At the risk of shooting fish in a barrel, I’m going to offer some thoughts on investment in single-family real estate, particularly the recent rush into the sector by Wall Street. I’ve spent some time consulting for companies which manage single-family homes for investors as well as with an investor who was an early player in the acquisition of distressed properties, so I have a passing acquaintance with the business.

First off let me say two things. First, I’ve run into a fair number of investors who have played in this space for a number of years. Some had a couple of rentals, some ten or twenty and a few had a portfolio in the hundreds. The one thing in common they all had was that they were generally one-person, family or small partnership operations and were hands on operators. Those are the successful ones.

Second, I watched a lot of investors flood into this market in the early part of the decade, leverage up and get their heads handed to them. They were not an insignificant of supply of inventory for the housing crash. Once again most were small operators but, as opposed to the group I mentioned above, they had no clue as to what they were about. I suspect they would have failed even had they not overused leverage.

The lessons I took away are that the business of operating single-family homes for rental is a lot more complicated than it appears on its face, if you run your business well it’s a good way to get rich slowly and it does not scale. Rental income fluctuates month-to-month depending upon vacancies, repair and maintenance expenses are always more than you expect (never underestimate the amount of damage a tenant can do) and the ultimate payoff is asset appreciation. So I think that owning a couple of rentals is not a bad place to put some of your money provided you have a good manager if you’re not going to do it yourself and it’s not a bad way to build a business so long as you have the wherewithal to do a lot of the management and repair work yourself in order to keep the overhead down.

There is one other caveat. You have to acquire your properties well. That seems like a no-brainer but you would be amazed at the number of investors I’ve come across who either paid too much relative to the rents their properties could historically support or just bought dumps which were money pits from the outset.

So, I tend to think that a lot of individuals who got in early on in the game of picking up distressed properties for investment probably made some good investments assuming they bought well and retained good management or can do it themselves. I think that the rush by big money into the sector is going to come to no good end. Why? Well here are my thoughts.

Management

No, I don’t mean that the people running these funds are incompetent, they may be stars for all I know. I mean that the business doesn’t scale. I’ve seen management companies with 1,000 or more single-family homes they were running for investors and I’m sure some of them today might have doubled that number but they were swimming awfully hard to keep up with their portfolios. Think of the things you have to do:

- Collect rents

- Collect past due rents and late payments

- Deal with HOA violations and collect HOA fines from tenants

- Go to court to get affect an eviction

- Evict Tenants

- Respond to tenant requests for repairs

- Schedule and oversee third-party vendors (plumbers, electricians, HVAC companies etc.)

- Clean out vacant units

- Refurbish vacated units

- Rekey vacated units

- Coordinate with utilities

- Advertise and show properties for rent

- Evaluate prospective tenants

- Monitor rentals

I could go on but you get the idea. Now when you look at that list what jumps out at you. If you said it’s a people intensive business you get a gold star. There isn’t much on that list you can manage from a computer. Trust me it’s a juggling act worthy of the best circus performer. Now throw in geography and you have a nightmare. Phoenix, for example covers an area of about 9,000 square miles. For comparison, the state of Delaware encompasses about 2,000 square miles. The best of the large scale property managers I know limit their portfolios to specific geographic locations within the metropolitan area and even the smaller ones take that lesson to heart. Not so the Wall Street types. The information I’ve been able to dig up on these new players show no geographic discipline at all. This isn’t a business in which top line growth falls right to the bottom beyond a certain level. Regardless of the investor, this is a low margin high cost business.

Acquisition Age

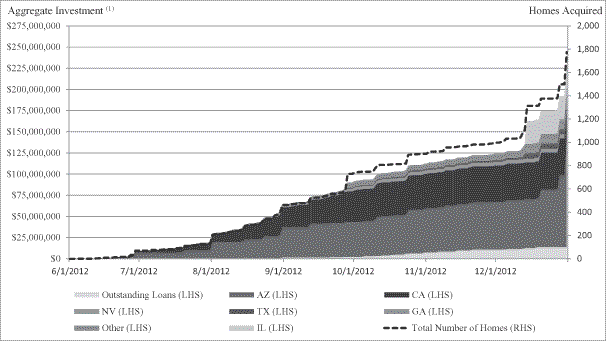

I know a lot of investors who did extremely well in this latest go around simply because they were liquid and jumped into distressed property at the right time. The right time was early 2009. By the end of that year foreclosure auctions were sold out affairs and the prices were up 25% or more. Still not bad buys but not the slam dunks of early that year. By contrast the Wall Street money didn’t move in until well into 2011 and really started buying in 2012. For example, from the prospectus for American Residential Properties, Inc, here is their acquisition activity since June 2012.

The company represents that as of March 31, 2013 it had a portfolio of about 2500 houses. As you can see, a significant part of that inventory was acquired in the past 9 months.

The point isn’t that the Wall Street money is overpaying for properties, I don’t know what homes will sell for in the future. From their prospectus it would appear that on a gross basis they’re renting these properties with a decent return, though their vacancy rate is troubling and if you give their gross rents a haircut only for taxes and vacancy, the returns are not eye popping. The point is, however, that at least for Phoenix their acquisition price doesn’t leave a lot of room for any erosion of the rental market either because of falling rents or increased vacancies. The big money is late to the party. Given the slim profit margins in the business their entry points don’t leave a lot of room for surprises, or as I’ll discuss in a moment a return of the single-family rental market to normal.

Rental Market

You have to look for a long time to find a better market for renting single family homes than we have right now. Vacancies are low, the quality of renters is high and they can afford premium rents. Trust me it hasn’t always been this way. You know the reason as well as I for this fortuitous turn, it’s a product of the housing crash. More specifically a good part of the renter market is comprised of former homeowners who lost homes through foreclosure. A lot of them make good money, have families and don’t want to live in an apartment and, of course, can’t qualify for a mortgage. The cherry on top is that they know how to maintain a home and as a rule take care of the rental.

It won’t last. Sooner rather than later the real estate industry is going to want to get their hands on this market and the government will oblige by altering the rules of the game to get them back into their own homes. That isn’t a bad thing for them or the country because a lot of them are where they are due to circumstances not because they are inherently deadbeats. When that happens … well you know what is going to transpire. Rental rates down, vacancies up, evictions up and expenses way up. Regression to the mean is going to be nasty for landlords, particularly those who didn’t buy low.

Here is the shooting fish in a barrel part. Right now the entire REIT market is taking it on the chin and some of the new single-family REITS (here and here) have been trading below their offering prices.

They’re getting hurt along with a lot of other income plays by rising interest rates in general, not because their performance has been inherently bad. I happen to like REITs as income plays and with some good analysis you can get into some pretty safe deals. As rates come down there will certainly be entry points for the asset class in general that make sense. I don’t think that holds true for the public single-family investment vehicles for the reasons mentioned above.

There may be a play with the single-family REITs at some point. When and if they decide to throw in the towel and liquidate there could well be some asset appreciation which accrues to shareholders. That presumes continued appreciation in the housing market, rational acquisition from here on and a management team which recognizes that liquidation is preferable to subpar investor returns. Lots of ifs there but it never hurts to look for the pony.

Wall Street avoided the single-family rental business for eons. I honestly don’t see what changed to merit their dive into it now.

Leave a Reply