Professor Krugman has repeatedly emphasized that little of what we understand from past business cycles applies today, because interest rates are near zero today (so he says). He concludes that the only useful studies are those of other eras of near-zero interest rates, and as a result one can ignore what Professor Barro, Mankiw and I (and anyone else who uses “traditional” economics) say about government policy.

First of all, one should have actual evidence that a low-interest rate economy responds differently to fiscal and regulatory policy. He has none, while we have plenty of evidence that fiscal and regulatory policy are having very much the same effects as they always do.

Even if we accept on faith that only low-interest rate economies must be studied, then one has to pay more attention to Barro and Mulligan, rather than less.

I’ve done some work on public policy and low interest rates, as in my JPE paper “Extensive Margins and the Demand for Money at Low Interest Rates.” My approach there was not to assume that the economy would be special at low interest rates, but rather look for evidence that would confirm that idea.

For years, Professor Barro’s Macro textbook has used World War II to estimate a government spending multiplier. (He and Charles Redlick have recently revisited WWII, and other U.S. defense spending episodes). I have looked at the labor market during World War II. Both of us looked at the expansion of government circa 1941-42 and the contraction of government 1946-47.

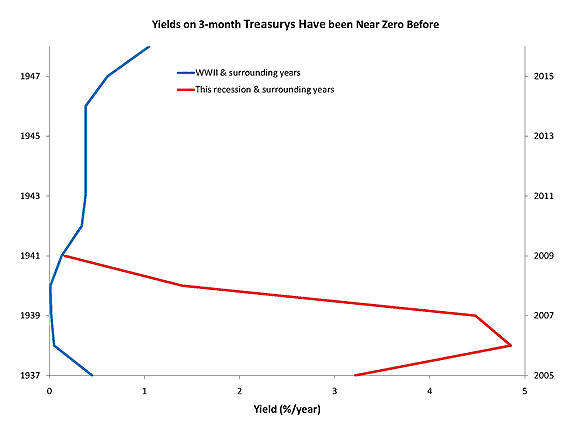

If low-interest rate economies must be studied for the purposes of today’s policy-making, studies like ours should get a lot of weight. The chart below shows the yield on 3-month Treasury Bills by year 1937-47 and 2005-15. Year is measured vertically and nominal yields are measured horizontally. Thus, near zero yields are seen on the left border of the chart.

As you can see, yields were at least as low during the episodes studied by Barro and I as they are today. For example, the average yield in 2009 was about the same (just a bit higher; shown by the red curve) as the average yield in 1941 (shown by the blue curve).

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply