Is it really different this time? In other words, is this recession really different from past recessions? I argue only in terms of magnitude. It was a bad recession, but it ultimately wasn’t any fundamentally different. Will the recovery be muted? I actually don’t think so. I just think we went down so hard that it will take a long time to recover. Unemployment, for example, will be relatively high through 2010, but mainly because it got so high in the first place. I expect fairly consistent improvement in all economic indicators through the year.

If you disagree with the above, fair enough. Clearly the Fed should remain accomodative if the economy isn’t growing. But what if we are recovering? Even if its a slow recovery? What should the Fed do? If this time really is no different, then they should do what they always do after a recession. Tighten policy.

Milton Friedman argued, quite convincingly I think, that the perfect monetary policy was to have relatively small and stable growth in money supply year after year. He actually argued that this could be done robotically, and that actual human judgement was a detractor to the process rather than additive. While I’m very sympathetic to this view, its clear that given today’s banking system, we can’t measure the de facto money supply accurately enough to implement the computerized Federal Reserve that Friedman envisioned.

John Taylor then argued an alternative in the 1980’s. If we can’t measure money directly, let’s measure its impact and try to target that. He said we could measure the output gap (difference between real GDP and potential GDP) and the difference between actual inflation and ideal inflation, then set monetary policy to push these numbers back toward the goal. This is the genesis of the Taylor Rule.

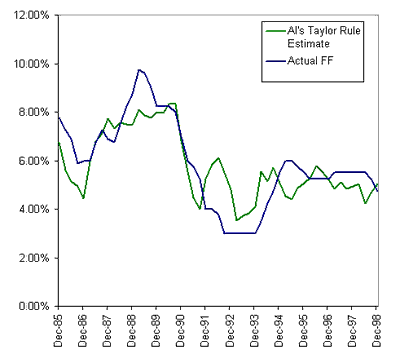

Now let’s back up for a moment. Look at the history of the Taylor Rule vs. actual policy during the so-called Great Moderation.

Taylor has argued that if we look at most of this period, actual policy seems to follow the Taylor Rule quite nicely. He argues that the Great Moderation occurred because of this enlightened policy.

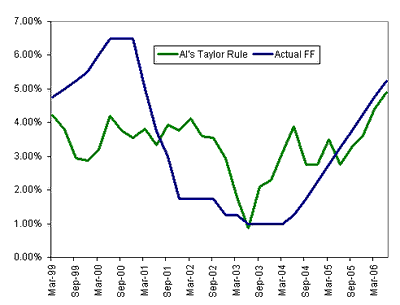

Then we get the 1999-2006 period.

Policy was consistently off, mostly being too low from 2001-2004. What did we get? A pretty poor decade of economic performance.

Where are we now based on the Taylor Rule? Right this minute my estimate is that its calling for Fed Funds to be -2%! Hence why I thought QE made sense. We can’t get traditional monetary policy easy enough. But if GDP growth is just 2% in 1Q and 2Q and CPI hangs around 1.5, the Taylor Rule suggested Fed Funds rates jumps to 0.75%. If inflation accelerates to just 2%, the recommendation is 2% by the end of the second quarter.

Realistically, the Fed can’t (or won’t) hike 200bps in just a few months. They are more likely to move in 25bps or 50bps clips lest they spook the market too much. Given that they meet every six weeks, it would take them 10 months to get from 0.25% to 2% at 25bps per-meeting hikes. If we throw a couple 50bps moves in there, it still takes them 7-8 months. This is why they need to start removing extraordinary accommodation now.

Remember, that monetary policy isn’t really about interest rates. Fed funds is just the tool the Fed uses to alter the money growth rate. As such, we could say that the Fed’s extraordinary liquidity measures are creating a de facto funds rate well below zero. The flip side of this is that with the economy improving, the effective funds rate is even further from its proper spot. So even if the Taylor Rule suggested rate is zero, the Fed would need to slow the money growth from its current pace considerably.

Ben Bernanke is currently talking about the lessons of 1938. I say learn the lessons of the Great Moderation and stick with a stable monetary policy.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply