The municipal bond market continued to roar ahead in the second quarter with long tax-free yields continuing their decline in April and May before rising slightly in June. Many of the same factors that were at work in the first quarter were again at work in the second quarter. Lower supply from a more austere universe of municipal issuers, higher demand from bond fund inflows, some asset allocation out of stocks and into bonds, and a general overall recognition of better municipal credit quality were all significant factors in the past three months. Liquidity – the ability to buy and sell bonds at reasonable spreads – has completely turned around from a year ago. Then we had the “taper tantrum” that saw record municipal bond fund outflows amidst fear of the Federal Reserve’s scaling back bond purchases. That period of June and July 2013 was marked by the almost total nonexistence of what one would consider a market-level bid. This was, of course, on longer-maturity municipal bonds, which are what bond funds owned and had to sell to meet redemptions.

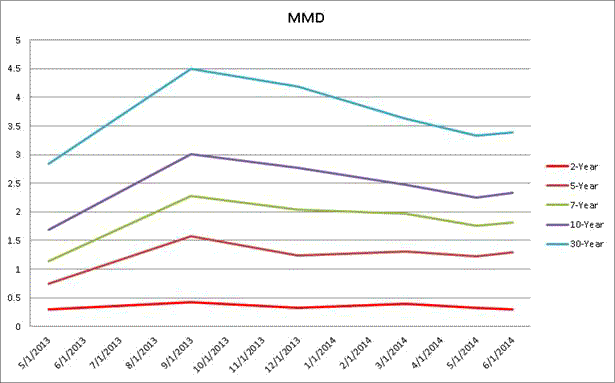

The graphs below demonstrate several salient points.

- Short-term yields were mostly unaffected last year, because the sell-off was the province of bond funds that bore the brunt of the tapering fears of retail investors

- Long-term bond yields were greatly affected, again because they were what bond funds WERE selling. The drop in trailing headline inflation from near 2% to 1.2% made longer-maturity tax-free munis the most compelling they had been since the post-Lehman Brothers sell-off of 2008.

- There has been a remarkable recovery in the tax-free bond market.

As we look forward, we continue to grow somewhat more cautious. Although long high-grade municipal bonds continue to look attractive compared to long US Treasuries, the continued rally (drop) in nominal yields has us readying for a pause that refreshes. Our concern is that we have travelled a road where long intermediate- to high-grade paper went from 3.5% yields in early 2013 all the way to 5-5.25% in late summer and now back to the 4% level or below, in many cases. Though a case can be made for continued downward pressure in rates, we are starting to become somewhat defensive. Portfolios have self-shortened as bonds yield to shorter call dates; and, at the margin, we have raised 5-10% cash in accounts. Many issuers will be issuing bonds to refund older higher-coupon debt as we approach the end of this year. This trend will continue into 2016. Although the amount of “net “new issuance might not be that large, the new issues still have to clear the market. That bulge, along with a possible flare-up in rates due to wage inflation, could present a buying opportunity; and we would like to have the ammunition with which to seize it. In addition, many market participants point out the large reinvestment bulge coming on July 1st from coupon payments, maturing bonds, and called bonds. With longer yields down 100-125 basis points from their peak, that reinvestment scenario may be more muted than people think.

Leave a Reply