1) Tim Geithner should consider changing his name to “Stradivarius”, because the Chinese have played him like a fiddle. A week of Chinese no-shows at Treasury auctions, and Tim is left scrambling to placate Beijing. His decision to delay the release of the “currency manipulation” report in favour of bilateral discussions left Macro Man literally laughing out loud. If a one week buyer’s strike is all it takes to save face and buy the Chinese a few more weeks/months of piss-taking, well, let’s just say that Timmy Strad is in over his head.

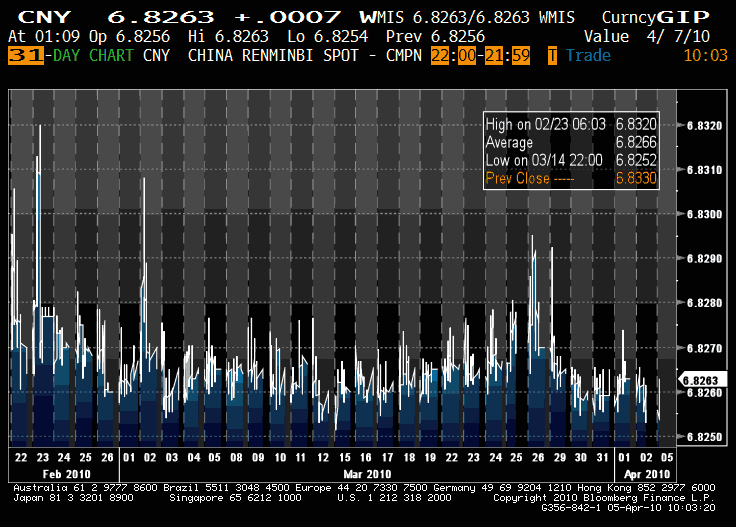

The US Treasury would do well to demand that the Chinese not intervene except when their notional daily fluctuation limits of 0.5% per day are met. Macro Man would like to show those limits on the chart below, but alas, the total range of USD/RMB since late February has only been 0.1%.

(click to enlarge)

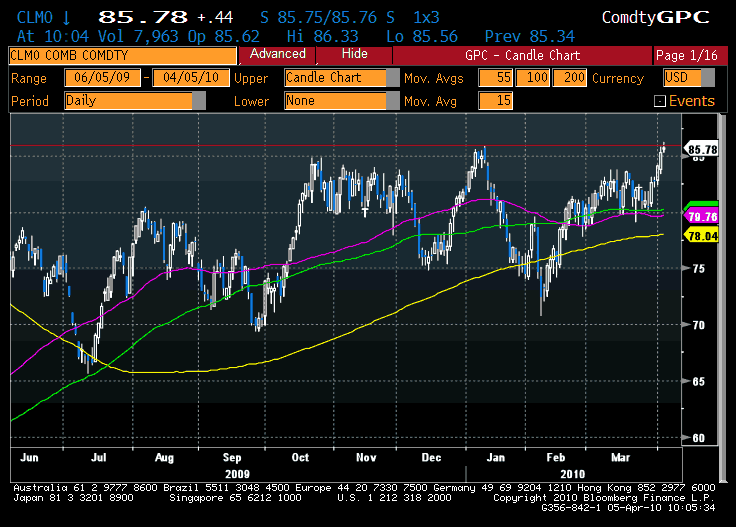

2) While it’s easy to finger the Chinese as the primary cause of Treasury weakness, that would be a gross oversimplification. The end of Fed QE has no doubt had an impact on quasi-Treasury MBS, and even more prosaic, old-timey, “fundamental” factors may be playing a role. Oil appears to have employed stealth technology in its latest bull run, given the general lack of acclaim that it’s received. But as you can see from the chart below, June oil is now at its highest level since Lehman; small wonder bonds have been wobbly!

(click to enlarge)

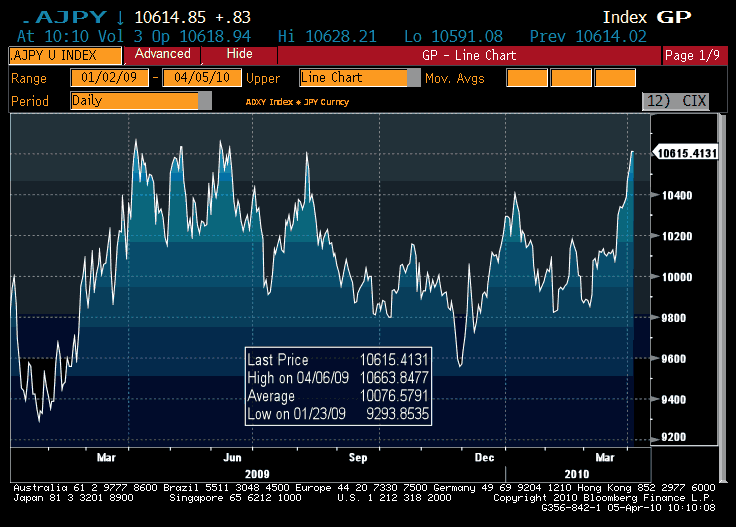

3) Mumblings of a Chinese reval combined with higher US rates; if you thought that sounded like a perfect storm for Asian currency outperformance versus the yen, you’d be right. The “AJPY” (ADXY * USDJPY) is up 7% since the beginning of March; perhaps it’s small wonder that the Nikkei is among the star performers amongst equity indices this year.

(click to enlarge)

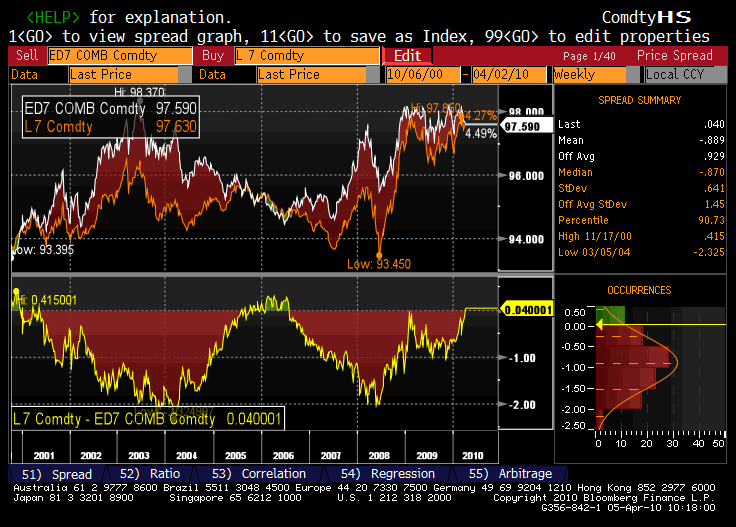

4. Following on from Thursday’s sterling post and Friday’s solid payroll figs, Dec 2011 eurodollars are now pricing in higher rates than Dec ’11 short sterling. Obviously, some of that is down to the fact that LIFFE has been closed the last couple of days; no doubt sterling will re-assert a small premium tomorrow. But still….it does seem odd that sterling is rallying in this context, which provides further evidence that it is primarily a short-covering rally. By the same taken, equal rates in Dec of next year isn’t exactly what you’d expect when you have one central bank talking about record low core inflation, and the other writing letters apologizing for the high levels of CPI. Hmmmm….

(click to enlarge)

5) Being a sports fan leads to some strange juxtapositions. Tonight sees Macro Man’s alma mater cast in the Darth Vader role of perhaps the biggest “good versus evil” morality play since the roles were reversed 19 years ago, back in the days when your author was in attendance.

At the same time, today sees opening day in baseball, where Macro Man is a fan of what has arguably become the worst team of time; certainly they’ve set the benchmark for consecutive losing seasons by an American professional sports team.

Just goes to show that in sports, as in trading, you can’t win ’em all…..

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply