I fell off the grid a couple of weeks ago, as seems to happen each time the teaching schedule ramps up. All those projects and papers seem like such a good idea until they show up on my desk needing to be graded. Between that and travel up and down I5 from one end of the state to the other, blogging suffered, to say the least.

There, however, is nothing like a Fed meeting to prod me back to the keyboard. Alas, the outcome of this meeting was not entirely unexpected. Policy remains unchanged, with only minimal changes to the FOMC statement. The Fed followed the path of all analysts not of the Zero Hedge variety and largely dismissed the unexpected decline in 4Q12 GDP:

Information received since the Federal Open Market Committee met in December suggests that growth in economic activity paused in recent months, in large part because of weather-related disruptions and other transitory factors.

“Transitory” = “don’t panic.” We can try to read something in the change of this sentence:

The Committee remains concerned that, without sufficient policy accommodation, economic growth might not be strong enough to generate sustained improvement in labor market conditions.

to:

The Committee expects that, with appropriate policy accommodation, economic growth will proceed at a moderate pace and the unemployment rate will gradually decline toward levels the Committee judges consistent with its dual mandate.

It sounds a little more optimistic, as though they are more comfortable they have policy about right. This, in turn, would suggest that no one at the FOMC is really thinking about accelerating the pace of asset purchases. Of course, I don’t think anyone was expecting that anyway.

There was no indication of setting thresholds for the end of large scale asset purchases. Such discussions are likely in their infancy; for now, all we know is that the end will come before the unemployment rate hits the 6.5% threshold. 7.25%, as suggested by Boston Federal Reserve President Eric Rosengren? Or a sustained period of substantial nonfarm payroll growth, as suggested by Chicago Federal Reserve President Charles Evans? Of course, these two thresholds may be effectively equivalent.

Kansas City Fed President Esther George (was she invited to the bloggers conference?) revealed herself as a true hawk with her dissent. To be sure, not entirely surprising. Still, I had wanted a little more confirmation before I labeled her a “hawk” rather than just having “hawkish leanings.” I got it. Her reason:

Voting against the action was Esther L. George, who was concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.

The potential imbalances reason seems like the primary reason for her dissent, and falls in-line with her recent speech. Such views are not uncommon – see A. Gary Shilling in Bloomberg, for example:

In desperation, monetary policies have become highly experimental. Huge government deficits are limiting the possibility of additional fiscal stimulus so policy makers are moving toward competitive devaluations. Meanwhile, low interest rates have spawned distortions as well as zeal for yield, regardless of risks.

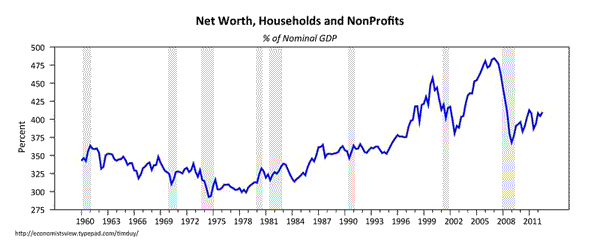

I can’t say that I am completely immune to such fears. Indeed, it is difficult to ignore the reality that the last two expansions were correlated with what I would argue were asset price bubbles. Moreover, I am somewhat interested in learning if the Federal Reserve could in fact stoke the fires of another asset bubble. But I think all of this speculation might be just a bit premature. We have an increasingly better idea of what an asset bubble looks like, and I don’t think we are quite there:

Yes, premature. Another 25% of GDP and I will likely start getting a little more nervous. Speaks to my concern that we are leaning a little too hard of monetary policy and not enough on fiscal policy. But that train has left the station.

Bottom Line: Like the Fed, I think it best to discount the GDP data. I didn’t really think the economy was growing over 3 percent in the third quarter, and I don’t below it was really shrinking in the fourth quarter. The underlying rate of growth is somewhere in between. More slow and steady for the time being. Slow and steady, though, has been enough to push the unemployment rate lower. As 6.5 percent comes closer – or if we see a handful of 200k+ nfp numbers – the Fed will begin easing back on the asset purchases. But I have trouble see that until mid-year at the earliest. For now, policy is on hold.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply