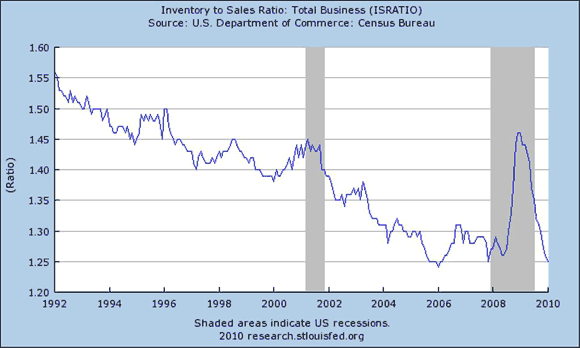

Increasingly, the recovery looks sustainable – sustainable in the sense that a double dip recession looks unlikely. As Bloomberg reports, this is the message of the inventory cycle, which appears to have largely run its course. Inventories surged as the recession intensified, leaving firms scrambling to bring output in line with the new level of sales. Now, firms have inventories under control:

At this juncture, production becomes increasingly dependent on the ability of the economy to sustain demand growth, and one critical sector, households, look capable of doing at least part of the job. Wednesday morning we get retail sales for March, with expectations for a solid 0.5% gain excluding autos – a continuation of a string of generally positive reports that reaches back to the middle of last year. That’s not to say sales have recovered; consumers are far from recapturing the prerecession trend. Instead, it looks like spending has reset along a lower growth path. And it is the growth, not the level, that is important to sustaining aggregate demand going forward.

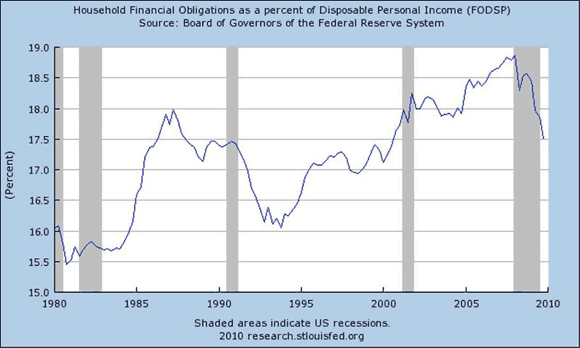

The retort for any even remotely optimistic assessment of consumer spending is that the weight of the consumer debt burden – not to mention tighter lending conditions – will curtail spending power. True enough, but that speaks more to the ability, or lack thereof, of regaining the past trend. Moreover, household balance sheets are actually improving, with household financial obligations reverting to 2000 levels:

Finally, the growing stability of the job market (even if still subpar) will further support consumer spending, not just by adding jobs, but also by releasing the pent-up demand via improved confidence.

To derail the recovery at this juncture, look for factors that are not merely weights on the outlook, but will actually reverse the positive momentum. For example, it is not enough to say that lending is constrained. To reverse momentum, one needs a story by which lending actually tightens further from the current situation (really, how many more ways can your local banker say “No”?). What are such stories? Some floating in the background:

1.) Renewed surge of foreclosures. Mounting anecdotal evidence points to a renewed surged by lenders to get failing mortgages off their balances sheets, and the ensuing fire sales will stop the housing recovery in it tracks. Moreover, falling prices will further cripple household wealth. This story, however, is most important if you were actually forecasting a housing recovery. But the lack of the typical post-recession building surge is already one of the factors keeping a lid on the pace of the recovery and preventing the rapid rebound in growth necessary to bring unemployment down quickly. Will additional foreclosures cause new residential construction to fall dramatically from already rock bottom levels? Or, as I lean toward, delay and weaken new construction activity? And note that while additional foreclosures will weigh on housing prices further, much of the big adjustment in prices is likely already behind us. Also note that foreclosures will accelerate the healing of household balance sheets; dumping an underwater mortgage improves net wealth (one of my central complains about modification programs is that they are efforts to trap households in negative net wealth positions).

2.) Waning fiscal stimulus. No doubt about it, a significant concern, but one that is already built into most forecasts for the second half of this year and next year, again preventing the sustained above trend growth of a true v-shaped recovery. More of a risk – that deficit discipline prompts fiscal authorities toward a greater retrenchment than currently expected (perhaps, for example, the Administration does little to offset the expiration of the Bush tax cuts) . Still, it is tough to see the need for rapid retrenchment when interest rates remain below the 4% mark. Or the 5% mark, for that matter.

3.) Energy price shock. Jim Hamilton ably handles this issue, noting that the current rise in oil prices does not look sufficient to derail the recovery. I would agree, but note that we saw oil prices quickly spike in 2007 and 2008, and ongoing and accelerating global growth could prompt a return of the $4 dollar gasoline that undermined the consumer in early 2008. Note that saving rates remain relatively low; while I increasingly believe the consumer rebound is sustainable, the lack of cash cushion still leaves households vulnerable to unexpected shocks.

4.) The external bogeyman. A Chinese collapse that ripples through the global economy hangs as a seemingly ever present threat, one that I have difficulty gauging. In my opinion, this is one of those issues that pessimists can cite for years (and have already) before it manifests itself into a real concern. Not unlike some of the other threats we have been living with for over a decade – like the Japanese “bond bubble.”

In short: I don’t consider myself particularly optimistic; the forecast of persistent high unemployment rates leaves me feeling pessimistic. But even a subpar outcome (one that argues for more policy action, not less) could be consistent with sustainable growth. To undermine sustainability, it is not enough to focus on factors already weighing on the economy- weak lending, fiscal stimulus waning, crippled housing sector, etc. We already know those factors are preventing a rapid return to past trends. Instead, look for factors that are not already baked into the forecast. Most likely, wait for ongoing growth to create an environment that makes the current dynamic untenable for policymakers – in other words, wait for central bankers to start tightening policy aggressively. We just are not there yet.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply