Congratulations to Didier Defago, new Olympic downhill champion, for conquering the Dave Murray course yesterday in Whistler. The run is the second longest in Alpine skiing (behind Wengen in, perhaps uncoincidentally, Defago’s home country of Switzerland), and as such requires a substantial degree of stamina. It was this endurance angle that made yesterday’s competition so compelling, as the fastest skier on the top half of the course (Bode Miller) plainly ran out of gas further down the mountain; it proved to be impossible to determine who the ultimate winner would be on the basis of the splits throughout the race.

It seems as if risk-asset bears will require a bit of stamina as well, as the downhill trajectory of global markets is proving to be as treacherous and bumpy as the Dave Murray. Stellar headline results from Barclays have given stocks an early-session fillip, and no doubt punters are wondering if “Magic Monday” will transmogrify into “Terrific Tuesday” courtesy of yesterday’s US holiday.

Yet beneath the surface, tensions still bubble along. The Greek situation remains unresolved, and Ecofin president Juncker rubbished the notion this morning that the IMF could be of any assistance whatsoever. OK, fine, but what are the alternative solutions? A European bailout seems like a pretty unpalatable solution for obvious reasons; in addition to the questionable legality of such an outcome, it’s not exactly a vote-winner in the core of EMU to subsidize a country where the national sport is tax avoidance.

So what are the options for Greece? The country is threatened by both liquidity issues (its ability to roll over debt) and solvency concerns (its ability to pay off principal and fund its ongoing outlays.) Fiscal reform is unlikely to bear immediate fruits of such richness that these problems will vanish. So what can they do?

It’s impossible to formally deval within the Eurozone, though they can effect a de facto “financial devaluation” on both the liability side (via bondholders’ haircuts) and the asset side (via a substantial wealth tax.) Neither of these will prove sufficient to permanently solve Greece’s problems, however, especially given that they do nothing for Greece’s competitiveness on the trade front.

The most likely option at this juncture appears to be what might be called the “Thriller” approach, i.e. muddling through, fighting fires on a case-by-case basis, and slowly turning into a zombie.

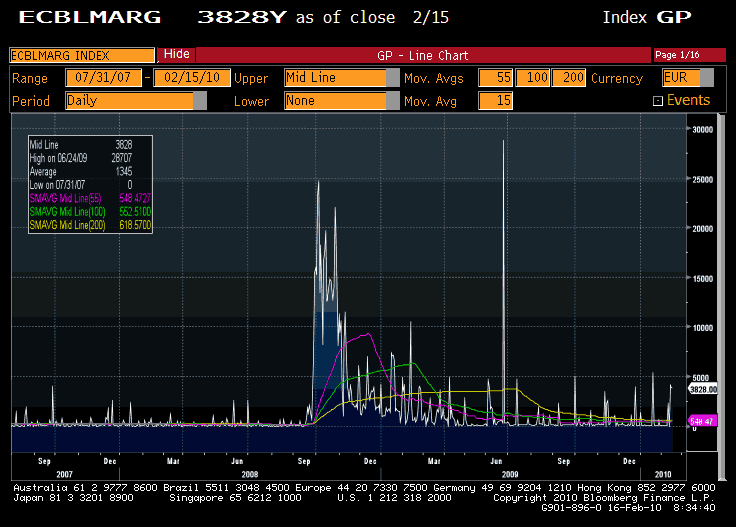

In any event, just because the course of markets has flattened out a bit for the time being doesn’t mean that there aren’t dangerous dips in store for the intrepid skier of financial markets. Over the past couple of days the ECB has seen decent demand (~€4 bio/day) for funds at its marginal rate of 1.75%; one wonders what sort of institution that has eligible collateral to borrow with this facility couldn’t find cheaper funds elsewhere (such as, er, EONIA.)

(click to enlarge)

In the context of yesterday’s comment on the fictional nature of benchmark short rates, this demand for funds is interesting, to say the least.

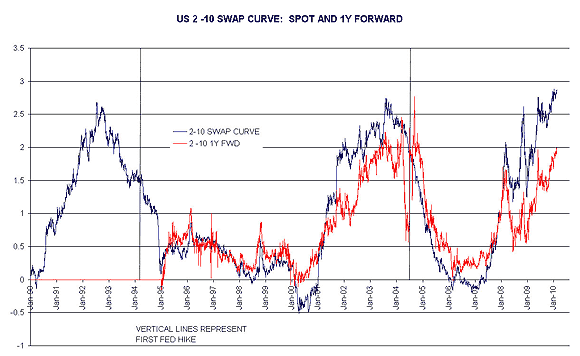

Elsewhere, curves continue to steepen to relatively extreme levels; the US 2-10 swap curve is now basically at its steepest level of the past two decades (and that’s with 10y swap spreads at an egregiously low level!) Sadly for the punter wishing to take the other side, the negative of the flattener is close to prohibitive; the 2-10 curve one year forward is nearly 90 bps below spot.

Still, at some point the flattener will start to appeal. In the last two US monetary policy cycles (really, the only two of the “swaps era”), the curve started flattening well before the Fed started putting rates up: more than a year, on average. Given the negative carry, now might not be the time to think about this trade, but should the carry become less onerous it will start to look mighty attractive. Moreover, the front end of the swap curve could come under pressure if the outlook for the financial system (inspired by a Greek haircut/default, perhaps?) starts going downhill….

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply