The Dollar’s weakness this week seems to be due to an organized attack on it, shades of Soros shorting the Pound in the early ’90s. The story on the secret cabal to replace the Dollar may have been a planned leak which was followed by an organized short and a surge in gold. Now the Financial Times reports of massive intervention in Asia to support the Dollar and slow the rise of Asian Tiger mercantilist currencies. The head of the Euro Central Bank has also been publicly bemoaning the weakness of the Dollar and a potential deal between the US and China to let the Dollar slide slowly while removing pressure from the US on forcing the Chinese to appreciate their currency. In other words, organized debasing of both currencies. In such a scenario, the Euro would continue to strengthen, threatening Euro exports. So now the Euro wants to join the race to devalue. Not really possible, is it? No one gets relative advantage.

These manipulations can explain why equities have been spiky in the past week. They also support the ending diagonal formation the USD, a formation which can form as intervention emerges, and can reverse sharply. Tomorrow may be a bounce in the USD and a fall in gold and US equities. How sustained this will be remains to be seen. The USD forex market is absolutely huge. It is a treacherous moment, however, when the worlds reserve currency can suffer from mere rumors of secret cabals; it shows a pervasive lack of confidence in the management of the currency.

The real secret cabal may be US leadership (Obama, Geithner, Bernanke) planning to continue to allow a slow fall of the Dollar in order to finance horrific deficits while lessening the burden of ever paying back the creditors. Two very interesting analyses of this in the last few days:

- Chris Martenson of The Crash Course argues that the Fed has postponed deflation by hiding the worthless debt for the banks. During the Greenspan Bubble from 2002-2007 the US doubled its Dollar denominated debt, from $26T to $52T. That increase is not supported by any concomitant increase in US productivity to support that level of debt, and hence can be expected to be written off to the tune of $20-25T. The write down of such magnitude would create a deep deflation. Some deflation is with us, but much of the worthless debt has been swapped into the Fed, where it sits without yet needing to be written off.

- Various commentators including here have noted how the Fed needs an exit strategy from their swaps of toxic debt: “Paradoxically, by buying and accepting bad assets, the central banks did not fix the solvency problem: they merely delayed the inevitable. The bad loans did not turn “good” by changing hands or being accepted as collateral by central banks.” As the Fed swaps them back, they send the zombie banks back into insolvency, causing the financial crisis to re-emerge. The internal debates inside the Fed to begin the exit, which would start with raising rates, is beginning to leak out.

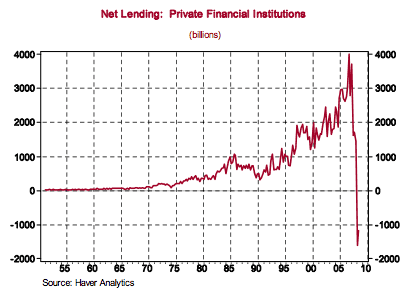

The core rule of economics is TANSTAAFL, and in this case the consequence of the Fed hiding the hot potato of toxic debt is a crushing drop in credit availability that is continuing and maybe accelerating. Simply put, zombie banks don’t lend. See chart.

The core rule of economics is TANSTAAFL, and in this case the consequence of the Fed hiding the hot potato of toxic debt is a crushing drop in credit availability that is continuing and maybe accelerating. Simply put, zombie banks don’t lend. See chart.

If this Dollar intervention gains scale, look for the USD to reverse up and US equities to reverse down. If it is short-lived, watch whether the Dollar shorts come back strongly and continue to hammer it down. In such an event the Fed may be forced to act to support the Dollar or risk a rapid devaluation. I had not expected this Dollar Crisis to emerge yet, and view this as merely a warning shot across the bow of the US Ship of State. Yet in the short term it ratchets markets and needs to be watched closely.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply