I tried a bunch of times to get on NYS’s health exchange last week. Dead end. The site went down for ‘repairs’ over the weekend, but as of 8 AM yesterday it was up and running. Some thoughts.

The first step is to get a user ID. For those familiar with this type of registration process the Captchas etc. are not a big hurdle. But two 8 digit codes (no spaces please) are required on step one. My guess is that there are fair number of people who will struggle with this. The same could be said for the password requirements (eight digits, two numbers and one capital letter).

The NYS exchange wants more than the standard ID info of address and SS#. I was asked a series of questions to ‘prove’ my identity. I was asked to identify a financial institution that I had opened an account with in the past two years. Five banks were listed, and one of them was the bank I had in fact opened a new account.

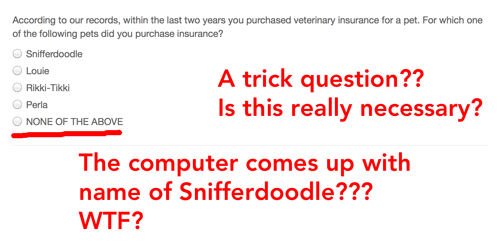

Another question blew my mind. I have never purchased pet insurance, so this was a trick question that required the response “None of the above” to continue with registration.

These questions prove that the exchanges have access to a great deal of information about who is signing up. I suspect that the need for the servers to go out and gather the individual’s data so that these questions can be posed, is the reason that the exchanges went down the first week. The plumbing for this can easily get clogged; the data bases for this type of info are huge. NYS has access to my IRS data, the pricing I got reflected the fact that my income was above the subsidy levels in the prior year.

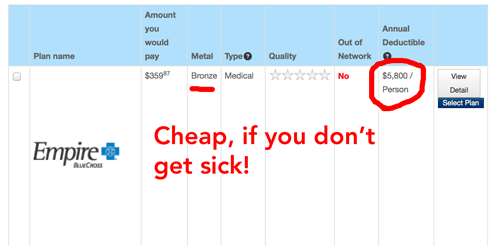

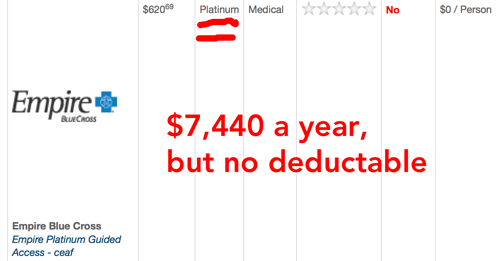

Once you exist, the rest is straight forward. I’m single, 63; I’m a headache for ACA. Obamacare needs young healthy people to enroll. For every one of ‘me’ ACA will need a half-dozen twenty-year olds to balance the costs. I looked at the cheapest plan (Bronze – $360/mo) and the richest (Platinum – $620/mo). The difference between the two extremes is the annual deductible:

This pricing structure is flawed. For the Bronze plan I would pay $3,684 per year and face a$5,800 deductible. If I get sick, my all-in cost goes to $10,120. If I pay the high monthly premium I would pay $7,740 a year, but incur no deductibles. Therefore, in the event I need the insurance I would ‘save’ $2,380 by opting for the Platinum plan. At my age the Bronze plan is a bad bet.

I can easily envisage an age cohort of mine who opts for the Bronze plan, gets sick and then is stuck with a $5,800 bill that can’t be paid. These very high deductibles are going to be a disaster for Obamacare. Who is going to eat the losses that will surely come from those with cheap plans and mega deductibles? The taxpayer will foot this bill….

I have medical insurance today that has similar features to the Platinum plan. It costs me $1,100 per month for the insurance. So I’m looking at a real savings of $5,760 per year! This is great news for me, and some will point to this and say that Obamacare is doing what it’s supposed to do. The fact that I am now in a group that includes lots of younger people who will not need the insurance has brought down my costs.

This is going to fail. I should not be getting a subsidy from Obamacare. My investment income the past few years (thanks to ZIRP/QE) puts me in the top 2% (Income greater than $175k = top 2%). Why in hell should I be getting a subsidy? And if I’m getting a subsidy, who is going to pay it? Those twenty-somethings are going to save me $5,800 a year?? Why?

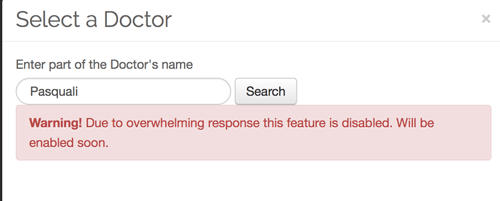

In spite of the large savings that I would realize from from signing up for Obamacare (a free one-month trip to Europe!) I did not hit the button. There is a catch in this for me. Can I keep the doctor that I have been seeing (and trust) for the past 25 years? There is no way to determine that. There is a field that allows you to check if your traditional doctor is covered by the plan. But when you ask, you get this:

Okay, this bug will get fixed someday, and when it does I will sign up for Obamacare (provided my Doc is in the group). When I do, I will save a bundle, but there is no way that this should be happening. Why is Obamacare putting big bucks in the pockets of geezers who are top 2%?

My conclusion is that the exchanges are setting the initial cost for insurance at rates that are artificially low. These are teaser rates that are designed to get folks to sign up. A year or two from now the insurance companies will be getting big increases. Whatever you think of Obamacare today, wait two years, you will come to hate it.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply