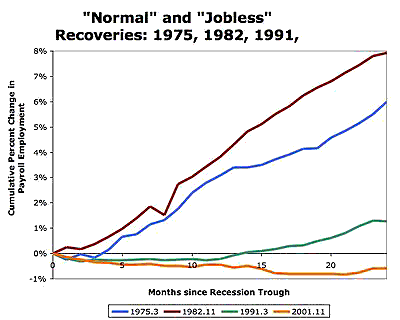

The behavior of U.S. employment at the end of the last two recessions (1991 and 2001) was different than in previous recessions. Employment did not grow fast and it took several years to reach the pre-recession levels. Because of this, the recovery years that followed both of these two recessions have been labelled “jobless recoveries”. Below is a chart from Brad de Long that compares them to two other previous recessions (original posting is here).

Employment was flat in 1991 and 2001 instead of increasing fast as in 1975 and 1982. Because of the current high level of unemployment combined with what might be weak growth there is a fear that the current recovery will also be a jobless one and that the unemployment rate will take a long time to reach a normal level (here is Krugman on this issue).

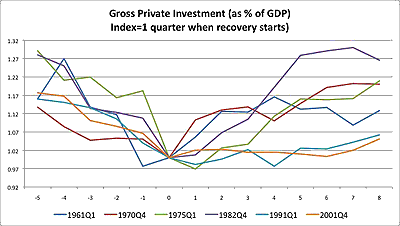

The behavior of employment will depend on many factors (amount of labor hoarding, productivity) but at the end of the day, the major factor be remain the strength of the recovery and how fast GDP and demand can grow. If we look at different components of demand (or GDP) there is an interesting factor about the last two recessions: In both of them, investment played a weaker role during the recovery phase. Below is a chart comparing the behavior of investment (measured as a % of GDP) around the recovery time (0 is the quarter when the recovery started according to the NBER).

What is interesting in this chart is that the last two recoveries were also special when it comes to the behavior of investment. In fact, the behavior of investment seems to mimic what we see above in the employment chart. While during the 1975 and 1982 recoveries investment grew faster than GDP (so the ratio increased), during the 1991 and 2001 recessions, investment grew at the same pace as GDP (so the ratio is flat). And this is more of a surprise if we take into account the fact that real interest rates remained very low during these two recoveries (more so in 2001).

We know that investment is the most volatile component of GDP so the V-shape that we see in 1975 and 1982 is what we would normally expect. By definition, it has to be that other components of GDP played a stronger role (relative to previous recessions) in 1991 and 2001 (consumption, exports). What was the exact role of those components will (hopefully) be the subject of a future post in this blog. What is interesting so far is the similarity in the behavior of employment and investment across the most recent recessions.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply