The presentation of Larry Summers at a recent IMF conference has generated a good amount of comments. While some of what he said was not completely new, the way he put together some of these ideas to present a fairly pessimistic view of the state of the US economy has led to a debate around the possibility of secular stagnation (see Krugman). Secular stagnation refers to the fact that some of the output losses during the crisis become permanent, the economy does not ever return to the previous trend.

But there was something else that Larry Summers discussed that I also find interesting: he referred to the fact that in previous expansions the US economy barely managed to reach full employment despite the existence of strong bubbles and excesses. This also leads to a pessimistic view of the recent years and not so much because of what happened after 2008 but what happened before 2008.

Here is some data and a story to make you share that pessimism: it is a fact that global real interest rates during the last expansion (2001-2007) were very low by historical standards. The main candidate to explain low real interest rates is the saving glut that Ben Bernanke referred to in his 2005 speech to describe the increase in the pool of global saving coming from Asia, Germany, Japan and oil producing countries. As saving increase, the world interest rate fell. In other countries (such as the US and some European countries), this led to an increase in spending and borrowing that resulted in an increase in global imbalances.

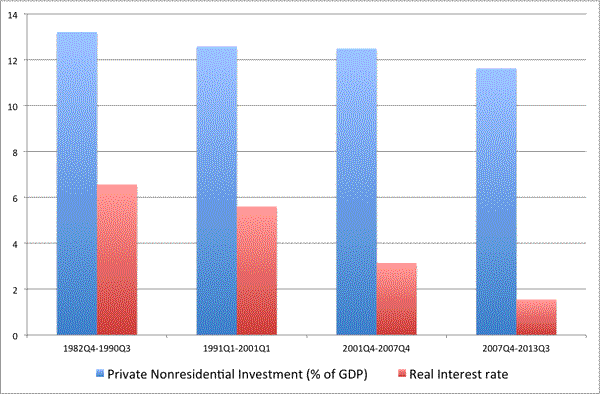

But if what we saw in these years was an increase in the pool of saving that drove down interest rates we should expect investment to increase (as supply shifts we move along a downward slopping demand curve to find the new equilibrium price). And if investment increases we should expect an increase in growth rates. But none of this happened. In fact, investment not only did not go up but it was lower than what it had been in previous expansions as shown in the chart below (data is for the US economy).

When we compare the last four expansions in the US economy we can see that while the real interest rate kept going down (especially in the 2001-2007 expansion), investment rates remained flat or even declined. I have included the current expansion in the chart although is not comparable to the others as it has not finished yet.

What happened to investment? Why didn’t it go up as real interest rates fell and the pool of saving was increasing? I am not sure we have an answer to these questions but what the data suggests is that we are not just facing the negative consequences of a deep recession, we should also have some concerns about the strength of the recovery based on the weakness of investment in the previous expansion (once we take into account the low level of interest rates).

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply