In this post, I’ll talk about two examples of how people tend to misinterpret market reaction to macro news.

You see lots of commentary to the effect that the stock market doesn’t care very much about the budget fiasco and/or that these budget fights only have a temporary impact on stock prices. If so, why wouldn’t investors buy stocks during a budget fight and sell them once the dispute is resolved?

At first glance, it seems like this strategy would work. And it often would work. But Eugene Fama and the EMH tell us that it’s too good to be true. Let’s take the 2% stock market rally last Friday on growing optimism of the budget deal. What does that stock market rally tell us? We can’t be sure, but the most likely explanation would go long following lines:

1. As of last Thursday investors saw a nontrivial risk of budget Armageddon. Let’s assume that budget Armageddon was expected to reduce stock values by 20%. That’s obviously huge, so in that case it would be wrong to say the stock market doesn’t care about the budget fight.

2. Let’s assume that last Thursday investors saw a 15% chance a budget Armageddon. That’s small, but obviously still significant. By Friday evening the perceived risk of default may have fallen to 5%. With 10% less chance of budget Armageddon that would reduce stock prices by 20%, stocks rallied by 2%. Of course these numbers are merely illustrative.

3. Changes in current stock prices are generally mirrored in changes in future expected stock prices. Thus if budget Armageddon had occurred and stocks had fallen 20%, then future expected stock values would also fall by roughly 20%. The effects are not temporary. That’s why even a 2% stock market rally is significant.

I am very sympathetic to the view that market setbacks in response to short-term crises are temporary. It certainly looks that way. However it’s a dangerously misleading way of looking at markets. Consider the sharp market “correction” of mid-2011. Stocks fell by nearly 20% during the euro zone crisis. When we look back on this period it merely looks like a blip in a powerful four-year bull market. But of course that’s not how it looked at the time.

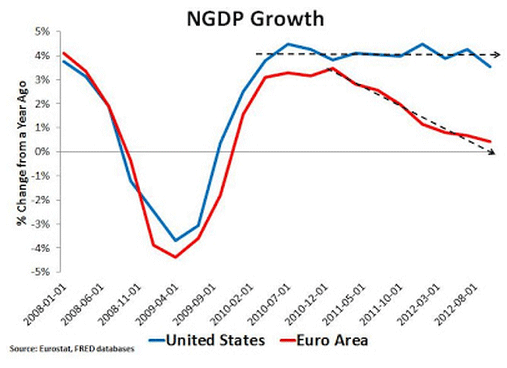

David Beckworth has a post comparing US and euro zone and GDP growth over the last decade:

What is puzzling to me is how anyone could look at the outcome of this experiment and claim the Fed’s large scale asset programs (LSAPs) are not helpful.

Note that though the euro zone and the United States have done roughly equal amounts of “austerity,” aggregate demand in the US has grown much faster than in the euro zone since 2011. And this difference largely explains the huge unemployment gap that has opened up between the two regions. Here’s Lars Christensen:

while the US is slowly getting out of the crisis things have in fact gotten worse and not better since ECB’s first rate hike in April 2011.

So the US in the euro zone have done roughly equal amounts of austerity, but very different monetary policies. As a result a nearly 5% gap has opened up between eurozone and American unemployment rates. And yet how often do you hear people say that QE is helped Wall Street but not Main Street? And they say this even though there is no plausible economic model where monetary policy could boost stock prices but not aggregate demand.

People get fooled by the fact that stock prices have recovered after each dip during the powerful four year rally. Thus it’s hard to see what the stock market was worried about during 2011. But if we look at Europe as a counterfactual, then the 20% dip in stock prices makes much more sense. The market might’ve been fearful that the US would also suffer a double dip recession. When it became clear that was not going to happen, stocks rallied. The double-dip recession that never happened in the US is sort of like the dog that didn’t bark in the Sherlock Holmes story, easy to overlook.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply