In his recent speech, Federal Reserve Bank of Atlanta President Dennis Lockhart highlighted concerns about the linkage between commercial real estate loan problems at banks and small business financing during the economic recovery:

“The overall commercial real estate debt in the financial system is smaller than residential, but it is disproportionately concentrated in small and regional banks. Smaller banks are a significant source of credit for small businesses, and in most recoveries we look to small businesses to generate a significant number of jobs.”

President Lockhart also referenced the results of a survey of small business finances the Atlanta Fed conducted late last year.

“A recent small business survey performed by the Atlanta Fed suggested that business loan demand was down primarily because of weak sales and modest revenue prospects. The credit availability picture was mixed. No surprise, construction-related firms and manufacturers had the most trouble obtaining credit during the last six months. But others did well in having their credit needs met. Of more than 200 respondents, nearly half did not look for credit at all, mostly citing weak sales or sufficient cash reserves.”

The survey President Lockhart was referencing was conducted in early December and included responses from 206 small businesses across the Sixth Federal Reserve District (the states of Alabama, Florida, Georgia, Louisiana, Mississippi, and Tennessee) regarding their access to credit. The intent of the survey was to include some additional small business perspectives to supplement our other monetary policy information-gathering efforts.

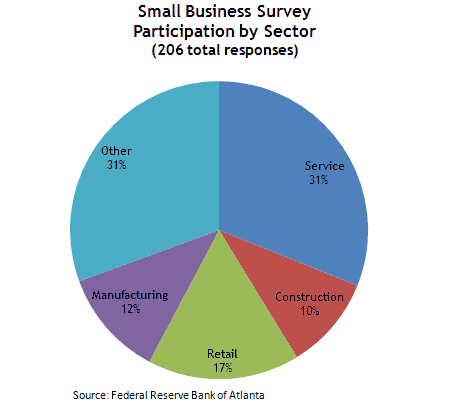

The firms in the survey were contacts established through our Regional Economic Information Network. In that sense, the survey is not based on a pure random sample of firms. However, the industry distribution of respondent businesses was reasonably representative of the industry mix of the Sixth District (see the chart). The average firm size in the survey was about 22 employees, with around 40 percent of respondents having between one and nine employees.

So, how did businesses surveyed respond? Slightly more than half the respondents said that they had sought to obtain a loan or line of credit from a bank in the last six months. The primary reasons given by those seeking credit were to replace an existing loan (cited by 50 percent of those respondents) and/or to obtain additional working capital (cited by 45 percent of those respondents).

The degree of difficulty firms felt they had in obtaining credit was mixed, with about 60 percent of respondents saying they were able to obtain all or most of the bank credit they sought. The small size of the survey (206 respondents) limits the accuracy of any sector-by-sector comparisons. However, it is interesting to note that construction firms stood out as the business type that had the greatest difficulty having their demand for financing satisfied, with 70 percent of them saying they were unable to obtain the funding they sought. That percentage compares with 50 percent of small manufacturers surveyed and 25 percent of retailers responding they were unable to obtain the funding they desired.

Of those businesses that had not sought credit during the last six months, the dominant reason given was poor sales/revenue (cited by 55 percent of those respondents). Other reasons for not seeking additional credit included sufficient cash reserves.

Slightly less than half of respondents expected to try to obtain a loan or line of credit from a bank during the next six months. The reasons given for seeking credit (businesses could give more than one reason) included the need to replace an existing loan (cited by 43 percent of those respondents), the need for additional working capital (cited by 44 percent of those respondents), and the need to purchase equipment (cited by 21 percent of respondents). Among firm types, construction firms anticipated a higher demand for credit than others.

For respondents who were not expecting to seek credit over the next six months, the anticipation of poor sales growth was the most frequently cited reason (cited by 49 percent of those respondents).

There are plenty of caveats that should be applied to these results. For example, the survey respondents represent established, relatively successful firms. We could not, with this effort, capture the experience of firms that have recently failed (perhaps for lack of credit). Nor can we ascertain the businesses that were never formed because they could not obtain start-up funding.

Still, we believe the results of our survey are instructive. To the extent that the firms in our survey are representative, it appears most going concerns have been able to obtain all or most of the credit they need. What they don’t have are customers.

Of course, this is a snapshot of current conditions, and things may change as the economy picks up, demand expands, and credit needs grow. And it would be very useful to know what the story is with those firms that have failed or were never created. We are consequently planning to conduct a follow-up survey as 2010 progresses. We’ll keep you posted.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply