The FOMC meeting begins today and ends tomorrow, followed by the traditional statement and Chair Janet Yellen’s first press conference. The Fed will also update its forecasts – important because ultimately the forecast drives the policy decisions. I don’t anticipate large changes to the growth or inflation forecasts. We should see modest downward revisions to the unemployment rate forecast. What will be more interesting is the impact those changes will have on the interest rate forecast. The bulk of the FOMC expects the first rate hike will be in the range of mid- to late-2015, with a handful earlier or later. A lower unemployment rate forecast may prompt some to move up their forecast. That said, I do not expect large changes in either direction.

As far as policy itself is concerned, it is widely anticipated that the Fed will continue to taper asset purchases and slice another $10 billion from the monthly total. There is no reason to think that the economy has shifted dramatically in either direction to alter the Fed’s current strategy for ending asset purchases. We know also that forward guidance will be on the table. Sometime soon – and I think the odds are better than even that “soon” is tomorrow – the Fed will need to address the Evans rule. My expectation is that they ditch numerical guidance for qualitative, discretionary guidance. The new guidance, however, should make it clear that rates will remain low for a long time.

Regarding low rates, I think it is worth reiterating a theme that the Wall Street Journal’s Jon Hilsenrath has been pushing this week: At this point, the Federal Reserve expects a long period of low interest rates even after they initiate the first hike. From Monday’s Grand Central Station:

…The central banks are projecting an economy that looks on its face like it is returning to normal in the next couple of years…Yet most Fed officials are projecting the target for short-term interest rates will be below 2%, much less than the 4% level that officials think is appropriate in normal times.

How can the Fed expect to maintain short-term rates so far below normal when its main metrics of economic vitality look like they’re back to normal?…

The economy is not getting back to normal, officials like Mr. Dudley are essentially arguing. It’s just getting to something a little less vulnerable. Watch out for the persistent headwinds argument in the Fed’s policy statement Wednesday or in Fed Chairwoman Janet Yellen’s press conference. It is the linchpin to the Fed’s assurance that rates won’t rise much in the next couple of years, even after they start inching up from zero. It is also one of the next battlegrounds in the Fed’s policy debates.

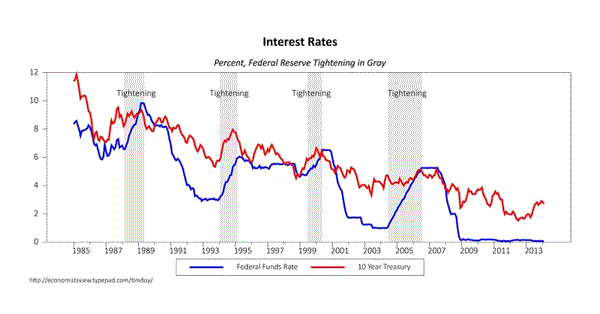

I am not entirely sure I like this characterization. The economy could have shifted into a new normal, and that new normal is characterize by a different constellation of prices, exchanges rates, and interest rates than the old normal. The new normal for interest rates may simply be lower than the old normal. Remember that we are still in the midst of a long-term secular decline in the level of interest rates:

Peak cycle interest rates – both short and long rates – have been on a steady decline since the 1980’s. And notice that the well-telegraphed Fed tightening in the last cycle had very little impact on long-rates. This raises the possibility that the big move in long-rates (after the tapering talk began) is already behind us. Thus, long-rate might not rise much if at all even as the Fed raise short rates. We will know the answer to that if buyers keep coming out of the woodwork whenever rates approach 3%.

This also implies that although the Fed may think they are running a looser policy than normal because short-rates are historically low, the reality is that the policy is equally tight in relative terms. Thus even though they will argue that rates are low even after they begin raising rates, they will still be reinforcing the continuation of the new normal.

Bottom Line: The Fed will continue with tapering by cutting another $10 billion from asset purchases. They will most likely alter the guidance but continue to signal an extended period of low interest rates. Low rates might simply be part of the “new normal” the economy is settling into, a new normal that the Fed may be unintentionally reinforcing.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply