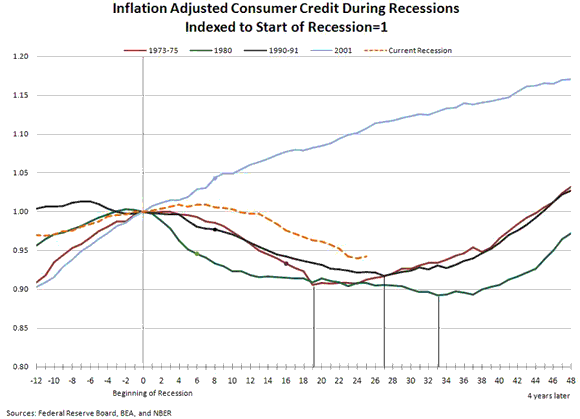

Total consumer credit outstanding expanded by $5 billion in January after contracting 15 of the previous 17 months. Consumer credit outstanding includes revolving and nonrevolving credit. Revolving credit is mostly credit card debt, and nonrevolving credit includes loans for items such as vacations, autos, and boats. Even with the slight increase in January, total consumer credit (after adjusting for inflation) has contracted nearly 6 percent since the recession began in December 2007. This number might seem like a huge contraction but compared with three of the past four recessions, it actually looks rather typical. Consumer credit contracted 9 percent in the 1973–75 recession, 11 percent in the 1980 and 1981–82 recessions (treated as one recession here), and 8 percent in the 1990–91 recession.

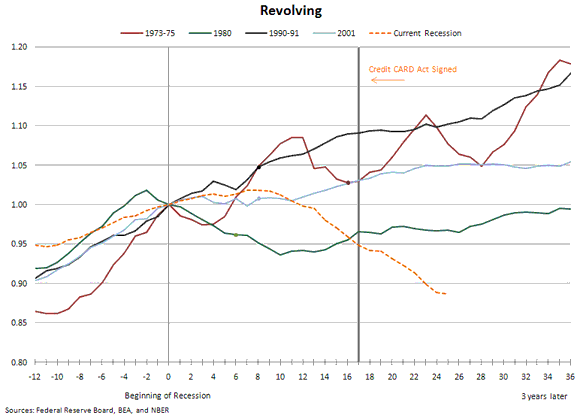

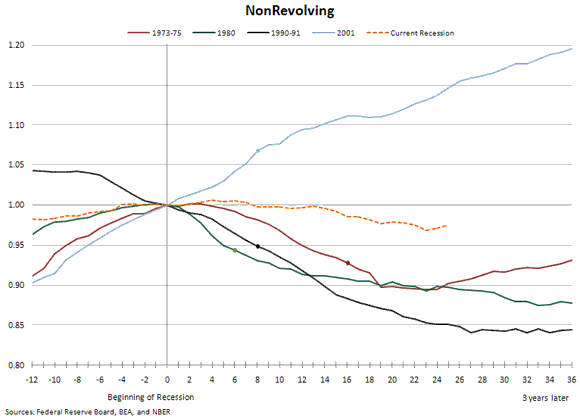

However, once the current recession is separated into revolving and nonrevolving credit, the relationship to past recessions changes. Typically in a recession, nonrevolving credit shrinks considerably while revolving credit shrinks little if at all. The trend so far in this recession has been the exact opposite; nonrevolving credit essentially has remained unchanged while revolving credit has shrunk 11 percent.

Is the decline in consumer credit the result of supply- or demand-side forces? Perhaps the answer is both.

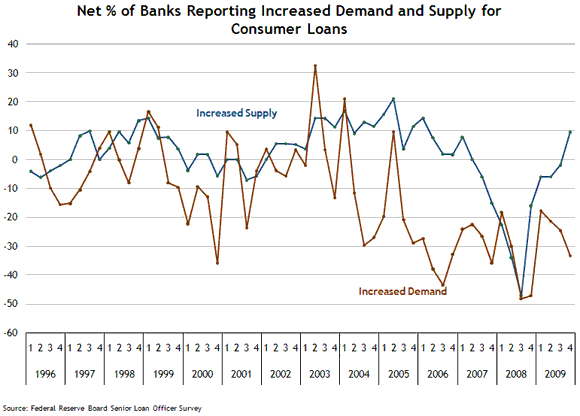

According to the Federal Reserve’s Senior Loan Officer Survey, demand for all types of consumer loans (revolving and nonrevolving combined) has fallen since the first quarter of 2009. A decrease in demand for consumer loans is plausible because consumers tend to delay big purchases such as cars and vacations when uncertainty about future income increases. Because future income is affected by job prospects, consumer credit demand lags the recession much like employment does.

The chart below shows banks reporting an increase in willingness to make consumer loans. In fact, the fourth quarter of 2009 marked the first time in nearly three years that more banks reported increased willingness to supply consumer installment loans than have reported decreased willingness.

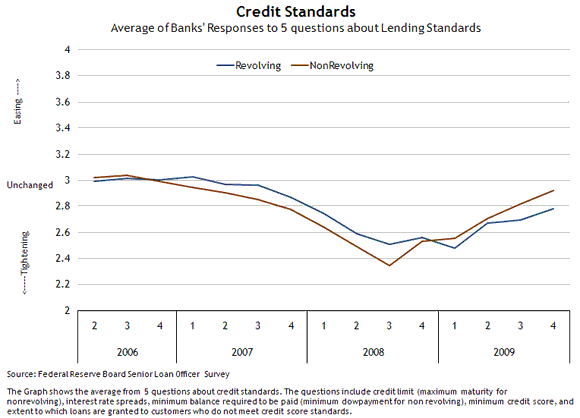

Even if banks are more willing to make consumer loans, their lending standards have gotten tougher. Increased credit standards have moderated in recent months, but on average banks are still reporting tightening rather than easing based on the January Senior Loan Officer Survey. This tightening is particularly evident for consumers seeking revolving credit. In fact in the fourth quarter of 2009 banks on average reported increased tightening for credit limits of revolving credit compared with the previous three months. This development came as little surprise since a special question on the Senior Loan Officer Survey in October revealed that banks would tighten a wide range of their credit card policies following the enactment of the Credit CARD Act.

Looking ahead, it will be interesting to see to what extent the tightening of standards for revolving credit impacts overall lending and to see if the Credit CARD Act ends up impacting revolving credit availability in the long run.

By Ellyn Terry, senior economic research analyst at the Atlanta Fed

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply