Each month the BEA releases figures for personal income and disposable personal income. These figures are a mix of private sector income and money received by individuals from the government. These government payments take the form of wages paid to government employees, and social benefits such as Medicare and Medicaid.

So I decided to take a shot at calculating ‘private’ personal income. From personal income I removed government social benefits (about $2.1 trillion in 2009) and wages paid to government employees (about $1.2 trillion). Then I added back in contributions for government social insurance, such as Social Security and Medicare payroll taxes (just under $1 trillion). Finally, I adjusted for inflation and population size to get a figure for real ‘private’ personal income per capita.

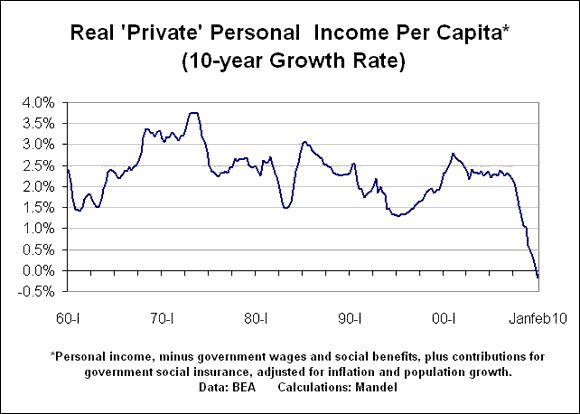

Here’s a chart of the 10-year growth rate of real private personal income per capita (the first quarter figure for 2010 is based on the average of January and February).

Over the past decade, real private personal income per capita has fallen at a 0.2% annual pace, the first time that has happened since the Great Depression.

Let’s compare this with the usual figure quoted by economists, real disposable income per capita. Real disposable income per capita–which includes government wages and social benefits, and adjusts for tax changes–rose at a 1.2% rate over the past ten years. In other words, when we add in government spending increases and tax cuts, real incomes per capita rose rather than fell.

The logical conclusion is that the private sector has been crapped out for the past ten years. Even before the crisis hit, the main thing that kept the economy afloat was the succession of Bush tax cuts and the expansion of federal spending which boosted benefits, particularly in healthcare.

This was a bad bad decade.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply