Yesterday afternoon right after the close, the Housing Index was released and came in at 18… a drop from the miserly reading of 19! Every category measured was down, here’s Econoday:

Highlights

The pending expiration of the $8,000 first-time buyer credit made for a disappointing 1 point dip in the October housing market index to 18, according to the National Association of Home Builders (NAHB). All components dipped in the latest report especially traffic which fell 3 points to 14. The results hint at a step back for housing which had been on the rebound thanks to government stimulus. The NAHB along with the National Association of Realtors are urging the administration to extend the first-time buyer program another year. Stocks are edging lower following the results but are still solidly higher on the session. Housing starts for September will be released tomorrow morning.

Weak, weak. Think banks will be in any kind of condition with that type of housing “rebound?” According to one forecasting firm, home prices are expected to fall another 11% nationwide in the next year ( Homes: About to get much cheaper). That will further destroy the bank’s balance sheets (real banks, not GS and JPM, the pretend bank/casinos).

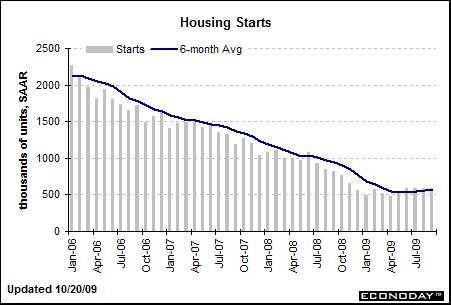

Indeed, housing starts came out this morning and missed expectations. Here’s Econoday’s take, absolutely depression level readings with downward revisions:

Highlights

Housing starts look positive in September from August but not after taking into account a downward revision to the prior month. Housing starts in September rose 0.5 percent, following a revised 1.0 percent decline in August. The September pace of 0.590 million units annualized was down 28.2 percent year-on-year and fell short of the consensus forecast for 0.615 million units. Importantly, August was revised down from 0.598 million units to 0.587 million units annualized. The advance in September was led by the single-family component which increased 3.9 percent after dropping 4.7 percent the month before. In contrast, the single-family component fell 15.2 percent after rising 20.7 percent in August.

By region, the September decline in starts was led by an 8.8 percent fall in the West with decreases also seen in the Northeast, down 5.5 percent, and the Midwest, down 1.8 percent. Starts in the South rebounded 7.1 percent.

Housing permits point toward a pause or temporary leveling in the housing recovery, slipping 1.2 percent, following a 2.8 percent rise in August. Permits in the latest month stood at an annualized 0.573 million units and were down 28.9 percent on a year-ago basis.

Markets appear to have gotten a little too optimistic about the upward trend in starts continuing without any bumps in the road. Homebuilders appear to recognize that supply of homes on the market is still high and that a strong recovery in new construction is not yet called for. While the downward revision to August may be a little disappointing to traders, the net result through September is still a nice, moderate recovery from the recession bottom.

On the release, equity futures dipped. Treasury yields eased and with additional help from lower-than-expected headline and core PPI numbers. (emphasis added)

What a disaster. Year ago numbers were already a complete and total disaster and now starts are down ANOTHER 28.2% in the past year!? Yikes! So we got a level out and now another descent has begun. Who could have known?

And the joke of the day goes to both Goldman with their ICSC store sales report and also to Redbook who are both saying that yoy sales figures are slightly positive! To which I simply have to call bullshit! Year over year sales are way down, the proof being sales tax revenues which are down nearly 20%! I hope that when all the fallout finally hits that we can destroy and tear down this type of complete fraud. Again, I would also take down all agencies that report government statistics and start over with one agency and a new set of rules for generating statistics (must always report raw data, must always report in the same manner using the same collection methods, etc).

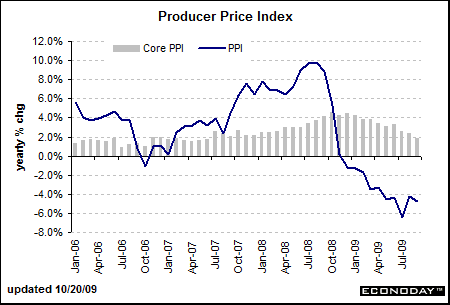

And here’s a surprise that very few have forecast except for yours truly, the PPI accelerated downwards! Once again the inflation crowd (and I do mean crowd) is just plain wrong as the PPI is down 4.7% year over year.

Highlights

Signs of inflation have disappeared in the government data-at least temporarily as the PPI report is still lagging the recent rise in oil prices. The overall PPI fell back 0.6 percent in September after rebounding 1.7 percent the month before. September’s drop was deeper than the market projection for a 0.3 percent decline in the headline PPI. The decrease in the latest month was led by a 2.4 percent fall in energy costs with food price inflation dipping 0.1 percent. The PPI core rate surprising slipped 0.1 percent, following a 0.2 percent increase in August. The decline was due in part to a drop in prices for light trucks. The consensus had forecast a 0.1 percent gain for September.

The September drop in energy prices was led by gasoline which fell 5.4 percent after a 23.0 percent surge the month before.

The core rate dipped largely on a 1.4 percent drop in light truck prices and a 0.6 percent decrease for computer prices.

For the overall PPI, the year-on-year rate dropped to minus 4.7 percent from minus 4.3 percent in August (seasonally adjusted). The core rate year-ago pace declined to up 1.8 percent from up 2.3 percent the prior month. On a not seasonally adjusted basis, the year-ago decrease for the headline PPI was 4.8 percent while the core was up 1.8 percent.

Inflation clearly has been smothered by weak demand and an earlier dip in oil prices. But in coming months we may see a rise in the headline number from recently strong oil prices. But this morning, Treasury yields were down on both the PPI and a downward revision to housing start numbers. (emphasis added)

This is a huge deal, an out-of-control deflationary spiral is a real possibility, especially if oil prices finally begin to react again to the cliff dive in demand. When we look at demand for oil and the transportation levels in general we are still seeing a drop of historic proportions. Should the fuel for speculation in these markets suddenly end, as they did last year, then you will see a deflationary spiral that will set your hair on fire!

Meanwhile, sales of the iPhone ignited better than forecast earnings at Apple. Frankly, their demand has surprised me as I would have thought that the consumer would run out of such discretionary money by now. Perhaps since they are no longer treating themselves to new houses and cars that splurging on a gee-whiz gadget is their one self-treat, for now. I’m still thinking that by the time this is over even the discretionary gadget sales will be very impacted, we’ll see.

So, we made new highs again yesterday, that means that the 3rd wave up of the final 5 got underway. I am beginning to see large cracks however, and note again that this could terminate anywhere in here. We are close… close to a top, close to the end of the count, close to the end of this rising wedge, close to wave C down, close to the end of our current dollar system, and if the government keeps on its present course, close to the end of our country as we know it. The problems we are facing are not your children’s problems, the math will not let it get that far and the problems are bigger than your government because it was your government that created the problems (bad math) to begin with!

The divergences here are as historic as the data is negative. Anyone who has read this blog has been warned…

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply