s ROE is coming in just under 25%, about 900 bps higher than the norm for its peers.

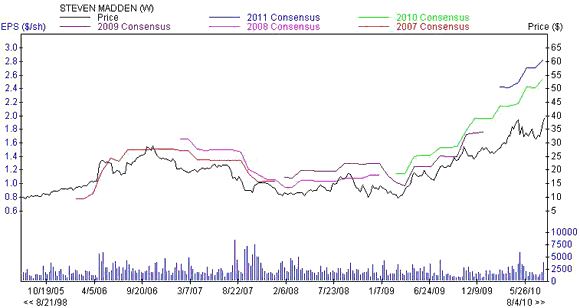

The Chart

Since early 2009 the Zacks Consensus Estimates for Steve Madden have been improved sizable and, just as important, consistently. SHOO is now just off of its all-time high, set about 3 months ago.

Leave a Reply