Many observers, including myself, have been puzzled by the Fed’s lack of urgency in recent months over the apparent slowing down of aggregate demand. The one thing monetary policy is capable of doing is stabilizing total current dollar spending, but it isn’t and this inaction effectively amounts to a tightening of monetary policy. There have been many reasons given for this seeming complacency by the Fed: internal divisions over policy, fear of political backlash, opportunistic disinflation, fear of awakening bond vigilettentes, and sheer exhaustion. Another potential reason is that the Fed simply doesn’t see this aggregate demand slowdown in the data. I actually considered this possibility some time ago but never put too much weight on it since this is the Federal Reserve after all. It has far more resources than I do and surely sees what I see in the data. However, after Fed Chairman Ben Bernanke’s speech yesterday I am beginning to wonder if the Fed is actually missing something in the data. In particular, I was stunned to read this sentence in the speech:

Meanwhile, measures of expected inflation generally have remained stable.

Uhm, unless I have been living in parallel universe and just got phased into this one this statement is completely wrong. Inflation expectations, as I show below, have been persistently declining since the start of 2010. Not only that, but Bernanke’s claim that inflationary expectations are stable has huge policy implications. It is widely understood that expectations of future inflation are a key determinant of current aggregate demand. If expectations of inflation are stable as Bernanke claims then aggregate demand growth should also be relatively stable. On the other hand, if inflationary expectations are falling and have been doing so for some time as I claim then it is likely that current aggregate demand growth also has been falling.*

If Bernanke really believes inflation expectations are stable then one must give him credit for implementing monetary policy in a manner consistent with that understanding. However, I simply cannot understand how he or anyone else at the Fed could hold such a view. The best indicators of inflation expectations have been screaming red alert for some time now. How the Fed could have missed this red alert is unfathomable to me, but on the off chance that they have and are reading this post I ask that they please take note of the following set of figures.

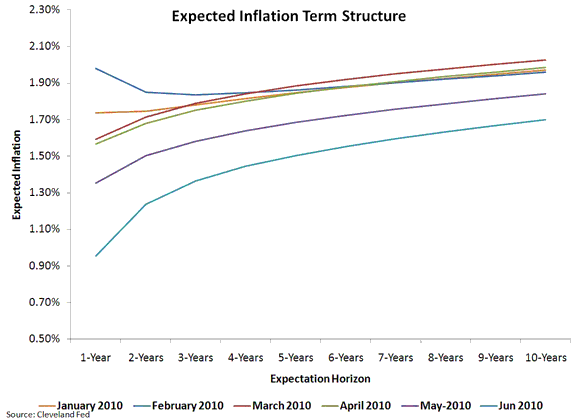

The first figure shows the term structure of expected inflation over the first half of 2010. The plotted curves in the figure show the average expected inflation rate at various yearly horizons for the first six months of 2010. The data comes from the Cleveland Fed. This figure makes clear that inflation expectations have been trending down across all horizons since the start of the year. Note that the 1-year horizon has seen inflation expectations drop by about 100 basis points.

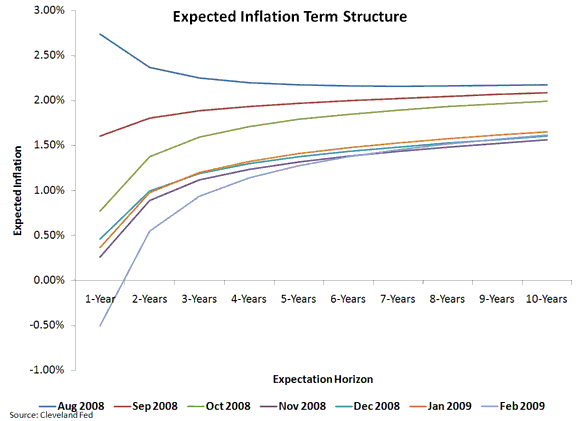

Now to put this figure into perspective let’s look at the term structure of inflation expectations the last time expected inflation fell rapidly and caused aggregate demand to tank. Yes, that would be the late 2008, early 2009 period. Here is the figure for this time. Notice any similarities?

Here too we see a decline across all horizons with the 1-year having the sharpest decline. Now current inflation expectations have not fallen as much as these above but they are persistently falling. And we know from the late 2008, early 2009 experience what happens to aggregate demand when inflation expectations are allowed to continue to fall: you get the greatest decline in nominal spending since the Great Depression.

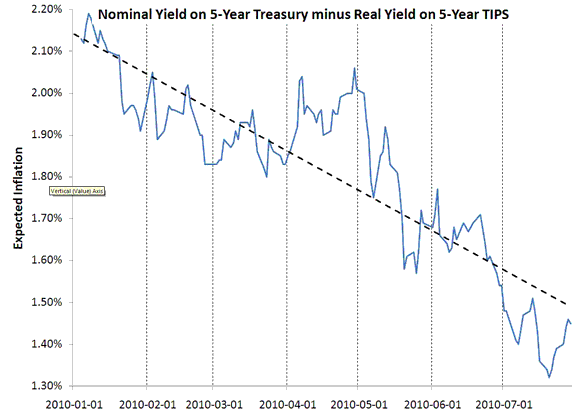

Now the dire picture painted by the Cleveland Fed data is wholly corroborated by the inflation expectations implied by the the difference between the nominal interest rates on regular treasury securities and the real interest rates on treasury inflation protected securities (TIPS). This measure of inflation expectations is graphed below using daily data on 5-year treasuries for the period January 4, 2010 – July 29, 2010:

Here again there is a clear downward trend. Inflation expectations are falling and there is currently no end in sight. Given all of this evidence, how can Ben Bernanke assert that inflationary expectations are stable? I am truly bewildered by that claim. I hope Fed officials who have read this far are also bewildered and are now reconsidering their views. Let me be very clear what all of this implies: by failing to stabilize inflation expectations the Fed is effectively tightening monetary policy at a most inopportune time. I hope this is not how the Fed wants to be remembered.

*It is also possible that expectations of robust aggregate supply growth could be pushing down expected inflation. In 2009 this may have been the case with rapid productivity gains, but in 2010 the productivity growth rate has seen a marked decline. Thus, it is unlikely this is making any meaningful contribution to the decline in expected inflation over the first half of 2010.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply