Are the solar companies finally making a comeback? ReneSola Ltd. (SOL) recently announced preliminary revenue results for the second quarter that was better than its previous estimate and said strong wafer demand continued in the second quarter.

It’s been a long wait for the solar companies which saw demand fall off a cliff during the global recession.

ReneSola is a Chinese-based manufacturer of solar wafers and provides OEM solar module services. Founded in 2005, it has grown quickly.

In May 2009, it acquired Chinese-based JC Solar, which is now a wholly-owned subsidiary.

The acquisition gives the company the ability to provide solar products throughout the entire chain, including polysilicon feedstock, monocrystalline and multicrystalline ingots and wafers, solar cells and modules.

The company is not limited to China as it has customers around the world.

Preliminary Revenue Results Higher Than the Prior Guidance

On July 1, ReneSola announced preliminary second quarter results and gave an updated second half guidance.

Revenue is expected in the range of $245 million to $255 million which exceeds the prior guidance of $230 million to $250 million. It is also up 21% to 25.8% from first quarter revenue of $206.6 million.

Gross profit margin also is projected to jump to the range of 28% to 30%, far exceeding its previous guidance range of 21% to 23%.

Total solar shipments also exceed the company’s prior range as it is projected to be 250 megawatts (MW) to 260 MW, up from 230 MW to 250 MW. Like the other preliminary results, it is also expected to be higher than the first quarter by 3.1% to 7.3%.

“The strong demand for high-quality wafer products witnessed during the first quarter of 2010 continued through the second quarter as a result of ongoing tightness in the wafer supply chain,” said Li Xianshou, chief executive officer.

“We expect to see stable pricing in the coming months as demand has remained strong and is expected to continue in the second half of 2010,” he added.

ReneSola is expected to report second quarter results on Aug 9.

Second Half Outlook

The company also provided guidance for the second half of 2010 along with its preliminary results. Solar shipments are expected in the range of 600 MW to 650 MW.

Revenue is forecast between $550 million and $570 million with gross profit margin between 28% and 30%.

Zacks Consensus Estimates Soar

Given the bullish preliminary results, it’s not surprising that analysts moved to raise estimates for the second quarter and the full year.

3 out of 5 estimates moved higher in the last 30 days for the second quarter, pushing the consensus up 7 cents to 32 cents.

The 2010 Zacks Consensus jumped 28% to $1.10 from 86 cents in the last month.

Analysts are less certain that this solar recovery is real going forward however. While the 2011 consensus also rose by 10 cents to 92 cents, this is an earnings decline of 16% compared with 2010.

Still, these numbers look a heck of a lot better than 2009 where ReneSola lost 86 cents per share.

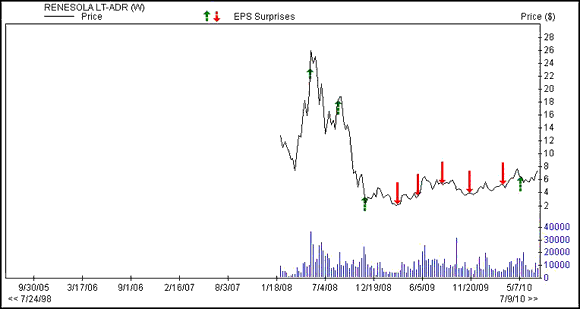

Earnings History Tells The Tale

ReneSola’s earnings surprise history is not good. As you can see from the chart below, since the company went public, it’s been mostly misses, including 3 out of the last 4 quarters.

But the company beat by 27.3% in the first quarter. Is the turnaround finally here in the solar industry?

ReneSola Is Cheap

ReneSola is a value stock at these levels as investors are still jittery about the solar sector, in general.

It is trading at just 6.9x forward earnings, which is well under its industry average of 11.4.

Its price-to-book ratio is within the value range at 1.6, but this is slightly higher than the industry average of 1.2.

Leave a Reply