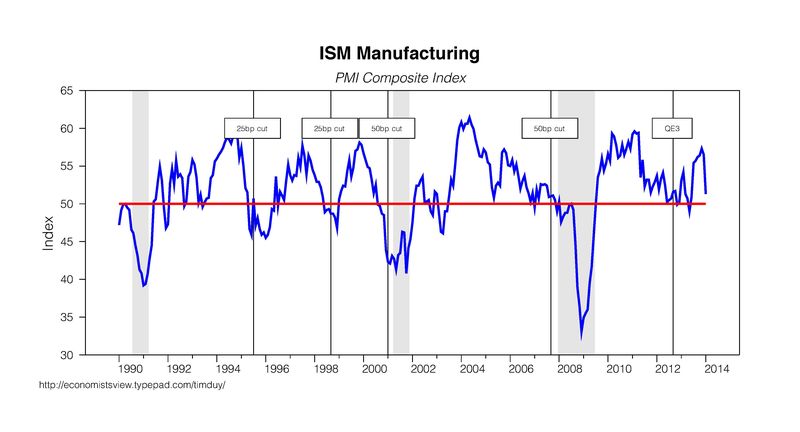

The financial markets are not being kind to freshly minted Federal Reserve Chair Janet Yellen. The level of scrutiny she will face when she makes what is likely to be her first public appearance as Chair next week was already high, and is rising by the minute. Global markets are faltering, and US equity markets tumbled Monday, with the weak ISM numbers reported to be the proximate cause of the sell-off:

(click to enlarge)

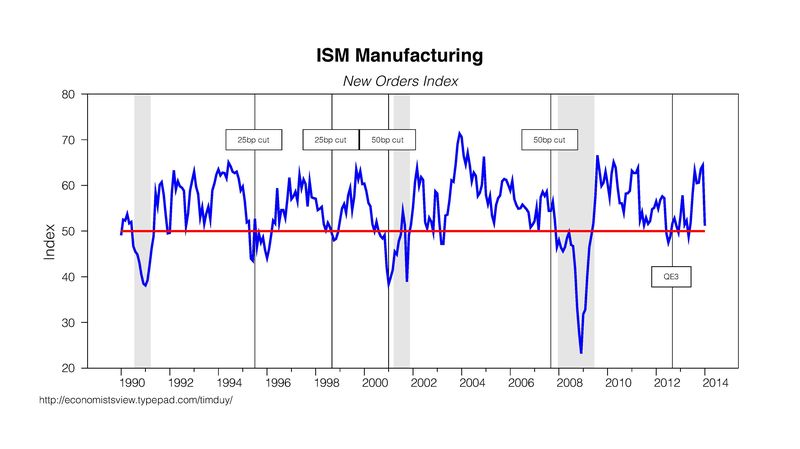

The decline was driven by what can only be described as a jaw-dropping decline in the new order component:

(click to enlarge)

Weather is suspected in the decline, and the ISM report offered some anecdotal support in that direction:

- “Poor weather impacted outbound and inbound shipments.” (Fabricated Metal Products)

- “Good finish to 2013, but slow start to 2014, mostly attributed to weather.” (Petroleum & Coal Products)

- “We have experienced many late deliveries during the past week due to the weather shutting down truck lines.” (Plastics & Rubber Products)

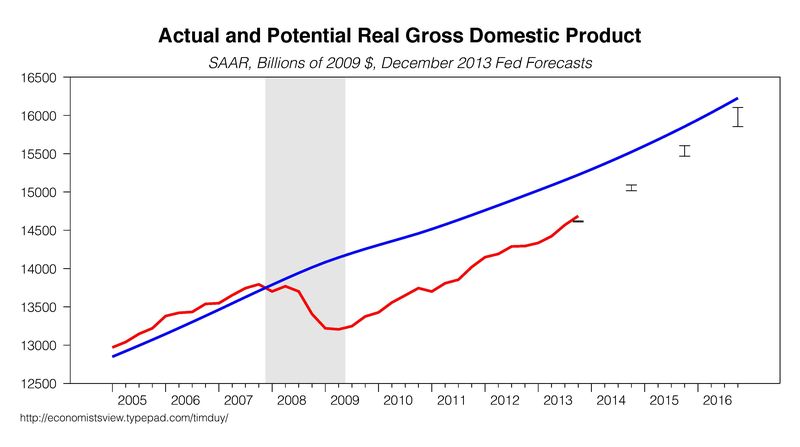

That said, this is arguably more than about just weather, and at least partially should trigger a fresh assessment on the strength of the US economy. To be sure, 2013 finished off with strong GDP numbers, strong enough to give the Fed hope that their 2014 forecast will be realized:

(click to enlarge)

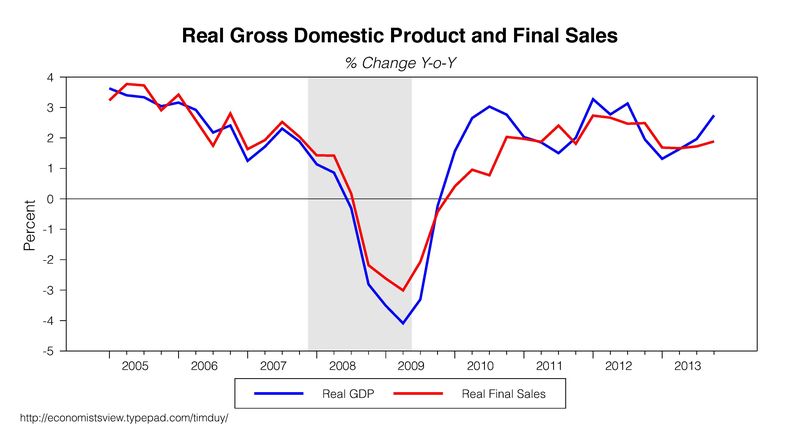

I suspect, however, that it is a bit too early to break out the bubbly. Recent gains have been driven by inventory build-up. Underlying growth still seems a bit tepid, in my view:

(click to enlarge)

Moreover, concerns about the health of the global economy are growing. Indeed, Ambrose Evans-Pritchard sees the threat of a global policy tightening in the making:

We now have a situation where the world’s two biggest economies – the US and China – are both winding down stimulus in lockstep. Call it simultaneous G2 tightening if you want. Europe is tightening passively as its balance sheets shrinks, and M3 money fizzles out. So let us call it G3 tightening (even if the Europeans are doing it by mistake)

This amounts to something of a shock to large parts of the emerging market nexus. Is it therefore proper for these EM states to further compound the shock with pro-cyclical monetary (or fiscal) tightening, and to do so on a scale that could ultimately push the global economy closer to a deflation trap?

Sounds very similar to my concerns from last week:

Funny thing is that what the Fed sees as no tightening is evolving into a global tightening now as central banks rush to raise rates. Consequently, money surges into the global safe asset – US Treasuries. And, interestingly, I think that you can argue that this is much, much more disconcerting than last year’s taper tantrum. This seems to me to be a pretty clear global disinflationary shock. And it isn’t like inflation was on a runaway train to begin with.

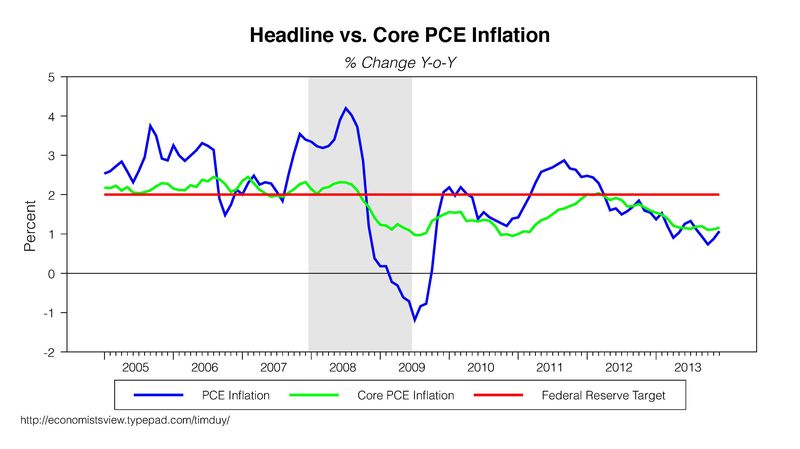

To reiterate the last point, the Fed’s decision to taper despite the obvious challenge to their inflation target looks increasingly questionable:

(click to enlarge)

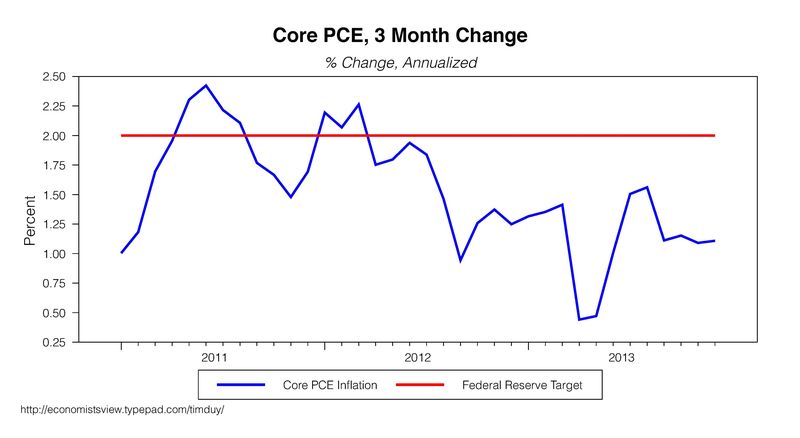

Fed policymakers don’t even really have any positive near-term trends to hang their hats on:

(click to enlarge)

Across the Curve points us to the Wall Street Journal’s anecdotal account of intense pricing pressures (and still weak demand) facing firms:

Executives from companies as varied as General Electric Co. ,Kimberly-Clark Corp. and Royal Caribbean Cruises Ltd. said some prices slipped in the last three months of the year—sometimes significantly—amid intense competition, weaker demand and pressure from cost-conscious customers.

Falling prices for adhesives weighed on Eastman Chemical Co., cheaper packaged coffee dragged on Starbucks Corp. , and “value and discounts” hit McDonald’s Corp. in the fourth quarter in what the fast food chain called a “street fight” for market share. Xerox Corp. is eyeing acquisitions that can “help us be more competitive on price pressure.”

Corporate revenues are showing the strain, whether from lower prices, weak demand or a combination of the two.

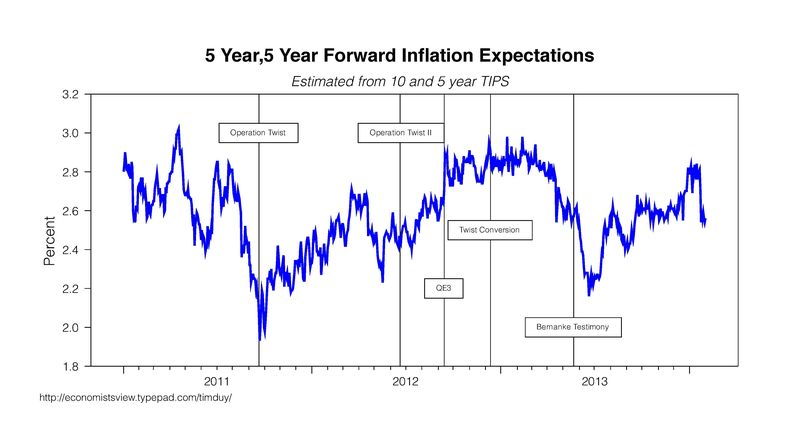

Despite the Fed’s claim that tapering is not tightening, that it is the stock of assets held, not the flow, that matters, that they could change the policy mix without changing the level of accommodation, market participants are acting as if tapering is indeed tightening. Five year, five year forward inflation expectations have tumbled:

(click to enlarge)

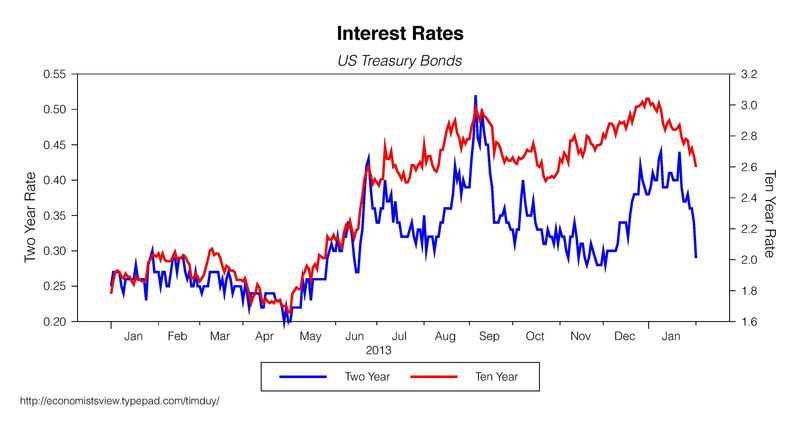

And bond market participants, who had been starting to get optimistic that improving economic conditions would prompt the Fed to tighten sooner than later are now rethinking that scenario:

(click to enlarge)

If this keeps up, it looks like Yellen will face an early test in her first few weeks as Chair. And I would say there is a good chance this does keep up until the Fed changes direction and decides that the US economy may not have reached escape velocity as believed. Of course, the early voice was a hawkish voice which signaled exactly the opposite, as reported by Michael Derby at the Wall Street Journal:

With regard to Fed policy, “I can’t say that things have changed just because of this market action,” Mr. Fisher said in an interview on Fox Business Network after the markets closed Monday.

The hawks fought long and hard for the taper; they will not be easily dissuaded from by a few sloppy days on Wall Street. Remember, the hawks believe asset purchases are fueling a potential asset bubble to begin with. Falling stock prices will only verify their bias and justify the policy.

Of course, the hawks will not be driving a policy shift. That shift would come from the center. But I sense that the center have something in common with the hawks – the center wants out of asset purchases too, which makes me think the bar to holding asset purchases steady at the next meeting is relatively high. Still, a deflationary shock should make them think twice. Then again, already low inflation should have made them think three or four times before tapering in the first place. Altogether, the desire to end asset purchases suggests to me that what we have seen so far is insufficient to prompt the Fed to change their plans. That is especially the case if the data does not soften further – if, for example, the next employment report shows a rebound in payroll growth and a further decline in the unemployment rate.

Another problem we have at the moment is the transition at the Federal Reserve. In many respects, Yellen is still an unknown commodity. Will she live up to her dovish reputation, or will she surprise on the hawkish side? I have to imagine that Yellen is not thrilled by this turn of events. Of course, no one would be, but she is in the unfortunate position of facing the House Financial Services Committee for the first time next week, and her words will carry an extra weight. If she opens the door to tapering the taper, so to speak, odds are she will be credited for a global rally – but then she has to follow through. If she acts as if the Fed is moving full steam ahead, then she will be blamed for the turmoil that ensues – and maybe have to reverse course after all.

Bottom Line: The Fed is once again in a familiar place. They try to pull back on policy, and markets tumble. Tightening has repeatedly proved to come too early; one wonders if the Fed would have had to keep doing more if they didn’t keep promising to do less. If history is any guide, they will eventually reverse course. But that same history would suggest that they need to see conditions deteriorate further before they act.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply