The good news is that the snow has finally started to melt. The bad news is that the precipitation hasn’t stopped; we’ve just reverted to the usual miserable rain. Still, it’s said that misery loves company, and while there is tragically an all-too-real wellspring of misery in Haiti in the purely financial sphere there is plenty of unhappiness to go around as well.

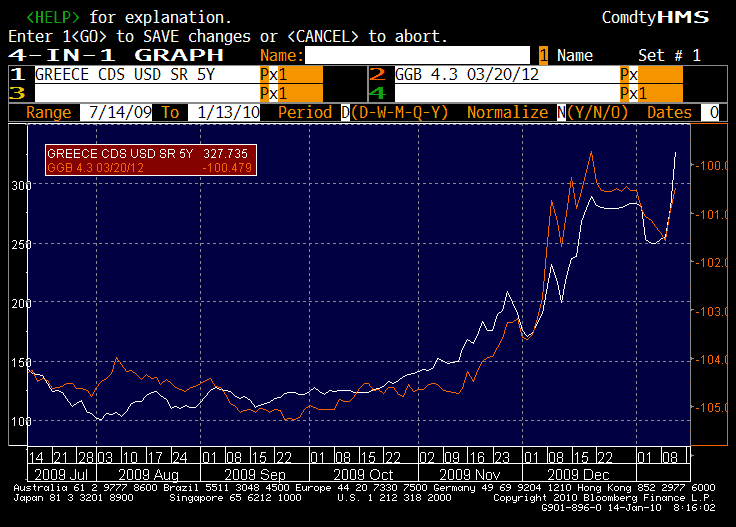

Greece, after enjoying a respite over the Christmas holidays (both Western and Orthodox) has come under the cosh once again, with yesterday’s rather unflattering ECB view of Greek debt restructuring proposals putting sovereign debt under pressure once again. While there was no doubt selling of actual bonds pushing the March ’12 yields over 4%, it would appear that most of the pressure was speculative in nature; observe how 5y CDS (white line, left hand scale on the chart below) attained fresh highs even as the price of the 2012 bonds didn’t plumb fresh lows.

(click to enlarge)

With Trichet speaking today after the ECB announces rates, markets will be keen to watch for signs that Greece is being cut adrift or in for further censure. (It should make entertaining viewing if for no other reason than that the Vice President of the ECB is himself Greek.) The market will also watch for signs of policy normalization, though it’s probably premature for such signals; that didn’t stop last month’s press conference from being an expensive proposition for Macro Man, alas.

Speaking of normalization, there were conflicting reports out of the US yesterday. Macro Man’s favorite purveyor of fairy tales was at it again yesterday, as a “paid advisory service” reported that the Fed may look to eventually allow the funds rate to drift up towards 0.50%, and they plan to start talking about it as soon as June. Wonderful! So now conversations planned five months in advance are now news? Mark it in your diaries, ladies and gentlemen: Macro Man has strong plans to talk about football (not the American version) on June 12th….

In any event, comments from NY Fed president Bill Dudley, who presumably knows a bit more about the trajectory of rates than the paid advisory service, said that rates could stay low as long as two years. Possibly coincidentally (but probably not), Mr. Dudley’s successor as Goldman’s chief US economist is among the few forecasting unchanged rates through the end of 2011.

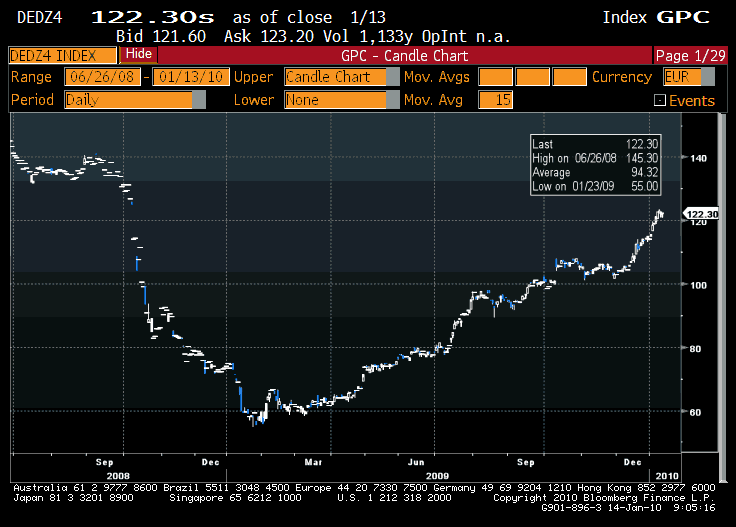

Finally, Macro Man shed a tear yesterday (OK, not really) as he bade adieu to the longest surviving resident of his portfolio yesterday. He closed out all of his positions in Eurostoxx dividends, which he first bought in February of last year as a hedge against his short-risk portfolio. The 2014 vintage, shown below, more than doubled in value.

(click to enlarge)

While there remains some upside to these contracts, it is considerably less enticing than it was just a few weeks ago. Assuming dividend payouts of 150 Eurostoxx 50 index points in 2014 (more or less consensus) , the annualized gain to be had from current levels is just over 4%. (Broadly similar to the yield available on 2y Greek paper, funnily enough!) While they can certainly richen further, these suckers do tend to build in a term premium a la eurodollar futures, so Macro Man wonders how much upside is really left. Moreover, the ongoing travails of Greece, as well as unpleasant surprises like yesterday’s SocGen writedown, provide a timely warning that serpents still roam the apparent Eden of current market sentiment.

It’s been a good run, and these divvy positions singlehandedly kept Macro Man’s equity book (modestly) in the black last year. With a lot of the juice now squeezed from the fruit, it’s best to lock in the rewards so as not to live through a Greek tragedy or any other misery that might otherwise come his way.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply