Jim Hamilton is defending his recent work calling into question the sustainability of the US debt load. Brad DeLong takes a first shot at Hamilton’s post here. I take issue with this paragraph:

Whether a country is able to borrow in its own currency is completely irrelevant for the above calculation. Yes, it means the country likely won’t technically default on the debt, and could always create new money to pay off the creditors. But as Reis (2013) and Leeper (2013) have recently explained, printing money does not generate any magical resources with which to resolve a real fiscal shortfall. The central bank could create some more inflation, but anticipated inflation does nothing to alter the above determination of the limits on government debt. Anticipated inflation would just cause the nominal interest rate R and the nominal growth rate g to both increase by the same amount, and therefore would do nothing to change the net growth rate r = R – g which is the key parameter in our equation for sustainability (see for example equation (2) in Econbrowser March 6 or equation (8) in our paper).

This ignores the possibility of financial repression – meaning that the government can force yields on its own debt lower, thereby ensuring that inflation, even anticipated inflation, decreases real interest rates. Back to another post by DeLong:

…and (e) even if we start to tip over into an unsustainable debt-path scenario, we can handle it, because that is why God made financial repression.

Let me spell (e) out a little bit. If investors start to fear that the U.S. debt trajectory is truly unstable, the immediate consequence is a fall in the dollar and an export boom, with somewhat higher domestic inflation. Because the U.S. government regulates the financial system, it can set reserve requirements where it likes–it can thus use its reserve requirements to force banks to hold Treasuries, and if it doesn’t like the interest rate at which banks are holding Treasuries, it can up reserve requirements some more.

No, financial repression is not ideal. But it is not a disaster like a collapse of confidence in the debt and the currency….

Arguably, we are currently witnessing a real-time example in Japan’s Abenomics policy mix. The Yen has depreciated significantly, consistent with expectations of inflation. And there is even growing evidence that wages are responding as well. From FT Alphaville:

One of the big determinants of whether ‘Abenomics’ manages to pull Japan from its deflationary spiral is through wage growth. Inflation can’t really kick off or arguably even begin without rising wages. One can argue about how important wage growth is, or where it fits in causality-wise — and we’ll come to that later. But it is — or will be — an important signal as to whether this three-pronged approach of the new-ish Japanese government is working.

And actually, it might be catching on. The FT’s Ben McLannahan wrote in early February that the decision by convenience store chain Lawson Inc to raise wages of two-thirds of its staff by 3 per cent could be quite significant..

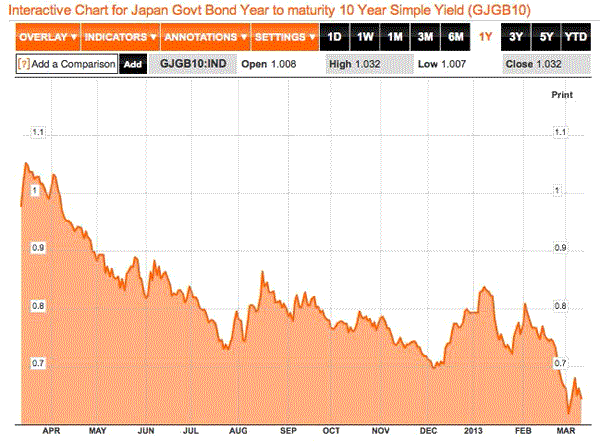

According to Hamilton, if we have higher anticipated inflation, we should see higher nominal interest rates on government debt, thereby debt sustainability is deteriorating. But alas:

Time and time again, Japan sticks out like a sore thumb that those preaching the unsustainability of government debt want to sweep under the rug with the “Japan is a special case” story (a country fixed effect). But it seems more likely that Japan’s economy is behaving exactly as you might expect given that it issues debt in its own currency. In other words, Japan is just a normal case pushed to the extreme.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply