We had negative quarters in the S&P on 2008 which made the PE ratio skyrocket to ridiculous levels. The trailing-twelve-month (TTM) earnings had to deal with negative quarters, until now: the last negative quarter was 4Q08, and it is about to drop out of the TTM calculation. Since almost all S&P companies have reported (99%), we can pretty well estimate the new TTM PE ratio for the S&P: 22. This is still high historically.

The market is looking at estimated forward twelve month (FTM) numbers, which have the S&P at around a 14 FTM PE. Yardeni expects earnings to grow from around $75 to close to $100 per share across the S&P in 2011, which would push the market towards Sp1350 at year end 2010. Still, dividends are lower than normal, down almost 10% YoY. S&P companies are sitting on cash, which in normal times would depress future growth, and earnings. Instead, if we get a recovery, they may increase dividends, sprucing returns to investors.

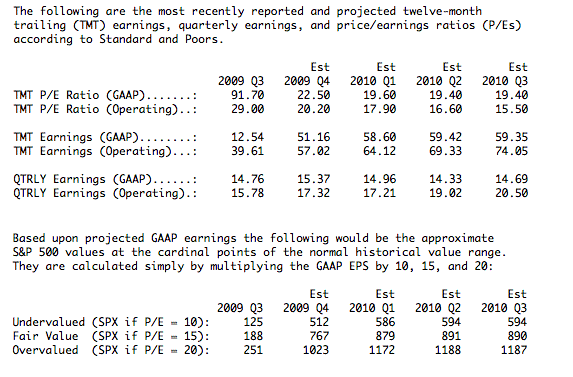

The Pragmatic Capitalist gives us a handy chart to estimate the S&P at more normal PE ratios:

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply