5. China will NOT meaningfully adjust its exchange rate mechanism in H1.

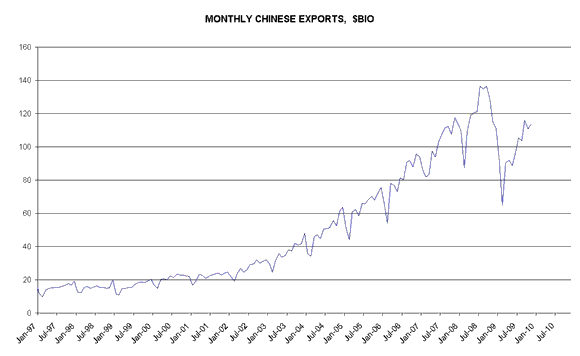

By this, Macro Man means that there will be no step reval, and that the peg at or around 6.8250 will remain intact. He was tempted to indulge in a spot of reverse psychology and forecast no move at all this year (there’s a decent chance of that), but he’s settled for just non-predicting the first half. What will spur a Chinese exchange rate move? Macro Man is looking at domestic inflation conditions, but also at two external factors. The argument could be made that the authorities will do nothing on the RMB until exports exceed their 2008 peak (they’re currently more than $20 billion below, on a monthly basis). Given the exorbitant Chinese whingeing about the US policy mix, Macro Man can also construct a scenario wherein PBOC doesn’t let the RMB move until the US starts tightening policy.

Of course, common sense would dictate that the appropriate response to “why should we tighten until you do?” is “grow a pair! Your nominal GDP growth is 12% higher than ours!” Sadly, however, common sense has little role to play in discussing the likely policy response of the world’s great mercantilist power.

So there you have it: the first half of this year’s non-predictions. Tune in tomorrow for the second five.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply